Post the lock downs the patterns of household spending are widely expected to change permanently. How it will change is of overwhelming importance to almost all business that supply households or are once or twice or three times removed from making sales directly to households. The demand to fly to some holiday destination not only affects hotels, B&B’s, restaurants, airports, travel agents, airlines and car rental companies taxi companies and all they employ or contract with – it will have the most profound implications for Boeing and Airbus and all their component suppliers.

Household spending accounts for 60% of all spending in SA and 70% in the US and other developed economies. Absent the control and command of governments (very active in the lockdowns) the decisions of households to spend or save or borrow to spend always moves the economy in the one direction or another. The market-place, post-covid19, will make the same call on its suppliers to adapt profitably to changing tastes. And to innovate successfully. That is to lead household spending to their own portals, real or virtual, depending on what will work best and be rewarded accordingly.

There is every reason for governments and their central banks to ameliorate the economic damage of their own making and offer compensation for the loss of incomes from work- including for the owners of businesses. Governments have every reason to encourage the demand for all goods and services when they allow firms after the lockdown to do what comes so naturally to them. That is to freely compete for custom and for the resources, labour and capital and premises to help them do so. There is no more reason for governments to get involved trying to pick post-covid business winners or losers than they would have at any other time.

And to leave future taxpayers with as little a burden of interest to pay on the additional government debt that is being incurred. Printing money rather than issuing expensive debt (when debt is as expensive as it is for the SA taxpayer) makes very good sense. The inflation in SA that might ordinarily come with money creation is a long way away- that is until supply and demand, both so damaged by the crisis, can recover to something like their potential.

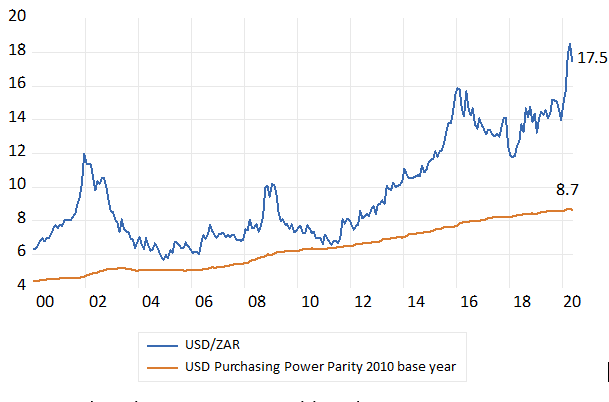

They say no crisis should be wasted. The crisis does provide an opportunity to stimulate what would be the most helpful source of growth for SA. That is export and import replacement led growth. The much weaker rand has made SA potentially much more competitive than it was only a few months ago. Adjusted for differences between SA and USA consumer price inflation the rand at USD/ZAR 17.50 is now about 50% undervalued Vs the dollar and about 18% more competitive with the US exporter or importer than it was at year end. A purchasing power equivalent dollar would now cost no more than R8.70 (See figure 1 below)

Fig.1; The USD/ZAR exchange rate and its Purchasing Power Equivalent[1] to May 27th 2020.

Source; Bloomberg, Investec Wealth and Investment

There is a strong case for retaining this competitive advantage. It is very easy to inhibit exchange rate strength should it materialize. The Reserve Bank can buy dollars with the rands it has an unlimited supply of. The Swiss National Bank does this all the time to hold back the Swiss franc. Furthermore buying dollars with rands would add to the supply of rands – it would be another form of money creation. And very helpful when every extra rand may encourage more spending and lending – so urgently needed for the recovery. Preventing exchange rate weakness should never be attempted.

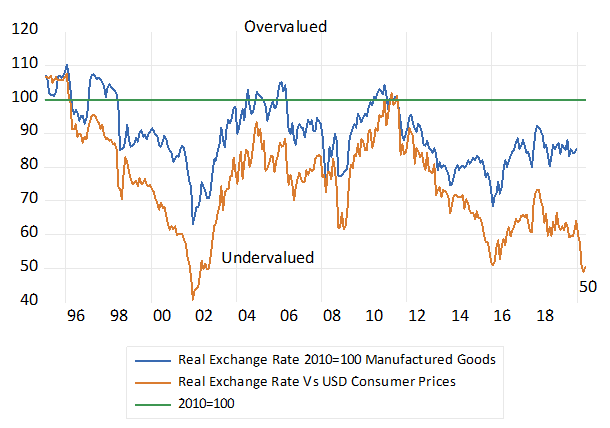

In figure 2 below we chart the relationship between the purchasing power value of the rand and its market value. This relationship represents the real exchange value of the rand with lower values indicating real rand weakness, or equivalently greater competitiveness for SA producers, and vice versa. We compare the real rand dollar exchange rate using the Consumer Price Indexes for SA and the US and the real rand exchange rate as calculated by the Reserve Bank. This real exchange rate is adjusted for the prices of manufactured goods of our 20 largest trading partners (weighted by their importance in our trade) using the prices of manufactured goods as the basis of comparison. This ratio has not been updated since year end. Given the stronger dollar the depreciation of the real rand so calculated is generally less severe than the real dollar exchange rate. The nominal trade weighted rand has declined by 20% since year end and so the real rand is likely to have declined by a similar degree this year.

Fig2. The real rand Vs the US dollar and SA’s trading partners. (2010=100)

Source; Bloomberg, SA Reserve Bank and Investec Wealth and Investment

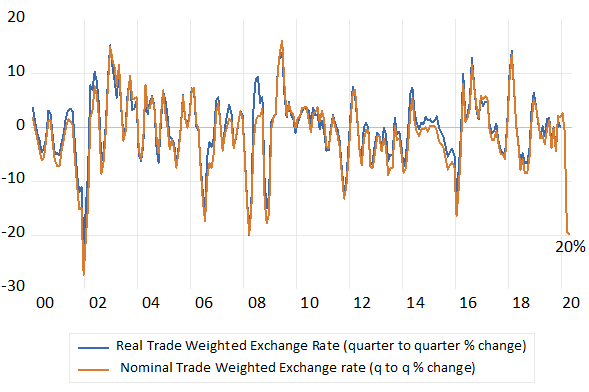

The value of the real rand is totally dominated by changes in the market value of the rand that fluctuates so widely and unpredictably. We compare quarterly movements in the market trade weighted value of the rand and its inflation adjusted value. As may be seen it is very much a case of the market exchange rate leading and the direction of inflation following. Rather than inflation leading to compensating changes in the market value of the rand. The so called pass- through impact of a weaker or stronger rand on prices in SA depends also on the direction of import prices in USD.

Especially important for the price level in SA is the dollar piece of oil that makes up a large percentage of SA imports- up to 40% at times. With oil prices as low as they are now the pass-through effect on SA prices and inflation is likely to be very subdued. Exporters from SA especially of metals and minerals that still make up a large percentage of SA exports are largely price takers established in US dollars. The weaker rand translates automatically into higher rand prices and vice versa. How much the weaker rand drives up the costs of our exporters and those suppliers who compete with imports depends very much on the direction of SA inflation. This is likely to remain subdued for now given the general weakness of demand for goods, services and labour.

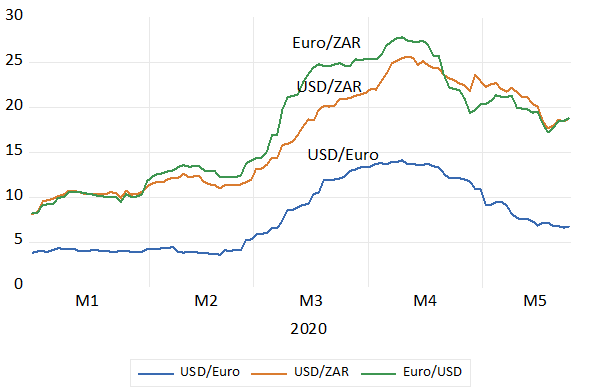

It is not only the level of the real rand that matters for the real economy. Movements in the market value of the rand and hence its real value of great importance for operating profit margins are also of great relevance. The USD/ZAR and the Euro/Rand exchange rate has been almost twice as variable on average as the USD/Euro exchange rate. This year is no exception. We show below how the volatility of these exchange rates on a daily basis this year.

Managing this volatility of the rand exchange rate is a burden carried by SA exporters and importers and those who compete with exports and imports.. It adds to their costs of hedging exchange rate risk and the pure uninsurable uncertainty about the actual direction of the rand demands a discouragingly higher expected return on their investments.

Fig.3 Quarterly per centage movements in the Nominal and Real Trade weighted rand – lower numbers indicate rand weakness.

Source; Bloomberg, SA Reserve Bank and Investec Wealth and Investment

Fig.4; Volatility of the USD/ZAR, the USD/ZAR and the Euro/USD Daily Data 2020 to May 25th[2]

Source; Bloomberg and Investec Wealth and Investment

There should be two objectives for exchange rate policy during and after the crisis. Firstly, should the opportunity present itself, to inhibit rand strength to encourage domestic production and consumption. Especially since inflation will be looking after itself well enough and interest rates do not need a stronger rand to decline further. The very weak domestic economy is reason alone for still lower interest rates. Secondly, and a much more difficult longer-term exercise, would be to seek ways to inhibit exchange rate volatility that is such a burden on foreign trade.

[1] The PPP rand is calculated as USD/ZAR in December 2010 (USD/ZAR=6.31) multiplied by SA CPI/US CPI) 2010=100

[2] Volatility is calculated as the 30 day moving average of the Standard Deviation of daily percentage movements in the exchange rate