The rand (USD/ZAR) has not been a one-way road. Yet SA portfolios are more likely to be adding dollars when they are expensive and not doing so when the rand has recovered.

The rand cost of a dollar doubled between January 2000 and January 2002 – but had recovered these losses by early 2005. The USD/ZAR weakened during the financial crisis, but by mid-2011 was back more or less where it was in early 2000. A period of consistent rand weakness followed between 2012 and 2016 and a dollar cost nearly R17 in early 2016. A sharp rand recovery then ensued and the USD/ZAR was back to R11.6 in early 2018. Further weakness occurred in 2018 and the rand has been trading between R15 and R14 since late 2018. Weaker but still well ahead of its exchange value in 2016. The rand in March 2019, had lost about 20% of its dollar value a year before. It has recovered strongly since and t on July 5th at R14.05, the rand was a mere 4% weaker Vs the USD than a year before

The USD/ZAR exchange rate; 2000-2019 (Daily Data)

Source; Bloomberg, Investec Wealth and Investment

Two forces can explain the exchange value of the rand. The first the direction of all other emerging market currencies. The USD/ZAR behaves consistently in line with other emerging market (EM) currencies. And they generally weaken against the USD when the dollar is strong, compared to its own developed market currency peers.

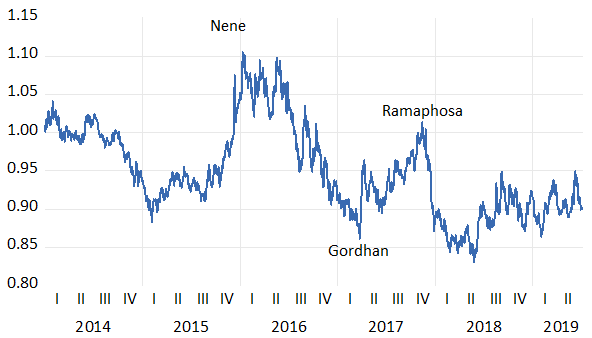

When the USD/ZAR weakens or strengthens against other EM currencies, it does so for reasons that are specific to South Africa. Such as the sacking of Finance Ministers Nene in December 2015 and Gordhan in March 2017. These decisions that made SA a riskier economy, can easily be identified by a higher ratio of the exchange value of the rand to that of an EM basket of currencies. The reappointment of Gordhan as Minister of Finance in late December 2015 improved the relative (EM) value of the ZAR by as much as 25% through the course of 2016. His subsequent sacking in March 2017 brought 15% of relative rand underperformance. The early signs of Ramaphoria was worth some 15% of relative rand outperformance – and its subsequent waning can also be noticed in an increase in the ratio ZAR/EM.

The rand compared to a basket of emerging market exchange rates (Daily Data)

Source; Bloomberg, Investec Wealth and Investment

This ratio has remained very stable since late 2018- indicating that SA specific risks are largely unchanged recently. Emerging market credit spreads have also receded recently – as have the spreads on RSA dollar denominated debt. The cost of ensuring an RSA five-year dollar denominated bond against default has fallen recently to 1.62% p.a. from 2.2% earlier in the year. The USD/ZAR exchange rate -currently at R14 – is very close to its value as predicted by other EM exchange rates and the sovereign risk spread. It would appear to have as much chance of strengthening or weakening.

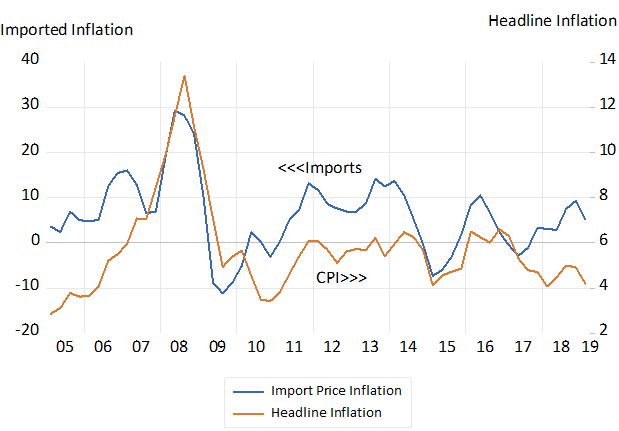

The exchange rate leads consumer prices because of its influence on the rand prices of imports and exports that influence all other prices in SA. A weak rand means more inflation and vice versa. And given the Reserve Bank’s devotion to inflation targets, the exchange rate therefore leads the direction of interest rates. Despite a renewed bout of dollar strength and rand weakness in 2018 import price inflation – about 6% p.a. in early 2019 -has remained subdued.

Import and Headline Inflation in South Africa (Quarterly Data)

Source; SA Reserve Bank, Bloomberg, Investec Wealth and Investment

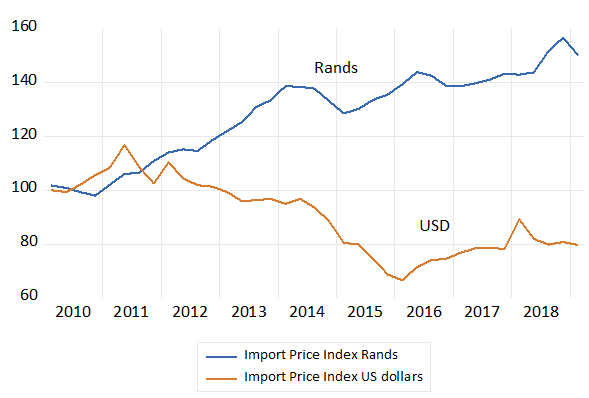

This has helped to subdue the impact of rand weakness against the US dollar that might have brought higher interest rates and even more depressed domestic spending. The dollar prices of the goods and services imported by South Africans has fallen by 20% since 2010 and by more than 10% since early 2018. This has been a lucky deflationary break for the SA economy.

SA Import Prices (2010=100)

Source; SA Reserve Bank, Bloomberg, Investec Wealth and Investment

Given that the rand is driven by global and political forces largely beyond the influence of interest rates in SA, it would be wise for the Reserve Bank to ignore the exchange value of the rand and its consequences. And set interest rates to prevent domestic demand from adding to or reducing the pressure on prices that comes from the import supply side. The SA economy can do better than merely hope for a weak dollar.