The short fall in government revenues of R56.8 billion reported in the Budget Review of 2023 came as no surprise to observers of the monthly tax returns. It represented a moderate miss in volatile circumstances – equivalent to 3.1% of the revenues expected in the February 2023 Budget of R1787.5 billion. A very large number and equivalent to 25% of GDP. This real tax burden (Taxes/GDP) is not expected to change over the next few years. Underestimated company tax, lower by R35.8b and net revenues from VAT down by R25.6b, accounted for much of the revenue shortfall. Weaker metal prices and massive investments in alternatives to Eskom power were largely responsible for both declines. Personal Income Tax grew as expected by 7% in line with some growth in real wages and salaries for those employed in the formal sector. The shortfall will be fully covered by raising additional loans of about R54b.

The higher ratio of national government expenditure to GDP, currently 29.1%, is estimated to decline to about 28% of GDP over the next three years. Still leaving scope for a positive Primary Balance of 0.3% of GDP this year and 1% next year. Raising revenues to exceed expenditures, net of borrowing expenses, is the first and necessary step to reducing the burden of National Debt to GDP-now about 74%, though predicted to decline to about 71% of GDP in three years. National government expenditure, is estimated to increase by an average 4.6% p.a. over the next three years, including servicing our debts, currently over 20% of all revenue that will cost the taxpayers about R400 billion this year. That would represent a decline after inflation.

The SA government is still practicing fiscal conservatism despite persistently slow growth that weighs so heavily on revenue. And inhibits expenditure. And raises persistent doubts about fiscal sustainability. That is the willingness of the government to avoid money creation, that is a heavy reliance on its central and private banks to fund its expenditure over the long run. Which raises the risks of more inflation and is already well reflected in high borrowing costs. Risks incidentally that have not trended higher in the run up to the Budget Review. Encouragingly the debt and currency markets reacted positively to the statement itself. The rand strengthened to improve the outlook for inflation and long bond yields declined by about 15 b.p.to help reduce debt service costs.

Source; Bloomberg

South Africa; Risk Spreads- Differences in borrowing costs. RSA-USA

Source; Bloomberg, Investec Wealth and Investment

In reading the Budget Review and listening to the Minister one is struck by how deeply dissatisfied the government is with its own performance. The statement is a catalogue of government failure.

To quote the statement

The case for reconfiguring government, as it is put, is vigorously argued by the government itself. It will however need its own genuine champions informed by events rather than a stale ideology. It will have quite simply to put the private sector and private sector incentives in control of much of the activities so badly performed by the SOE’s and government departments generally, that could be outsourced. It can be called private public partnerships rather than privatization, but the essential reforms required will be to incentivize operating managers on the bottom line and return on capital- as the private sector does – to thrive and survive. The upside is incalculable.

And as far as funding a reformed public sector, the place to start would be to dispose of key underperforming assets on the best possible terms. Selling assets or leasing them over the long term would be equivalent methods for raising capital and reducing government debt. The leases can be sold to funders (foreign and local) who would be very keen to provide finance on favourable terms, given credible operators. The Transnet iron-ore line from Sishen to Saldanha would be an obvious candidate for sale or lease. There will be many other such projects made much more valuable under different operating control. For the mines to lease and operate their essential gateways to the market would add many billions to their values and taxable incomes.

The odds on a US recession in the next twelve months have receded in the light of the continued willingness of US households to spend more- despite much higher interest rates and reductions in the supply of money and bank credit. Spending on goods and food services rose by 0.7% in September on top of a robust increase of 0.8% in August. The annual increase in retail sales is 3.7% and the increase over the past three months is running at an annual equivalent of 8% p.a. Prices at retail level are falling. They stimulate demand but they also devalue the inventories held to satisfy demand. Prices have their supply and demand causes. They also have their effects on demand- and supply. Lower prices stimulate demand and incomes are now growing faster than prices.

All that is holding up the US CPI – now 3.7% up on a year ago – are house prices – and what are imputed as owners’ equivalent rent. That is at what the owners could earn if they rented their homes They are up 7% on a year before. They have a huge weight in the CPI – over 25% – and if excluded from the CPI – would have headline inflation running in the US below the 2% target. Cash rentals account for a further 7% of the US CPI. By contrast food eaten at home carries a weight of only 8.6% in the CPI and food eaten out is 4.8% of the US CPI Index. SA also includes owners’ equivalent rent in its CPI with a weight of 12.99% and actual rentals account for only 3.5% of the index. Both rental series in SA are up by a below average 2.6% on a year before. The headline inflation rate in SA was 5.4% in September.

Owners equivalent rent is a very different animal to other prices. Higher implicit rentals based on the improved value of an owner’s home are not the usual drag on spending. The extra wealth in homes, as would all increases in household wealth, more valuable pension plans, more valuable share portfolios, etc. will encourage more, not less spending. The boom in US house prices post Covid has had much to do with the ability and willingness of US households to spend more and help push up prices generally. Average house prices in the US are now falling under pressure form much higher mortgage rates and house price inflation to date will be falling away rapidly as will owner’s equivalent rentals. Thus helping to reduce headline inflation.

The question investors are asking about both inflation (falling) and the state of the economy ( holding up) is what will it all mean for interest rates. The stronger the economy the lesser the pressure on the Fed to lower short rates. And the greater will be the pressure on long term rates in the US. The key ten-year Treasury Bond is now offering 4.9% p.a. reaching a 16 year high. In the share market what is expected to be gained on the swings of earnings may be lost on the roundabouts of higher interest rates, used to discount future earnings. But if inflation is subdued, any visible weakness in the economy, can be followed immediately by lower interest rates. This thought will be consoling to investors.

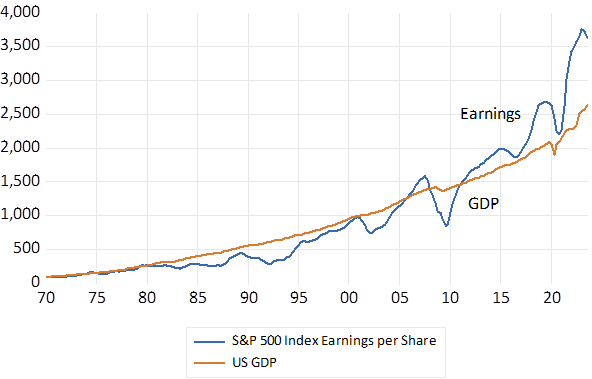

The attention paid to GDP by investors is fully justified. Where GDP goes so will the earnings reported by companies. Their correlation since 1970 is (R=0.97) Though helpfully to shareholders in recent years earnings have been running well ahead of earnings indicating widening profit margins from the IT giants. GDP , on a quarter-to-quarter basis, is a highly volatile series. Though growth in earnings is much more volatile.

US GDP and S&P 500 Earnings. Current values. (1970=100)

Source; Bloomberg, Federal Reserve Bank of St. Louis and Investec Wealth and Investment.

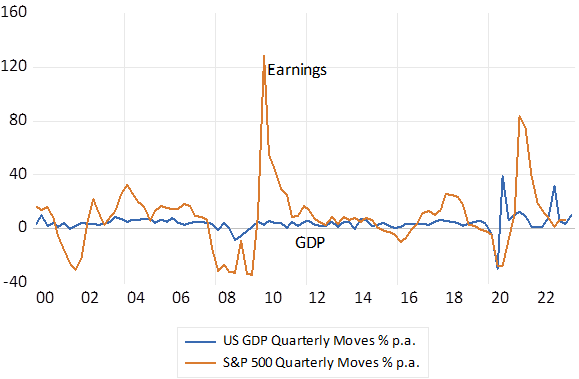

The underlying trend in GDP and earnings will never be obvious. To make sense of their momentum, to recognize some persistent cycle, the data has to be smoothed and compared to a year before. Thus we will know only in a year or more whether the US economy has escaped a recession. It is not recessions that move markets, only expected recessions do so. And the jury will always remain out.

GDP and S&P 500 Earnings Growth Quarter to Quarter % Annualised.

Source; Bloomberg, Federal Reserve Bank of St. Louis and Investec Wealth and Investment.

We all know that market determined prices reconcile supply and demand. Higher prices discourage demand and encourage supply. What is true of an individual price is true of all prices on average, as represented by a Consumer Price Index(CPI) That prices generally tend to rise with increased demands or reduced supplies and vice versa seems obvious enough.

Higher prices discourage demand and encourage supply. That prices generally tend to rise with increased demands or reduced supplies and vice versa seems obvious enough. But the supply and demand for all goods and services are not determined independently of each other. The supply of all goods and services produced in an economy over a year is equivalent to all the incomes earned producing the goods and services that year. The value added by all producers (GDP) is equal to all the incomes earned supplying the inputs that produce output. Incomes are received as wages, rents, interest, dividends, taxes on production and what is left over, the profits or losses for the owners after all input costs have been incurred.

Produce more, earn more and you are very likely to spend more. The economic problem, not enough of everything, too little income, is surely not the result of any reluctance to spend on the necessities or luxuries of life. The problem is we do not produce enough, earn enough income to spend really more.

Extra demands can be funded with debt. Yet for every borrower spending more than their incomes, there must be a lender saving as much. Matching financial deficits with financial surpluses, is the essential task of financial markets and financial institutions, and may not happen automatically or seamlessly. There may be times when the demand for credit and the spending associated with it may run faster or slower than the supply of savings. If so incomes and output may increase temporarily above or below long-term trends. We call that the business cycle. Interest rates (yet another price) may be temporarily too low or too high to perfectly much the supply of and demand for savings. But such imbalances must sooner or later will run up against the supply side realities, the lack of income.

There is a further complication. The supply of goods and service is augmented by imports. And demand includes demand for exports. In South Africa both imports and exports are each equivalent to about 30% of the economy, making a large difference to supply and demand. But the prices of these imports and exports are not set in South Africa. They are set in US dollars and translated into rands at highly unpredictable and generally weaker exchange rates. The prices paid for imports and exports affect average prices. And they mostly push the averages higher. It has been the case in SA of a weaker exchange rate leading, equivalent to a supply side shock, and prices following.

And the rand is still expected to depreciate against the dollar by more than the difference between SA and US inflation. The bond market expects the rand to weaken against the USD by an average 7.3% p.a. over the next ten years, being the spread between RSA bond yields (12%) and the US yield(4.7%) While the difference in inflation expected in SA (7.2% p.a.) and in the US (3.2% p.a) over the next ten years is much less, only 4.8% p.a. according to the break-even gap between vanilla bond and inflation protected bond yields.

Lenders to the SA government remain suspicious of SA’s ability to grow fast enough to raise the taxes that could sustain fiscally responsible policies. That is the government will not avoid resorting to funding expenditure with money supplied by the central and private banks. A sure source of extra demands without extra supply that leads to ever higher prices as it does persistently in most African countries.

There is little monetary policy and short-term interest rates can do to strengthen the rand and bring inflation down further against this backdrop. That is without resulting in too little demanded and even less supplied than would be feasible. That in turn bringing still slower growth more fiscal strain, higher borrowing costs and a still weaker rand- and higher prices. The call is not to inhibit already depressed demand but for economic policy reforms that would stimulate the growth in SA output and incomes enough to change the outlook for fiscal policy, the exchange rate and inflation.

The group of countries that will make up the enlarged BRICS, Argentina, Egypt, Ethiopia, Iran, Suadi Arabia and the UAE have little in common other than a deep suspicion of the motives of the US and its close allies. A state of mind also shared by left wing opinion everywhere including in the US itself. If the unlikely combination of kingdoms, autocracies and genuine democracies is to become more than a another talking shop with an anti-West bias, then it should take an important lesson from the economic development of the US and Europe.

What has been of great benefit to the US and to Europe, since it established a common European market and Euro are their highly significant common currency areas. The same money is used everywhere in the US and Europe as a medium of exchange and a unit of account. Thus unpredictable rates of exchange when buying or selling goods and services across frontiers are avoided, as are the direct costs of converting one currency into another- usually converting US dollars -into the domestic money.

Trade and financial flows between the states of the US and now of Europe is greatly encouraged by what is a fixed exchange rate regime within a common market, also free of protective of domestic industry tariffs or discrimination against foreign suppliers, by regulation. As it does incidentally when transactions of one kind or another take place within any country. The important trade between Gauteng and the Western Cape for example is facilitated by prices set in the rand common to both.

In the nineteenth century when which international trade and finance first flourished and economies came to benefit from wider markets for their goods and labour, and the ability to realise productivity and income enhancing economies of scale, currencies were mostly linked by fixed rates of exchange. The link was the ability to convert the different monies, if necessary, into gold at a fixed rate. And the issuers of different monies made sure to maintain convertibility by protecting their balance of payments through adjusting domestic interest rates. If gold generally flowed out interest rates could be raised to conserve and attract gold reserves and vice versa. Provided the commitment to currency convertibility was fully credible, the extra interest received would balance the payments by attracting or retaining capital.

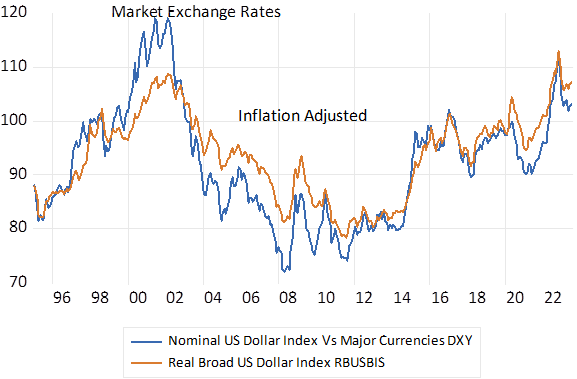

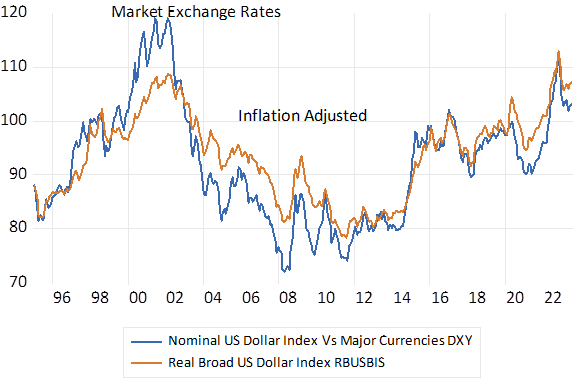

A modified fixed exchange rate system was re-established after the second world war with the US dollar as the reserve currency- but dollars that could be converted into gold at the request of other central banks. This commitment was abandoned unilaterally by the US in 1971 and market determined exchange rates, with the still dominant US dollar, became the norm. Highly variable rather than predictably fixed exchange rates have become the unsatisfactory order of the day. The rates of exchange of other currencies with the dollar, both in money of the day terms and when adjusted for differences in inflation of different currencies have varied very significantly – and unpredictably- damaging volumes of international trade and real investments.

US Dollar Exchange Rate Index. Market Determined and Inflation Adjusted

Source; Bloomberg, Federal Reserve Bank of St.Louis and Investec Wealth and Investment

It has not been a case of exchange rate moves levelling the playing field for traders in goods and services- so maintaining purchasing power parity in the face of differences in inflation rates across trading partners. Rather the exchange rates have adjusted to equilibrate independent flows of capital – large and reversible flows – in search of better risk adjusted rates of return- to which inflation then responds. Weaker exchange rates lead to more inflation and vice versa. Without stable exchange rates, controlling inflation in the face of capital withdrawals and a suddenly weaker exchange rate with the US dollar can become a severe interest rate burden on the domestic economy – as South Africa demonstrates.

The enlarged BRICS could establish fixed exchange rates between each other to promote trade and investment. They might usefully adopt a Chinese standard- that is offer convertibility of their own currencies into Renminbi at fixed rates. And rely on the Bank of China to manage the float of the crucial rate of exchange of Renminbi into US dollars, as it now does.

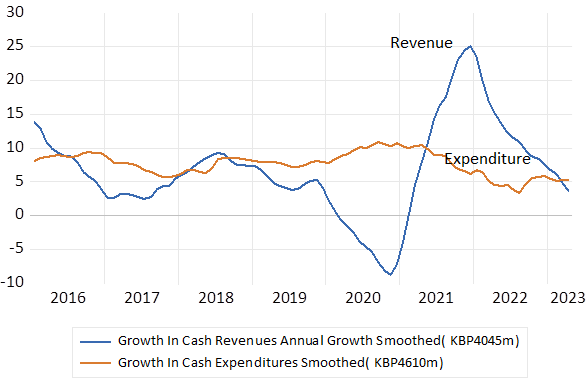

An unexpected shortfall in SA government revenues, has provoked something of a fiscal contretemps. R60b less revenue than was estimated in the February Budget has followed an even larger windfall in 2021 linked to the post Covid inflation of metal prices. The recent pull back in metal prices and in mining company profits has seen government revenues falling back sharply from peak growth rates of 25% in late 2021 to zero growth. Government expenditure has stayed on an essentially modest growth tack of about 5% p.a.

Recent Trends in SA National Government Revenues and Expenditure. Growth smoothed Y/Y

Source; SA Reserve Bank and Investec Wealth and Investment

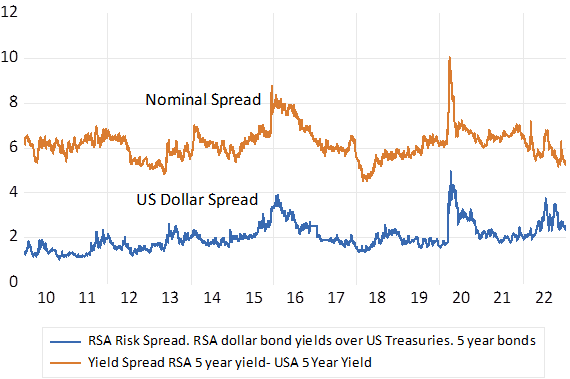

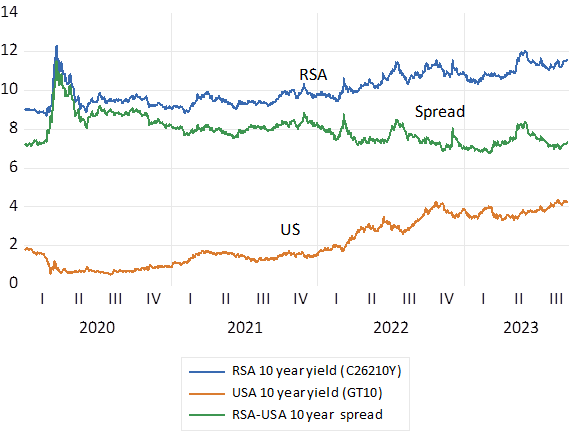

Less revenue means more borrowing. South African taxpayers are already paying a high price for our highly compromised credit-rating. We pay an extra 2.7% p.a. more than Uncle Sam to borrow US dollars for five years. And a rand denominated RSA five-year bond offers investors 5.5% p.a. more than a US Treasury of the same duration (9.89-4.39) The spread on a ten-year RSA over the US Treasury yield is even higher, over 7.3 % p.a. (11.57-4.25). The reason for such expensive, after expected inflation, borrowing costs and risk spreads is the persistent skepticism of potential investors in SA bonds, local and foreign, about the willingness and consequences of South Africa having to live within the limits of government revenue- heavily constrained as it is expected to be – by very slow growing GDP. The further forward lenders are asked to judge our growth prospects and fiscal policy settings, the wider have been the risk spreads and the higher the cost of issuing long dated debt.

RSA and USA 10 year bond yields and risk spread.

Source; Bloomberg and Investec Wealth and Investment

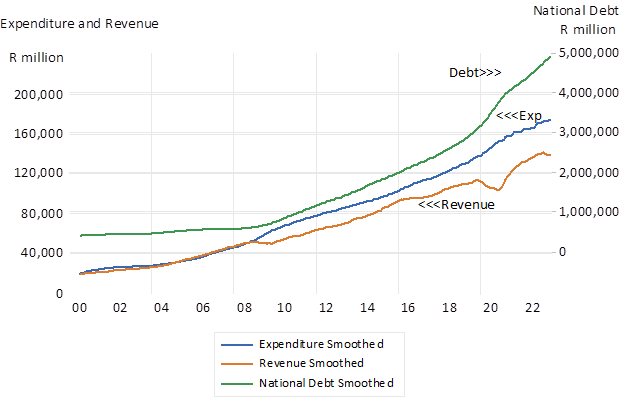

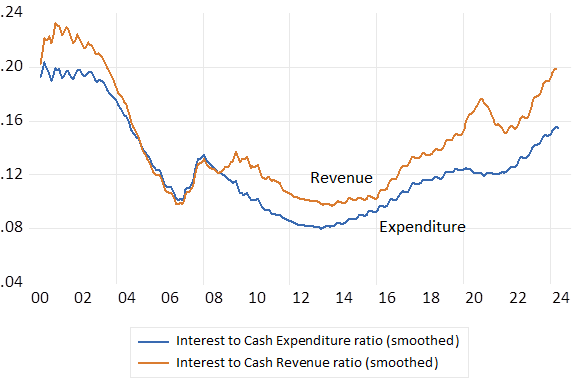

Yet if it is a crisis in the bond market (not immediately obvious given modest recent interest rate movements) the heavy burdens of raising debt for the SA taxpayer has been a long time in the making. SA national government revenues have consistently lagged government spending- by a per cent or two each year ever since the recession of 2010. And the Covid lockdowns were naturally much harder on revenues than government expenditure. These difference between revenue and expenditure have had to be covered by large extra volumes of additional government borrowing. The share of interest paid by the national government in revenues and expenditure has been rising sharply, doubling since 2014. Interest paid in serving the national debt is now 20% of all national government revenues and about 16% of all expenditures. It is not the kind of expenditure that helps win elections.

SA Government Revenue, Expenditure and Debt

Source; SA Reserve Bank and Investec Wealth and Investment

Share of Interest Payments in National Government Revenue and Expenditure

Source; SA Reserve Bank and Investec Wealth and Investment

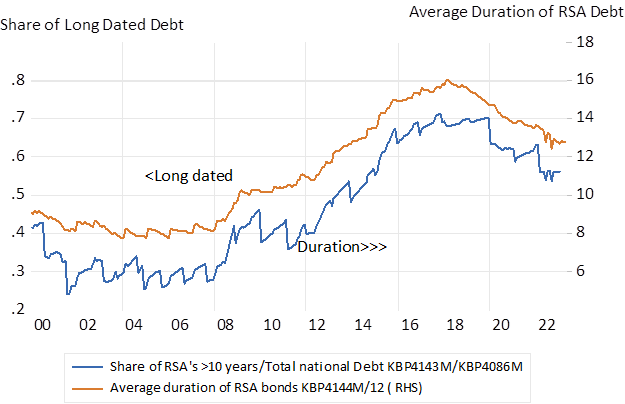

The share of RSA debt of more than ten years to maturity rose strikingly from 30 to over 70 per cent of all national government debt between 2008 and 2020 – at inevitably much higher rates. The government could immediately relieve part of the burden of high interest rates by reducing the extraordinarily long duration of RSA debt. As indeed it has been doing since 2018.

The extended duration of RSA debt. Long dated debt as share of total debt and average duration of all debt in years (Monthly data)

Source; SA Reserve Bank and Investec Wealth and Investment

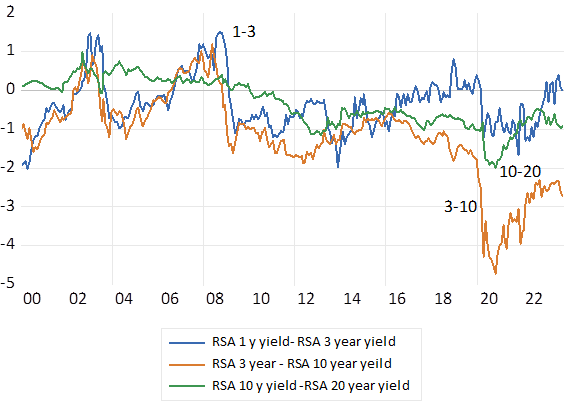

RSA Bond yield differences- by duration of debt

Source; Iress and Investec Wealth and Investment

It was a form of hubris to think that lenders would be willing to take a twenty year and longer view on the fiscal outlook for SA on reasonable terms. The long-term lender is highly exposed to inflation and default through inflation, that the short-term lender largely avoids. The benefits of borrowing long are apparently that it avoids the risks that rolling over short-term debt that may prove to be difficult at inconvenient moments in the money markets. But this makes even less sense when the SA Treasury was building its cash reserves at the Reserve Bank from R70 billion in early 2010 to R183 billion by January 2023.

Managing the interest burden of national debt can play a small part in solving the problem of slow growth for the SA government. Even should government and private spending in real terms remain as deeply and unpopularly constrained as it is likely to be this year and next. Only faster growth can avoid the interest rate trap as interest paid/all government spending should rise further. Absent growth the burden of paying interest, rather than undertaking other forms of spending, is very likely to make a resort to money creation, as an alternative to more borrowing, irresistible. The growth enhancing choices for economic policy should be obvious. There is really no other way.

Peter Bruce has pointed to something in the Stellenbosch water of the late sixties and seventies that produced so many rand billionaires. They would not have been inspired by some professor of economics enthusiastic about the power of free markets telling them to do good for the nation by getting rich. They are much more likely to have been told the opposite. Told why markets will not work nearly well enough and that any faith in entrepreneurial flair would be entirely misplaced. I have yet to meet a Stellenbosch economist who believes that an economy is best left guided by the forces of competition.

And one can perhaps understand why. The interventionist economic policies, long adopted in SA before 1994, clearly helped to completely transform the economic and educational status of the Afrikaner nation, in a generation, both absolutely and comparatively. They might have done even better with freer markets, but this would not have been self-evident. By every measure, the Afrikaner, on average lagged well behind the standards enjoyed by the average English speaker in the nineteen thirties. By the sixties they had caught up. Even, as the average incomes of both communities had improved significantly.

Many of the best and brightest Maties sought their futures working for the state and its agencies. The case for ownership by the state of some of the commanding heights of the economy, steel, electricity, railways and ports was taken as a given and not contended. And they were not, with few exceptions, seen as the path to private riches through corrupted procurement and biased tenders to which SOE’s are so conspicuously vulnerable. Nationalism and strong sense of community may have had something to do with this restraint.

Perhaps with Johan Rupert a fellow student, the example of the ineffable Anton Rupert was the inspiration. He who went door to door selling shares in his fledgling enterprise that was to take down a powerful near monopoly of the cigarette market in SA. The billions of the Stellenbosch cohort, like those of the Ruperts, were made in a conventional way. By competing successfully with established businesses for their customers and executing better combined with intelligent financial engineering that is always the leveraged and risky path to great wealth. Taking the opportunity provided by contestable markets is characteristic of successful, dynamic economies.

Peter Bruce is quite wrong to assert (Business Day July 27th) That Stellies route to billions is gone — and it’s undesirable. Apartheid-era billionaires can’t be reproduced in today’s democratic conditions.

It would be highly desirable were the South African economy to produce a few more billionaires in a similar old-fashioned way. By taking on established interests, winning market share and reviving businesses that have lost their way and are now valued at far below what can be regarded as their replacement cost. With the help of value adding, better designed financial structures and appropriate incentives for managers based on what really matters, return on all capital employed. It seems to me the opportunity to acquire great wealth in rands and dollars is as open, perhaps more open than it has ever been given current market pessimism.

The aspirant billionaire will not have to rob the taxpayer to get rich – though it is still unfortunately the most obvious route. Yet more than a few new billionaires are hard at work proving my point that Bruce may not have noticed from his rural retreat.

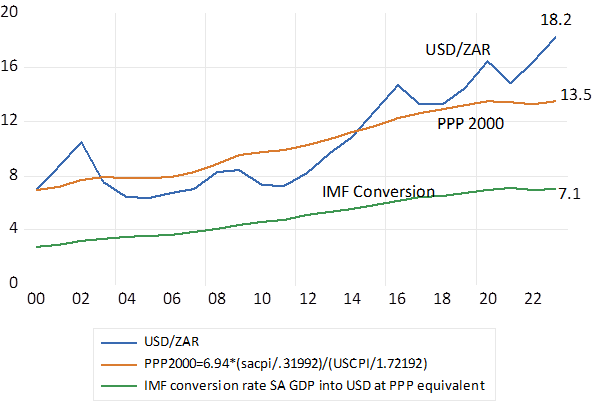

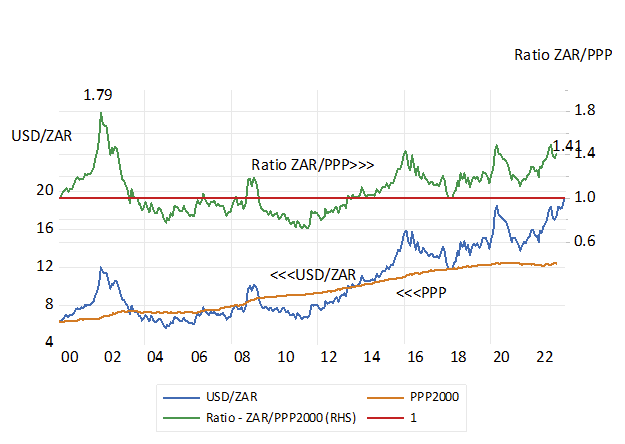

Though admittedly a billion rand today is a lower target, worth a lot less than a billion in 2000 – about 35% as much, after SA inflation. To compare purchasing power in US dollars, you might do as the IMF does – divide billions of rands by 7 not 19 to convert SA GDP into purchasing power dollar equivalents. If the rand just compensated for differences in SA and US inflation since 2000, a dollar would cost R13.5 and a billion rand would buy the equivalent of USD74m – more than nickels and dimes.

The exchange value of the Rand (USD/ZAR) and its purchasing power equivalent

The group of countries that will make up the enlarged BRICS, Argentina, Egypt, Ethiopia, Iran, Suadi Arabia and the UAE have little in common other than a deep suspicion of the motives of the US and its close allies. A state of mind also shared by left wing opinion everywhere including in the US itself. If the unlikely combination of kingdoms, autocracies and genuine democracies is to become more than a another talking shop with an anti-West bias, then it should take an important lesson from the economic development of the US and Europe.

What has been of great benefit to the US and to Europe, since it established a common European market and Euro are their highly significant common currency areas. The same money is used everywhere in the US and Europe as a medium of exchange and a unit of account. Thus unpredictable rates of exchange when buying or selling goods and services across frontiers are avoided, as are the direct costs of converting one currency into another- usually converting US dollars -into the domestic money.

Trade and financial flows between the states of the US and now of Europe is greatly encouraged by what is a fixed exchange rate regime within a common market, also free of protective of domestic industry tariffs or discrimination against foreign suppliers, by regulation. As it does incidentally when transactions of one kind or another take place within any country. The important trade between Gauteng and the Western Cape for example is facilitated by prices set in the rand common to both.

In the nineteenth century when which international trade and finance first flourished and economies came to benefit from wider markets for their goods and labour, and the ability to realise productivity and income enhancing economies of scale, currencies were mostly linked by fixed rates of exchange. The link was the ability to convert the different monies, if necessary, into gold at a fixed rate. And the issuers of different monies made sure to maintain convertibility by protecting their balance of payments through adjusting domestic interest rates. If gold generally flowed out interest rates could be raised to conserve and attract gold reserves and vice versa. Provided the commitment to currency convertibility was fully credible, the extra interest received would balance the payments by attracting or retaining capital.

A modified fixed exchange rate system was re-established after the second world war with the US dollar as the reserve currency- but dollars that could be converted into gold at the request of other central banks. This commitment was abandoned unilaterally by the US in 1971 and market determined exchange rates, with the still dominant US dollar, became the norm. Highly variable rather than predictably fixed exchange rates have become the unsatisfactory order of the day. The rates of exchange of other currencies with the dollar, both in money of the day terms and when adjusted for differences in inflation of different currencies have varied very significantly – and unpredictably- damaging volumes of international trade and real investments.

US Dollar Exchange Rate Index. Market Determined and Inflation Adjusted

Source; Bloomberg, Federal Reserve Bank of St.Louis and Investec Wealth and Investment

It has not been a case of exchange rate moves levelling the playing field for traders in goods and services- so maintaining purchasing power parity in the face of differences in inflation rates across trading partners. Rather the exchange rates have adjusted to equilibrate independent flows of capital – large and reversible flows – in search of better risk adjusted rates of return- to which inflation then responds. Weaker exchange rates lead to more inflation and vice versa. Without stable exchange rates, controlling inflation in the face of capital withdrawals and a suddenly weaker exchange rate with the US dollar can become a severe interest rate burden on the domestic economy – as South Africa demonstrates.

The enlarged BRICS could establish fixed exchange rates between each other to promote trade and investment. They might usefully adopt a Chinese standard- that is offer convertibility of their own currencies into Renminbi at fixed rates. And rely on the Bank of China to manage the float of the crucial rate of exchange of Renminbi into US dollars, as it now does.

There is a certain balance of payments (BOP) outcome. That the dollar payments and dollar receipts in the currency market will strictly balance over any period- an hour, day quarter or year. The exchange rate and interest rates will continuously adjust to make it so- to equalize supply and demand for dollars and other currencies traded. And it is a very good idea for the authorities not to intervene in or attempt to influence this market determined exchange rate with interest rate adjustments. Or to directly control demands for or supplies of foreign currencies to achieve a temporarily better, perhaps less inflationary rate of exchange. A shadow market will emerge to siphon off undervalued dollars, leading to an official scarcity of dollars. Making it very difficult to do normal helpful income enhancing business across the frontiers and discouraging to foreign investment so important to any economy. As MTN knows only to well from its experience in Nigeria.

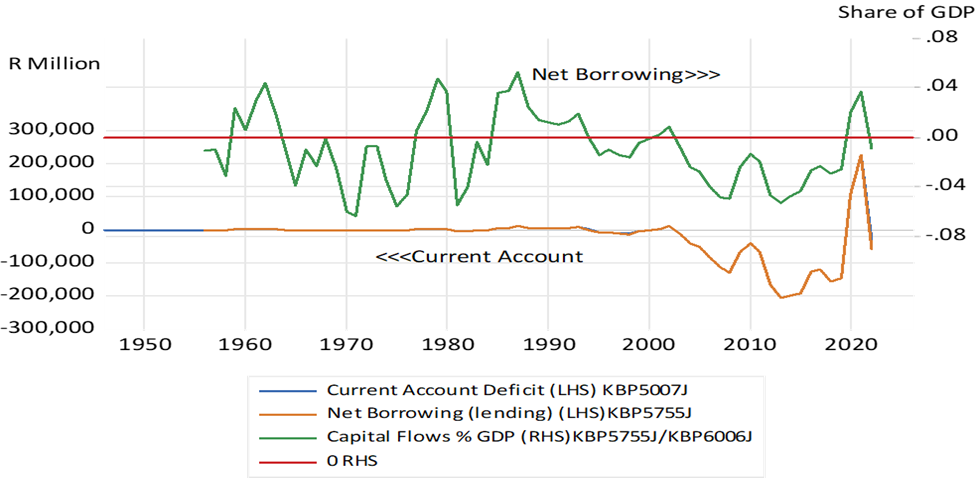

Another BOP relationship will also always hold. The current account of the BOP- that measures payments and receipts for imports, exports and the flows of dividends and interest paid or received by South Africans, will always be matched equally and oppositely by what are measured as flows of capital over the exchanges. A current account deficit will always be matched by a capital account surplus of the same amount and vice versa. There is no cause-and-effect relationship implied by this identity. The current account does not determine the capital flows – any more than the capital flows determine net flows of foreign trade, interest, and dividend payments. It is an accounting identity.

The capital and current accounts- an identity, identified.

Source; SA Reserve Bank and Investec Wealth and Investment

Over most years the current account of the SA balance of payments has been in deficit. Exports of goods and services almost always exceed imports – generating a consistently positive balance of trade (BOT) While the deficit on what might be described as the asset service account, dividends and interest payments, almost always exceeds dividend and interest received by enough to exceed the positive BOT. The interest and dividend yields on SA liabilities much exceeds the dividend and interest yield on SA assets held abroad. But between 2020 and 2022 South Africa ran current account surpluses and exported capital on a significant scale. So much so that the market value of SA assets held offshore now exceeds that of the market value of foreign owned assets in SA. This was not good for the South African economy.

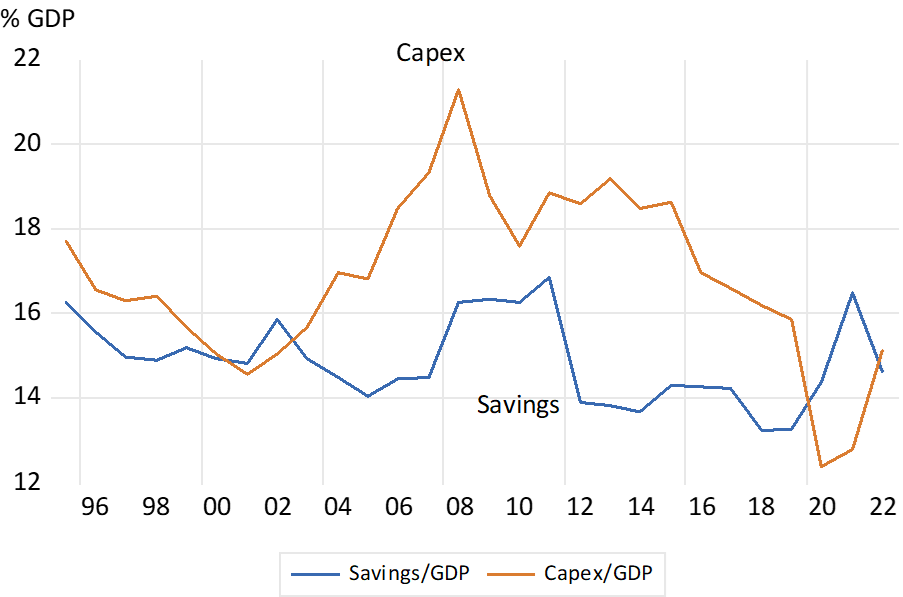

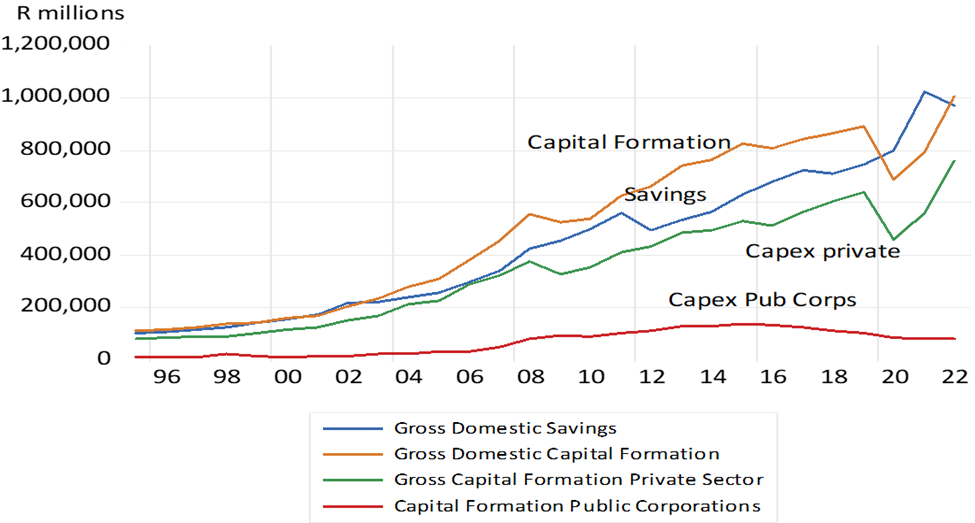

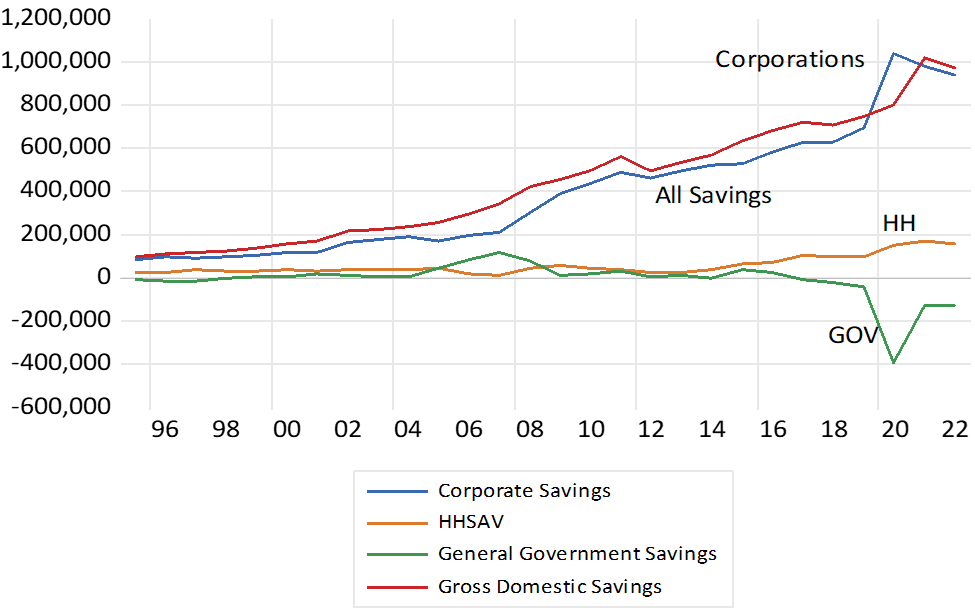

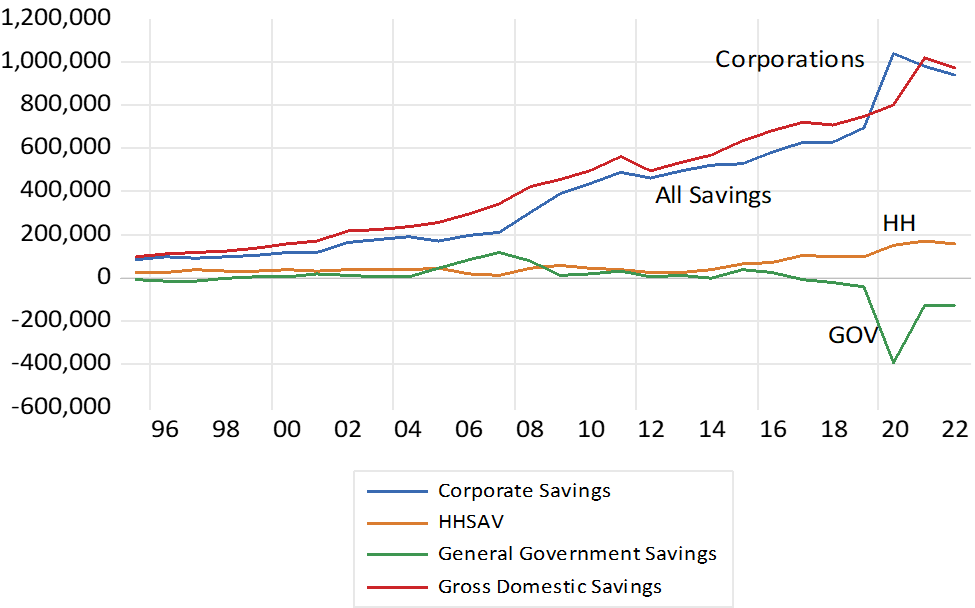

There is a National Income Accounting Identity to help make the point. The current account deficit also equates to the difference between Aggregate Incomes that are equal to Aggregate Output (GDP) and Total Expenditure on final goods and services (GDE) It is also by definition the difference between Gross Savings and Gross Capex. Post Covid, Gross Savings, almost all in the form of cash retained by the corporate sector, held up better than Capex and capital – from a capital starved economy – flowed out.

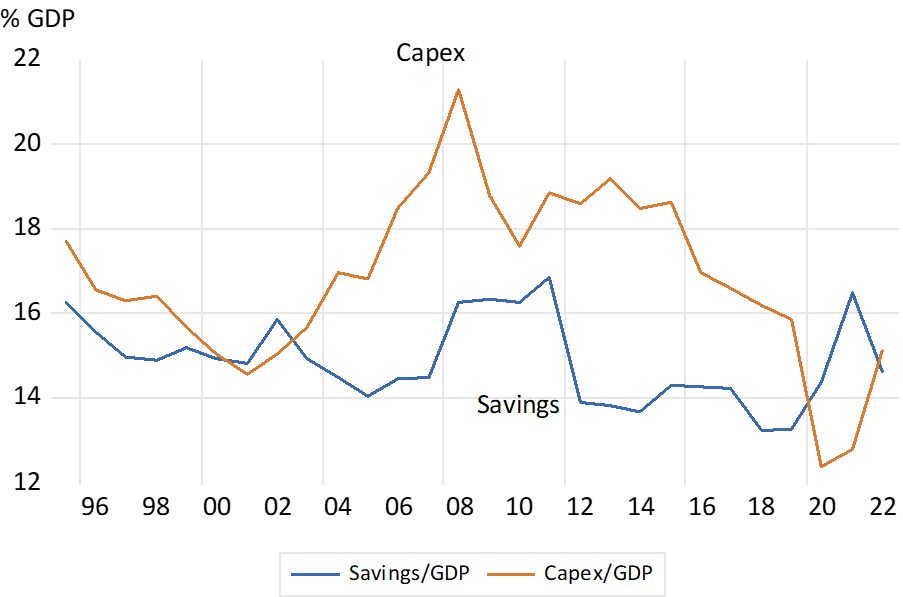

South Africa, Gross Savings and Capital Formation – Ratio to GDP – Annual Data, Current Prices

Source; SA Reserve Bank and Investec Wealth and Investment

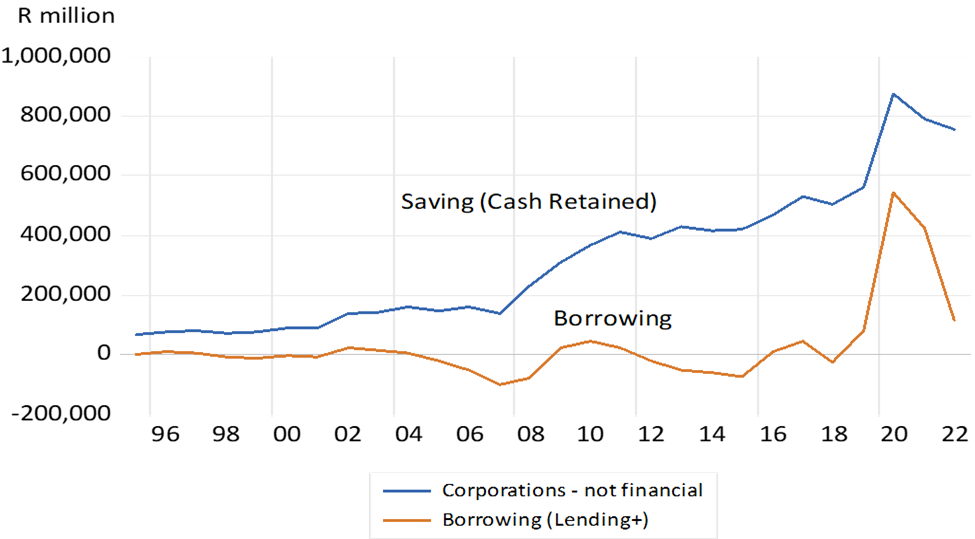

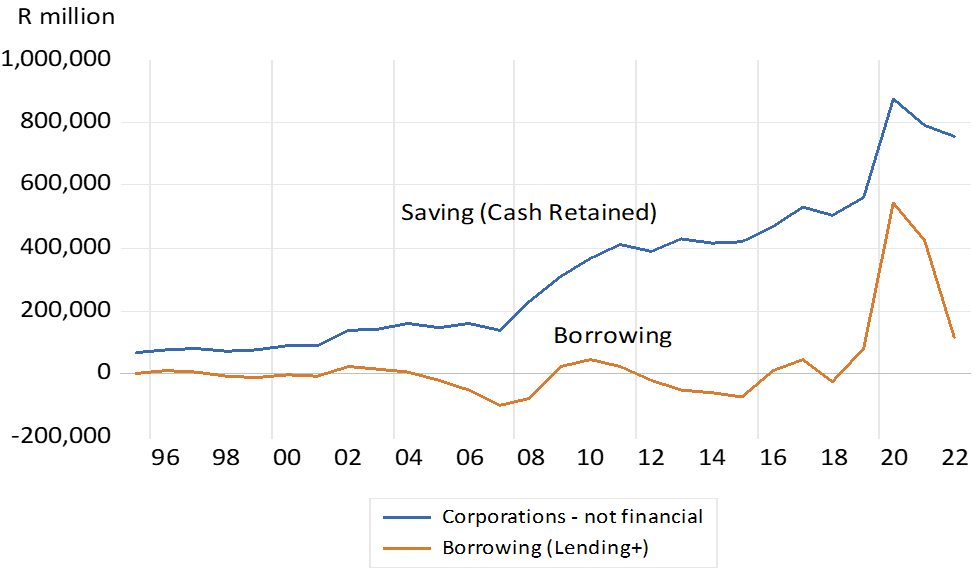

South African Non-Financial Corporations; Cash from Operations Retained and Net Lending (+) or Borrowing (-) Annual Data

Source; SA Reserve Bank and Investec Wealth and Investment

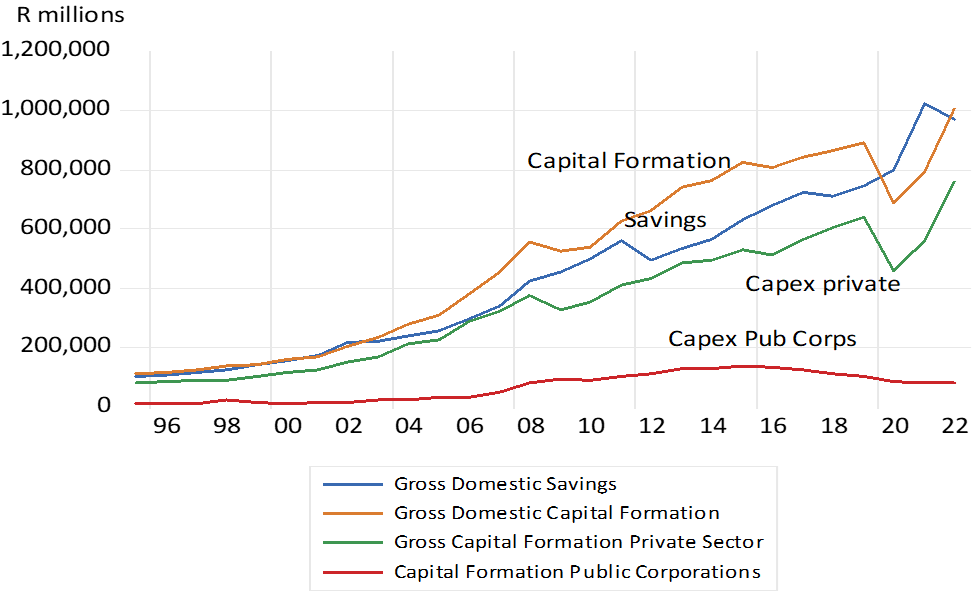

South Africa; Gross Savings and the Composition of Capital Expenditure by Private and Publicly Owned Corporations

Source; SA Reserve Bank and Investec Wealth and Investment

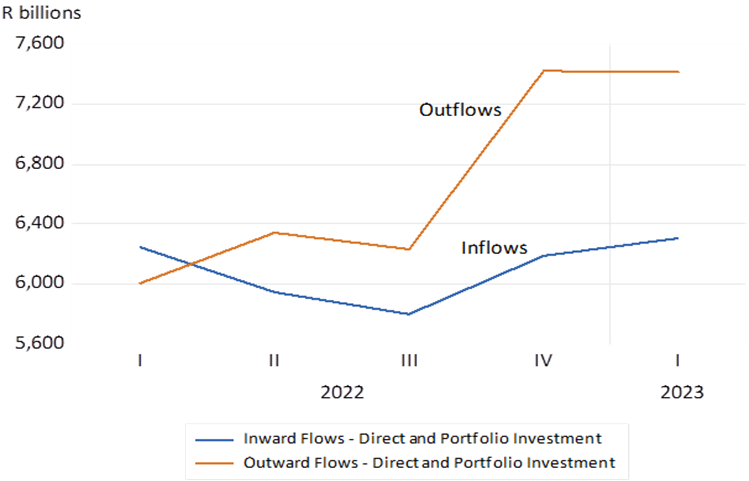

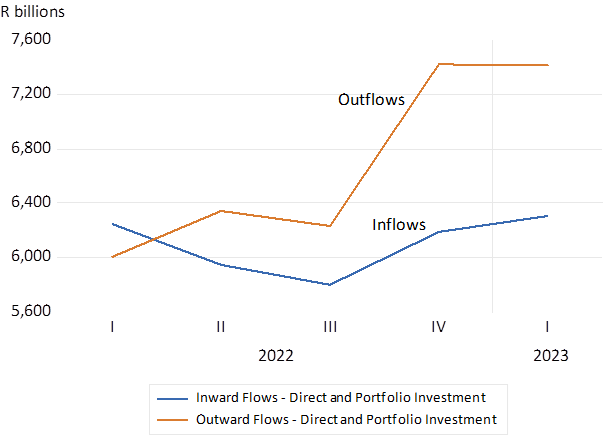

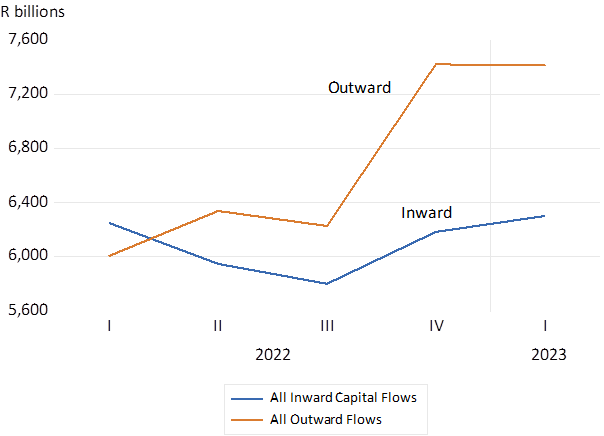

South Africa; Inflows and Outflows of Capital; Direct and Portfolio Investment. Quarterly 2022-2023

Source; SA Reserve Bank and Investec Wealth and Investment

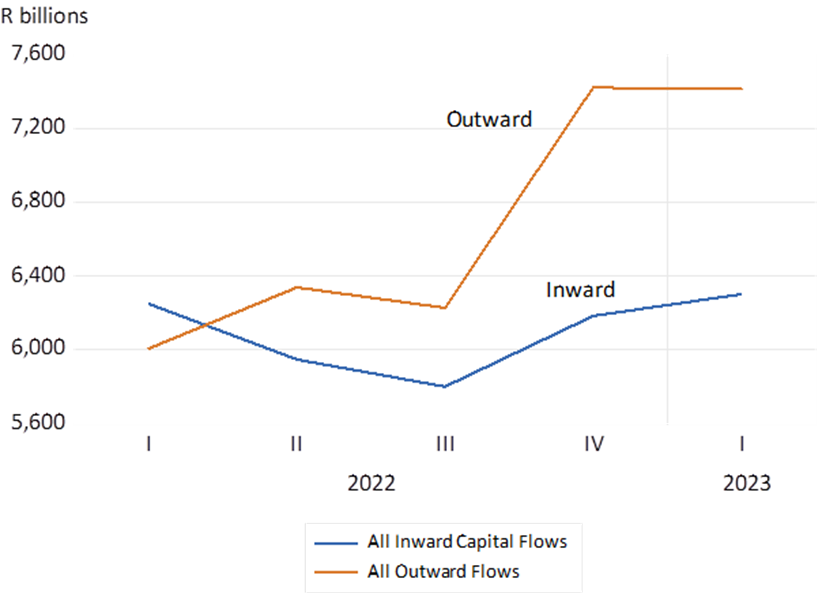

All Capital Flows to and from South Africa; Quarterly Data (2022.1 2023.1)

Source; SA Reserve Bank and Investec Wealth and Investment

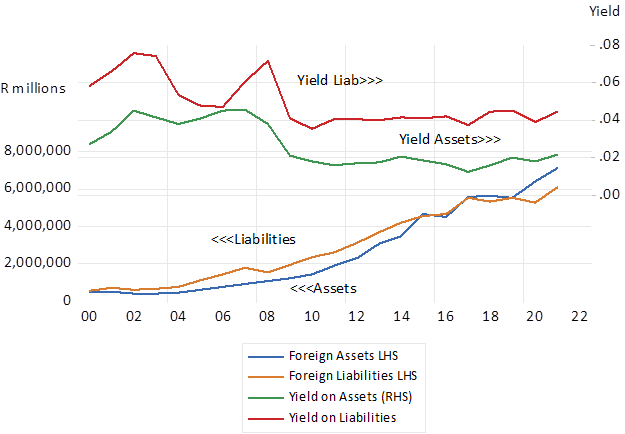

SA; Total Foreign Assets and Liabilities; Direct and Portfolio Investments and Yield

Source; SA Reserve Bank and Investec Wealth and Investment

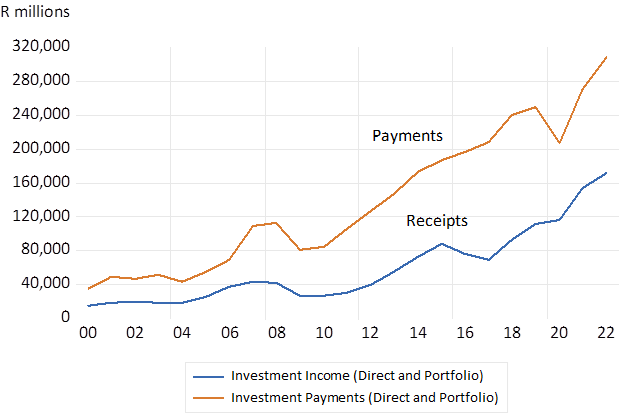

SA Foreign Investment Income (Dividends + Interest) Annual Data

Source; SA Reserve Bank and Investec Wealth and Investment

South Africa; Gross Savings Annual Data (R millions)

Source; SA Reserve Bank and Investec Wealth and Investment

Both the ratio of Gross Savings – and Capex to GDP can be regarded as unsatisfactorily low in SA. The opportunity to raise the savings rate seems limited, given low average incomes. However, the opportunity to raise the rate of capex to GDP and to attract foreign capital to fund income growth encouraging capex and the accompanying larger current account deficits is always open. SA must be able to offer faster growth and the accompanying higher expected returns, to attract more foreign capital and to retain a greater share of domestic savings.

Supply side reforms are urgently needed for the SA economy. We all know what they are. Demand will keep up with supply automatically. Extra Supply – extra incomes earned producing more goods and services- creates its own demands. Yet until the economy can deliver more growth and better returns, the best we can do with our savings is to invest them abroad. (including buying shares of companies listed on the JSE that do almost all of their business outside the SA economy) Without such opportunities, the pension and retirement funds, upon which we depend for our future income, would be in a truly parlous state.

I wrote as following in a letter to the Wall Street Journal in response to an op-ed piece by John Cochrane a formidable youngish economist very much in the Chicago School tradition – where he was a professor. He is now a Senior Fellow at the Hoover Institution. You can follow his blog Blog: http://johnhcochrane.blogspot.com/

Incidentally I have not yet had any acknowledgment from the WSJ – nor do I expect them to publish my letter.

Here is an answer to Cochrane’s (WSJ, August 1st ) question – … does money alone drive inflation? Money (mostly) in the form of deposits in banks held by households and by firms, on behalf of their shareholders, is clearly an asset of the depositor and a component of their wealth. Because the deposit liabilities issued by the shareholders of banks are not expected to be repaid (net wealth goes up with bank deposits because they are expected to grow with the economy and the demand for deposits and will not have to be repaid or be expected to be repaid). Similarly as Cochrane posits, government bonds, or any paper issued by a government, that are never expected to be repaid by taxpayers, are another component of wealth. An excess supply of net money (deposits) or an excess supply of net bonds- over and above the willingness of wealth owners (savers) to hold those assets –would lead to an increase in the demand for other assets and goods and services- and so generally higher prices for goods, services and other assets as portfolios are adjusted to excess holding of money or bonds. That is lead to inflation.

But where could the excess supplies of money and or bonds come from? As Cochrane indicates only and always from a fiscally undisciplined government. A fiscal theory of inflation is essential in explaining all inflations everywhere. It is hardly an original concept.

A fiscally constrained government can call on its central bank and its private banks to fund all the bonds it wishes to issue. The central bank most simply might directly fund the government by buying its additional paper and crediting the government’s deposit account with it. Which, as the Treasury deposits with the central bank run down as the government spends more, would increase the cash reserves of the banks. And their ability and perhaps willingness to lend more- including to the government. And if extra bank lending ensued by banks flush with extra cash, the supply of bank deposits would increase by a multiple of the additional cash deposits injected into the system.

Or the central bank could at its initiative supply (lend) extra cash to the banks so that they may be willing to fund the government with the same influence on the supply of bank deposits as the government spends more. And if the increase in the supply of deposits – bank liabilities and of government paper – bank assets – exceeded the willingness of the public to add to their deposits or bonds – inflation would follow. The deposit liabilities of the banks and their loans to government (bonds) would be increasing at a similar rate. The banks, perhaps more than a wider set of financial institutions, would be holding many of the extra bonds issued by governments- particularly in many countries mostly without a well-developed bond market but very vulnerable to fiscal difficulties and high rates of inflation. Inflation is not an American invention.

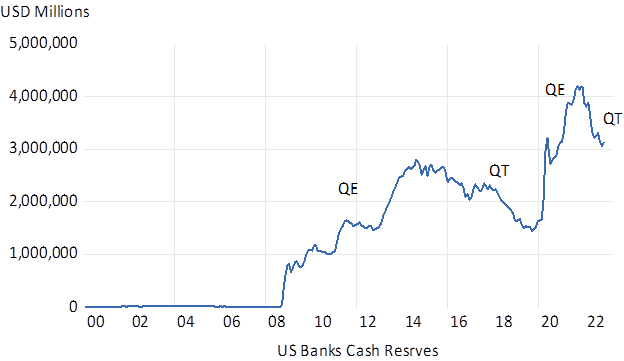

Inflation is explained by the inter- actions of governments, banks and the wealth owning public. The exchange of a hugely increased supply of extra deposits held by US banks with the Fed (QE) (cash) for extra private or publicly issued securities after 2010 was restrained – it was understandably not a risk loving lending encouraging time for the US banks after the GFC. The money multiplier (M2/Cash Reserves) collapsed – and the supply of deposits grew slowly and more or less in line with the demand for extra deposits issued by the banks, so avoiding much inflation. But not incidentally of share or real estate prices that were on a tear. Predicting inflation will always demand a close watch of fiscal policy – of the supply of and demand for government bonds in wealth portfolios – and of the behavior of banks- central and private. It will always be complicated.

The case for a company buying back its own shares is clear enough. If the shareholders can expect to earn more from the cash they could receive for their shares than the company can expect to earn re-investing the cash on their behalf, the excess cash is best paid away.

Growing companies have very good use for the free cash flows they generate from profitable operations. That is to invest the cash in additional projects undertaken by the company that can be expected by managers to return more than the true cost of the cash. This cost, the opportunity cost of this cash, is the return to be expected by shareholders when investing in other companies. Such expected returns, a compound of share price gains and cash returned, are often described as the cost of capital. And firms can hope to add wealth for their shareholders when the internal rate of return realized by the company from its investment decisions exceeds the required returns of shareholders.

All firms, the great and not so good, will be valued to provide an expected market competing rate of return for their shareholders. Those companies expected to become even more profitable become more expensive and the share prices of the also rans decline to provide comparable returns. How then can a buyback programme add to the share market value of a company? Perhaps all other considerations remaining the same- including the state of the share market, the share price should improve in proportion to the reduced number of shares in issue. But far more important could be the signaling effect of the buy backs. Giving cash back to shareholders, especially when it comes as a surprise, will indicate that the managers of the company are more likely to take their capital allocating responsibilities to shareholders seriously.

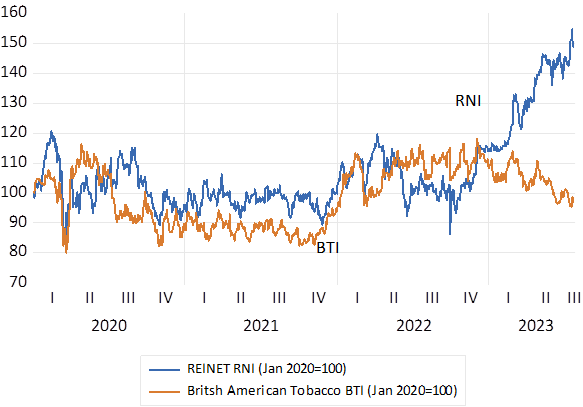

The case of Reinet (RNI) the investment holding company closely controlled by Mr. Johann Rupert is apposite. Mr. Rupert believes the significant value of the shares bought back by Reinet have been “cheap” because they cost less than their book value or net asset value (NAV) Yet the market value of Reinet still stands at a discount to the value of its different parts and may continue to do so. Firstly, shareholders will discount the share price for the considerable fees and costs levied on them by management. Secondly, they may believe the unlisted assets of Reinet may be generously valued in the books of RNI, so further reducing the sum of parts valuation suggested by the company and reducing the value gap between true adjusted NAV and the market value of the holding company. Finally, the market price of RNI has been reduced because the returns realized by the investment programme of RNI may not be expected to beat their cost of capital and will remain a drag on profits and return on capital. Therefore the value of the holding company shares is written down – to provide market competing, cost of capital equaling, expected returns- at lower initial share prices. And realizing a difference between the NAV reported by the holding company (its sum of parts) and the market value of the company – share price multiplied by the number of shares in issue (net of the shares bought back)

Yet for all that, the shares bought back may prove to be cheap should Reinet further surprise the market with further improvements in its ability to allocate capital. And the gap between NAV and MV could narrow further because the value of its listed assets decline. Indeed, shareholders should be particularly grateful for the recent performance of RNI when compared to the value of its holding in British American Tobacco (BTI) its largest listed investment. RNI has outperformed BTI by 50% this year. Unbundling its BTI shares – an act normally very helpful in adding value for shareholders because it eliminates a holding company discount attached to such assets- would have done shareholders in RNI no favours at all this year.

Fig.1; Reinet (RNI) Vs British American Tobacco (BTI) Daily Data (January 2020=100)

Source; Iress and Investec Wealth and Investment

The recent trends in flows of capital out of and into businesses operating in SA are shown below. It may be seen that almost all the gross savings of South Africans consist of cash retained by the corporate sector, including the publicly owned corporations. (see figure 2) Though their operating surpluses and retained cash have been in sharp recent decline for want of operational capabilities and revenues rising more slowly than rapidly increasing operational costs. Their capital expenditure programmes have suffered accordingly as may be seen in figure 3. The savings of the household sector consist mostly of contributions to pension and retirement funds and the repayment of mortgages out of after-tax incomes. But these savings are mostly offset by the additional borrowings of households to fund homes, cars, and other durable consumer goods. The general government sector has become a significant dissaver with government consumption expenditure exceeding revenues plus government spending on the infrastructure. It may be noticed that the non-financial corporations in South Africa have not only undertaken less capital expenditure with the cash at their disposal- they have also become large net lenders- rather than marginal borrowers- in recent years. (see figure 5)

Fig.2; South Africa; Gross Savings Annual Data (R millions)

Source; South African Reserve Bank and Investec Wealth and Investment

Fig.3; South Africa; Gross Savings and the Composition of Capital Expenditure by Private and Publicly Owned Corporations

Source; South African Reserve Bank and Investec Wealth and Investment

In recent years, during and post the Covid lock downs, total gross saving has come to exceed capital; formation providing for a net outflow of capital from South Africa. Rather a lender than a borrower might be the Shakespearean recipe, but the problem is that both gross savings and capex in South Africa commands a comparably small share of GDP as shown below. South Africans save too little it may be said for want of income to do so. But they invest too little in plant and equipment and the infrastructure that would promote the growth in incomes, consumption and savings. The source of capital exported is that the gross savings rate held up while the ratio of capex to GDP fell away significantly.

Fig.4; South Africa, Gross Savings and Capital Formation – Ratio to GDP – Annual Data, Current Prices

Source; South African Reserve Bank and Investec Wealth and Investment

Fig. 5; South African Non-Financial Corporations; Cash from Operations Retained and Net Lending (+) or Borrowing(-) Annual Data

Source; South African Reserve Bank and Investec Wealth and Investment

The reason many SA companies are buying back shares on an increasing scale is the general lack of opportunities they have had to invest locally with the cash at their disposal. And the cash received has been invested offshore rather than onshore on an increasing scale. For want of growth in the demand for their goods and services for all the obvious reasons. As a result the aggregate of the value of South African assets held abroad at march 2023 exceeded those of the foreign liabilities of South Africans, at current market valuations, by R1,699 billion. Total foreign assets were valued at approximately 9.5 trillion rand.

Fig 6; South Africa; Inflows and Outflows of Capital; Direct and Portfolio Investment. Quarterly Flows 2022.1 – 2023.1[i]

Source; South African Reserve Bank and Investec Wealth and Investment

Fig.7; All Capital Flows to and from South Africa; Quarterly Data (2022.1 2023.1)

Source; South African Reserve Bank and Investec Wealth and Investment

The reluctance to invest in SA makes realizing faster growth ever more difficult. That the cash released to pension funds and their like is increasingly being invested in the growth companies of the world, rather than in SA business, is the burden of a poorly performing economy that South Africans have to bear. Rather a borrower than a lender be- if the funds raised can be invested in a long runway of cost of capital beating projects. Faster growth in the economy would lead the inflows of capital and restrain the outflows of capital required to fund a significant increase in the ratio of capital expenditure to GDP and a highly desirable excess of capex over gross savings.

[i] The investments are defined as direct when the flows are undertaken by shareholders with more than 10% of the company undertaking the transactions. And as portfolio flows when the shareholder has less than 10%. Much of the economic activities of directly owned foreign companies in South Africa, including their cash retained and dividends paid to head office will be regarded as direct investment. For example, describing the activities of a foreign owned Nestle or Daimler Benz in SA.

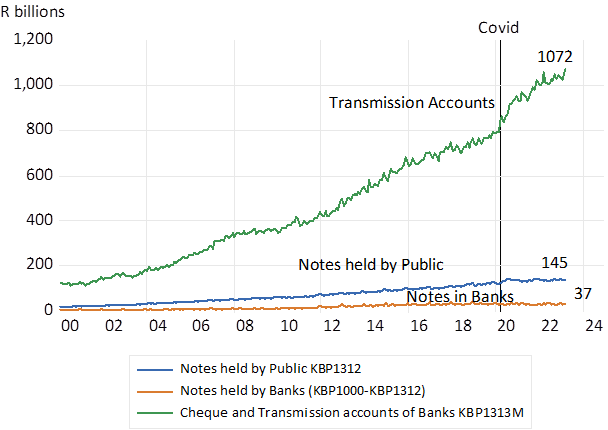

Starbucks has a prominent notice. Responsibly Cashless. It might have read better or more honestly as profitably cashless. Avoiding the costs and dangers of handling and transporting cash and the associated bank charges – including the likelihood of cash not making it to the till in the first instance – will surely be in the owner’s interest and justifiably so. On the proviso that the sales lost would not be at all significant as affluent and tech savvy customers tender their telephones. It is not a conclusion the owner manager of a small stand-alone enterprise in control of what goes in or out of the cash register will come to. For them cash is still king.

Starbucks and other cash refusers are probably within its rights refusing legal tender. Only the notes and coins issued by the Reserve Bank qualify as legal tender in SA – money that cannot be refused in proposed settlement of a debt. But presumably can be rejected when offered in exchange for a good or service. SARS would probably approve of a cashless society for obvious income monitoring purposes. The Reserve Bank might, were it a private business, have mixed feelings about reducing the demand for a most valuable monopoly. It pays no interest on the notes it issues and earns interest on the assets the note liabilities help fund. In 2004 the note issue funded 40% of the Assets on the Reserve Bank. That share is now down to 15%. It was 20% before Covid.

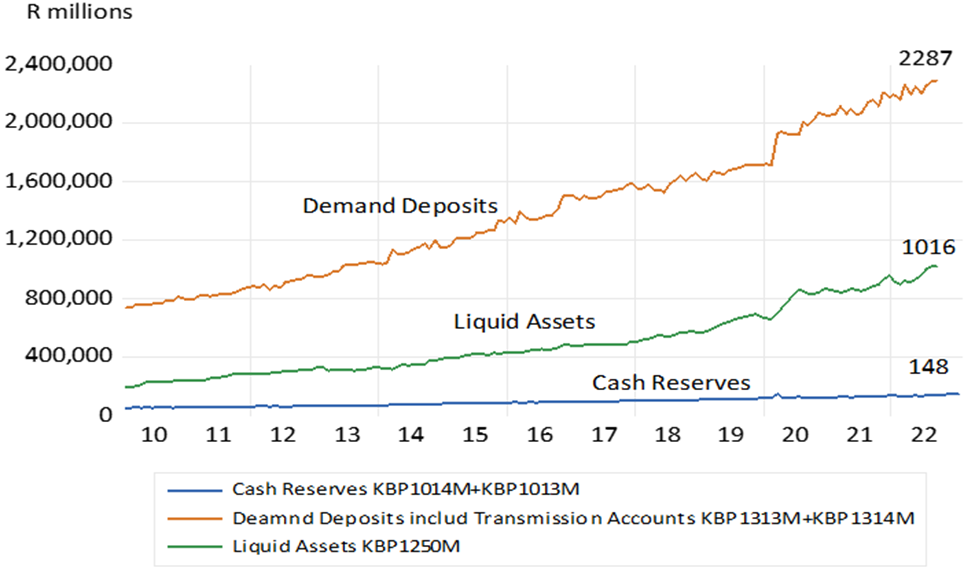

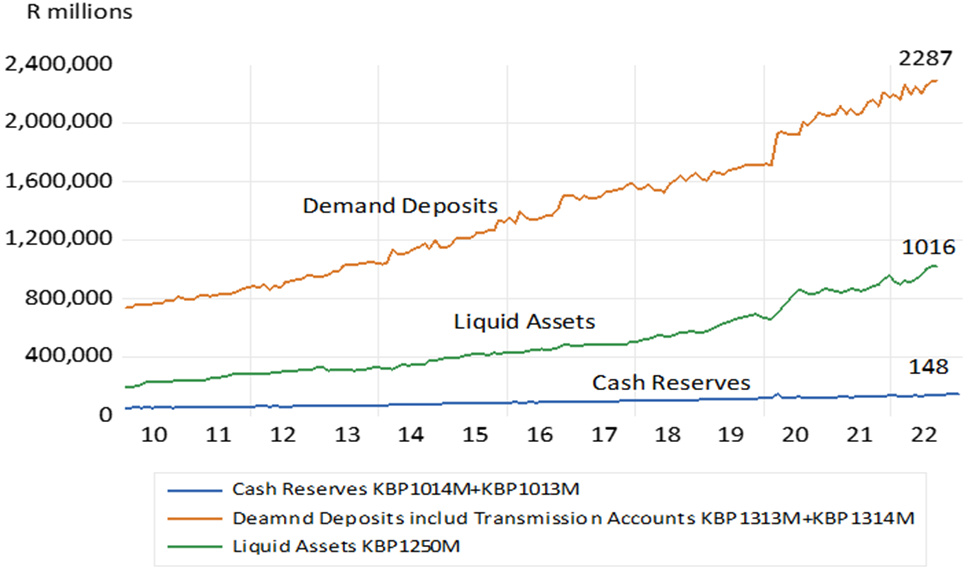

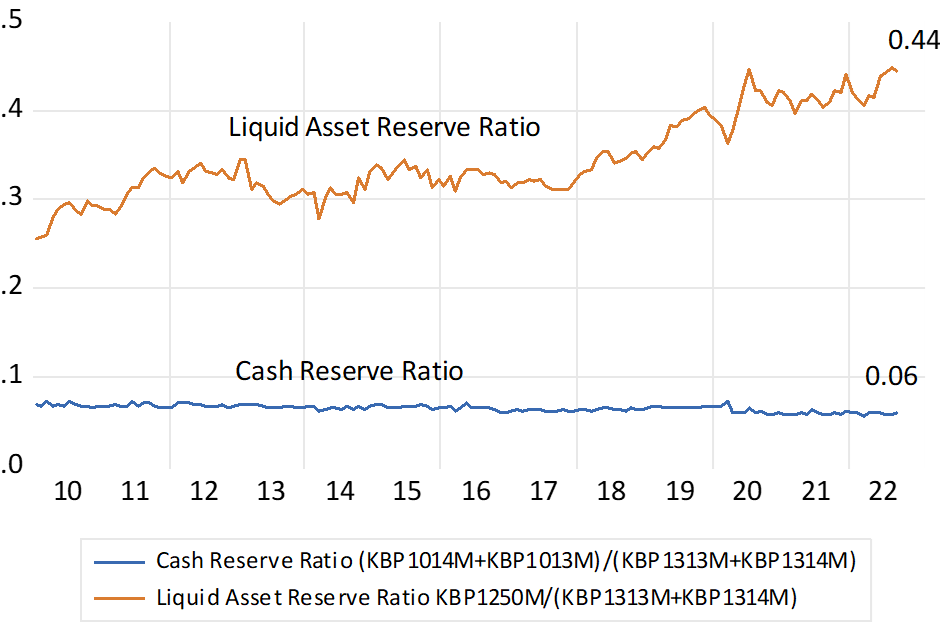

Clearly notes, have lost ground to the digital equivalent- a transfer made and received via a banking account. A trend that becomes conspicuous after the Covid lockdowns. Since then, the transmission and cheque accounts at SA banks have grown very strongly from R790 billion in early 2020 to nearly 1.1 trillion today- or by about a quarter. By contrast the notes issued by the Reserve Bank since have increased only marginally – by R20b – with most of the extra cash issued being held by the public. The private banks have managed to reduce their holdings of non-interest bearing cash in their vaults and ATM’s. By closing branches and ATM’s and retrenchments. Replacing notes with digits- have been a cost saving response. A central bank replacing paper notes with a digital alternative could be an alternative. But it would be very threatening to the deposit base of the private banks and their survival prospects.

South Africa; Money Supply Trends.

Source; SA Reserve Bank and Investec Wealth and Investment

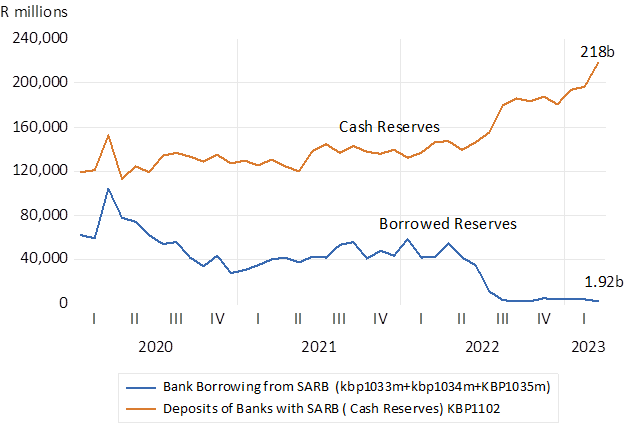

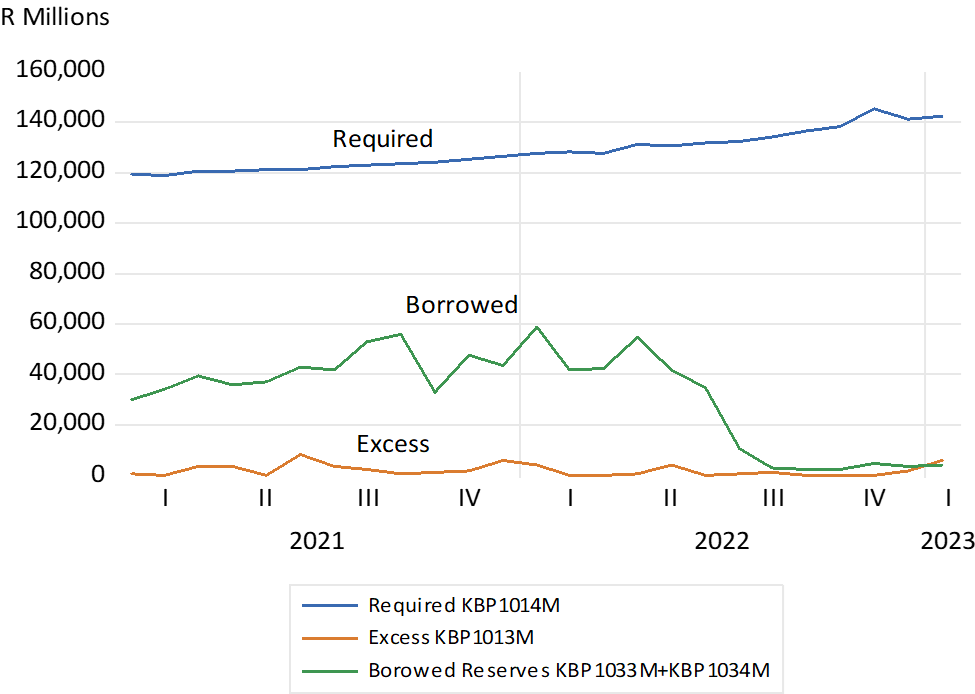

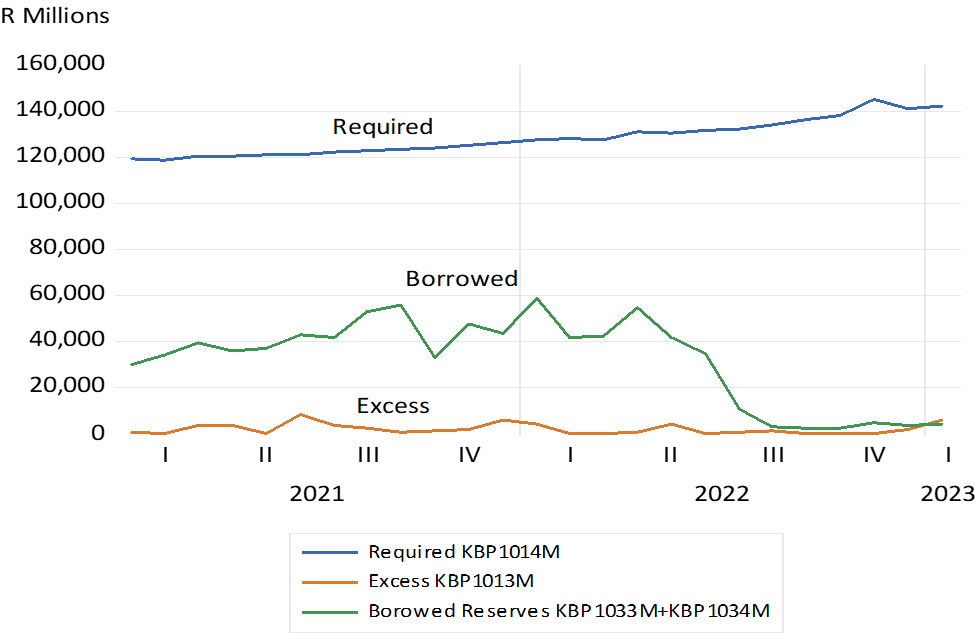

The Banks in SA have however dramatically increased their demands for an alternative form of cash- deposits with the Reserve Bank. They now earn interest on these deposits. What used to be significant interest charged to the banks when they consistently borrowed cash from the SARB – to satisfy the cash reserve requirements set by the SARB – at the Repo rate- has now become interest to be earned on deposits held with the SARB. These deposits have grown by R100bilion since 2020 while cash borrowed from the SARB has fallen away almost completely from an earlier average of about R50 billion a month.

SA Banks – demand for and supply of cash reserves since Covid

Source; SA Reserve Bank and Investec Wealth and Investment

The SARB, following the Fed, regards the interest it pays on these deposits as fit for the purpose of preventing banks from converting excess cash into additional lending. Which would lead to increased supplies of money in the form of additional bank deposits. It takes a willing bank lender and a willing bank borrower to power up the supply of cash supplied to the banking system by a central bank into extra deposits The testing time for central banks in a banking world full of cash will come when increased demands for bank credit accompany the improved ability and willingness of the banks to turn excess cash into extra bank lending. Then interest rate settings may not control the demand by banks for cash reserves to sufficiently restrain the conversion of excess cash into additional bank lending, that in turn will lead to extra and possibly excess supplies of money and so extra spending as money is exchanged for goods, services and other assets, that will force prices higher. Clearly not for now the banking state of SA or of the US where the supply of money is in sharp retreat.

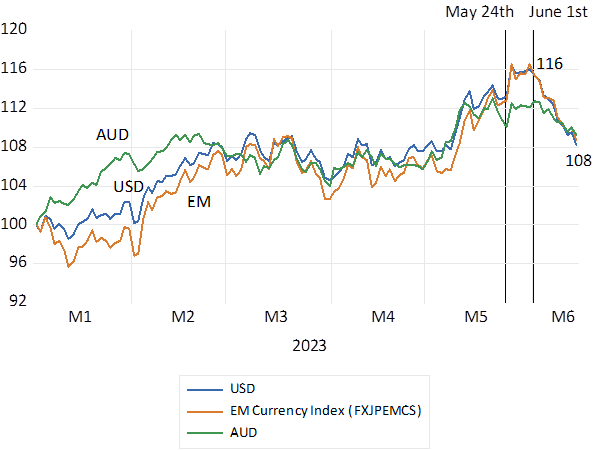

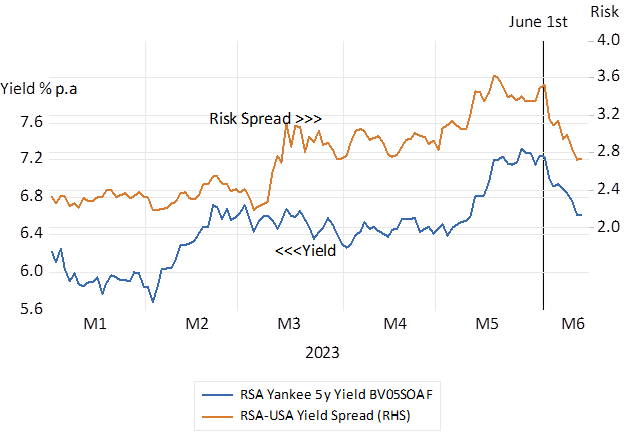

The rand has recovered strongly this month – by about 7% against the US dollar, and has performed similarly Vs the Aussie dollar and an index of EM currencies. The rand had weakened through much of 2023. It weakened by a further 3% when the SARB increased rates unexpectedly sharply by 50 b.p. on May 25th. Since June 1st the ZAR has recovered – as interest rates in SA have fallen away. arply.

The ZAR Vs The USD, the AUD and the EM Currency Index. (Daily Data January 2023=100)

Source; Bloomberg and Investec Wealth and Investment Long term RSA bond yields have declined significantly and helpfully by between 50 and 70 basis points this month. The Yankee Bond, a five year dollar denominated claim on the RSA, now yields a lower 6.4% p.a. compared to the 7% p.a. offered on June 1st. Moreover, the spread between the RSA dollar bond and a US Treasury of the same duration has narrowed significantly from 3.6% p.a to 2.8% p.a. This interest rate spread provides a very good indicator of the risks of default attached to SA bonds. More important perhaps for the direction of the rand and the economy has been the recent inflection in short-term interest rates. When the SARB raised rates on the 25th May, the money market, as represented by the forward rate agreements of the banks, immediately predicted a further one per cent hike in short rates over the next six months. The SARB is now expected to be much less aggressive. The market is now expecting short rates to rise by a quarter per cent.

RSA Dollar Denominated (5 year Yankee Yield) and the SA Sovereign Risk Premium (Daily Data 2023)

Source; Bloomberg and Investec Wealth and Investment

Why have surprisingly lower short term interest rates helped the rand as surprisingly higher rates clearly weakened the rand last month? There is much more than coincidence at work here. Higher short-term rates – higher overdraft and mortgage rates- combined with the higher prices that follow a weaker rand – are expected to further depress spending in SA and the growth outlook for the economy. The weaker the outlook for the economy, the weaker the growth in incomes before and after taxes, the more government debt is likely to be issued. And the graver becomes the eventual danger a of a debt default. For which still higher interest rate rewards have to be offered to investors to compensate them for the additional risks implied by a deteriorating fiscal condition. These higher interest rates then raise the cost of capital for SA business – making them still less likely to undertake growth encouraging capex. The Reserve Bank is ill advised to react to exchange rate shocks in ways that further threaten the growth outlook – and can prove counterproductive by weakening the rand that then lead to still higher prices. Interest rate increases make sense when excess spending – excess demand – is putting pressure on prices. Which is not the case for the SA economy today. The right response to exchange rate shocks is to ignore them as their temporary impact on the price level falls away. Absent any additional consistent pressure on prices from the demand side of the economy, over which the SARB will always have strong influence. The notion of self-perpetuating inflationary expectations, as promoted by the Reserve Bank when explaining its interest rate reactions to a weaker rand, is supported neither by evidence nor is it consistent with self-interested economic behaviour. It is poor theory and even poorer practice. But this leaves open the question- why then have interest rates come down in SA? The answer can be found offshore. The Fed has found good reason not to push its own rates higher. The pause on rate increases in the US became widely expected and was confirmed yesterday gives the SARB even less reason to raise its own interest rates. The Fed by dealing effectively with a surge in inflation (which has not been self-perpetuating) has improved the outlook for interest rates, the SA economy and the rand.

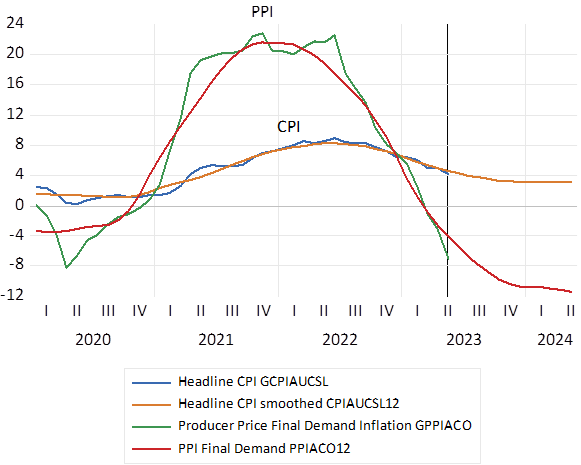

Update on US Inflation – to May 14th 2023.

Both CPI (4.0%) and PPI headline inflation fell more than expected in May. Monthly moves were low – 0.2% for CPI and negative for PPI. The only proviso was the elevated rate 0.4% m-m for core CPI- CPI excluding energy and food. But core has a very large rental weight- over 40% which was up 8% y/y – but rentals are clearly heading lower and core may not be the most useful leading indicator for CPI – PPI- now strongly lower may do much better in predicting CPI. The Fed paused but member dot plots indicated further increases to come. But the Chairman says the Fed will remain data dependent and my view is that the Fed panic about inflation is over. Because demand pressures on inflation are largely absent- thanks to higher interest rates and negative growth in money supply and bank credit. The global pressure on interest rates in SA is therefore abating. As discussed in my commentary above

US Headline Inflation Y/Y growth in Index

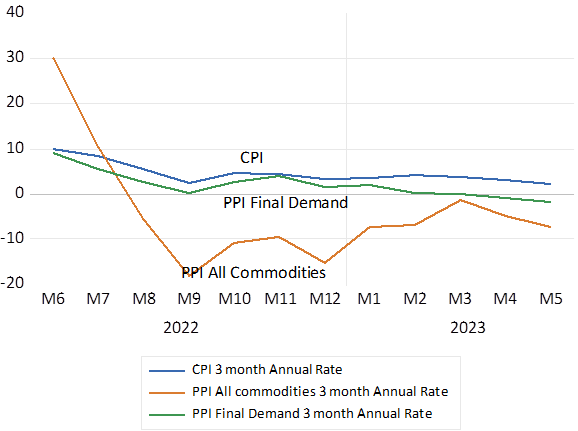

US Inflation over the past three months – % per 3 months annualized. CPI now running at a quarterly rate of 2%. PPI inflation – headline and quarterly- is now negative

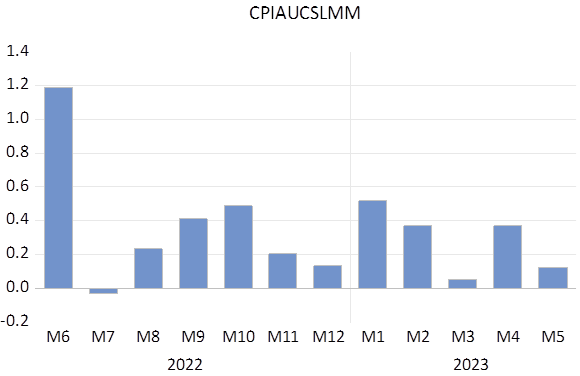

Monthly % move in CPI Seasonally Adjusted. Latest April-May 2023=0.12%.

Chat GPT has been an overnight sensation in the world of internet dependents – that is most of us. Though as any overnight sensation would attest – it takes a lifetime of sacrifice and investment to become that overnight sensation. As has surely been the case with the application of Generative Artificial Intelligence. Huge investments have been made – are being made – in developing and applying AI. And the great IT firms are leading the way with their impressive operating margins and returns on capital and abundance of cash flow invested in clouds of computers . They profitably supply the indispensable picks and shovels at the frontiers of knowledge.

And much of their heavy R&D is in the form of employment benefits for their army of researchers – increasingly applying AI – to answer the questions their customers and colleagues ask of them- and answer them far more effectively and rapidly. Among the important applications of AI is in the writing of the code that animates software and its development. With AI the applications and adaptations – the answers to the coders – comes much more rapidly. And the R&D is mostly expensed through the income statement and may not appear on the balance sheet. But will attract great value from the investors who determine the share price of the IT giants who dominate the market value of the S&P 500. Understandably so given the promise of AI. Perhaps the most important question shareholders should now be asking their managers is how are you adapting to AI?

It is estimated that a fifth of the time of office workers is spent answering enquiries of one kind an another. Imagine AI as that true expert on the customer or the internal functions and operations of your company always sitting beside you and your laptop, and comfortably speaking and understanding your language. You will have clearer answers and immediate answers to the questions. Better still the expert may help you ask better more imaginative and important questions- the answers to which will follow. It is asking the right questions that lead advances in science. Humans will be needed for that.

McKinsey has attempted to measure the potential of AI from the bottom up so to speak. By examining in detail how AI is now and could be adopted in the workplace. They have come up with very imposing estimates of extra GDP and of faster rates of change of output and productivity. Which is output volumes divided by numbers of work hours producing them. To quote Bloomberg on the McKinsey study “ Whole swathes of business activity, from sales and marketing to customer operations, are set to become more embedded in software — with potential economic benefits of as much as $4.4-trillion, about 4.4% of the world economy’s output — according to the study by McKinsey’s research arm…….Depending on how the technology is adopted and implemented, productivity could increase 0.1%-0.6% over the next 20 years, it found….”

A follow up question is worth asking. How well will the growth in productivity show up in the numbers we use to measure output and productivity and its growth? One of the puzzles economists have been wrestling with for many years is the apparently persistently slow growth in productivity recorded over many years despite conspicuous automation and labour saving. Are we entering a new phase of productivity improvements – almost certainly – but to recognize them we will need superior techniques to measure them.

We measure the value rather than the volume of production. Revenues recorded are prices charged in money of the day, multiplied by the quantity of goods and service supplied- easier to measure in mines, farms and factories than in the increasingly predominant service sector of a modern economy that sells a service the volume of which may not be obvious. For example how does one judge the quality of a report produced by an analyst today- enhanced by abundant data and powerful software and increasingly by AI? Not surely by the number of words written. Furthermore an enhanced customer service, better advice more rapidly provided, as for example, provided by a call centre, now armed with AI, will not be usually be directly charged for. The improved benefits it provides will come with a single charge for the good or service supported by a call centre- a laptop or cell phone for example. Or the fee charged by a customer relationship manager- a financial advisor perhaps, based upon assets being managed. A higher price or fee perhaps charged for the good or service bundled with the call centre or advisor would not necessarily mean more inflation. But rather represent a higher payment for an improved good or service.

To calculate output (GDP) and incomes or the values added we compare firm revenues today with revenues one or ten years ago, when prices observed were generally lower- given inflation. To make comparisons of real output and income and their growth over time, the value of all the goods or services supplied, must be adjusted for inflation to estimate the volume of goods or services produced. To estimate the real volume of goods or services produced or incomes generated over time. Most important prices have also to be adjusted for the changes in the quality of the of the goods and services supplied. We will not just be comparing the price of an aspirins with an aspirin which may well have increased over time. But rather comparing the prices charged for ever more accurately targeted capsules, developed with the aid of AI, and worth more in a real sense. AI is very likely to improve the quality as well as the quantity of goods or services provided.

Improved and lower costs of production could bring a mixture of absolutely lower prices and improved quality. It might mean deflation rather than inflation. How much prices fall in response to increased supplies will depend upon the growth in demand generally. That is on monetary and fiscal policy that could cause prices to rise on average even as economic growth – that is the volume of goods and services provided is growing. But if you underestimate quality gains incorporated into the price of goods and services and overestimate inflation by a per cent or two a year, you will then be underestimating productivity gains and economic growth at the same rate. And then be telling a very different story about economic progress. Perhaps AI will help economists and statisticians adjust more accurately for the changing and improved nature of the goods and services we consume.

A depressing reflection of the State of South Africa was the complaint of Richard Friedland, CEO of private health provider, Netcare, about a coming nursing crisis. An aging cohort of nurses, many more of whom will be retiring, is not being replaced for want of government action – ‘…..about which it was warned well in advance and chose to ignore it …” Netcare, he reported “…had been accredited to train more than 3,000 a year; it now trains barely a 10th of that…”

Clearly there is a demand for more nurses and a very large potential supply of aspirant nurses, given the current employment benefits and prospects. Why the government stands in the way of Netcare helping to close the gap between supply and demand of nurses is perhaps not as obvious as it should be?

Let us attempt to round up the usual suspects. The first suspect must be the arguments against private medicine that are made in principle. The case for equal treatment for all, paid for by the taxpayer, is one that ideologues employed in the Department of Health, hold fervently. Helping the nursing and other services a private hospital provides may provide may threaten this vision.

Though even the ideologues appear to concede the case for top up medical benefits paid for by the more prosperous. Perhaps they realistically understand that the better off in their key economic roles are much more likely to take themselves and their contribution to the revenues of government away from SA, for want of a world class and affordable medical service. A benefit we assuredly receive from the private hospitals and independent physicians that they are willing to pay for through a pay as you go system.

For an economy so obviously lacking in human capital, and not only for the capital embodied in the cohort of nurses, who are especially attractive immigrants, the consequences of an uncompetitive medical offering for highly mobile skilled South Africans are truly disastrous for income growth and taxes collected in SA. Upon which any National Health Service must ultimately

depend. Equal and hopelessly inferior is not an attractive prospect even for those who ignore the current realities of our government provided medical services.

It may still be asked why can’t the government, via its own large suite of public hospitals and large budgets, are failing to train more nurses and doctors for that matter? The answer is in the existing budget constraints. Budgets that provide well for those already in government service, provide employment benefits that keep up with and often exceed inflation of living costs, but leave very little over to employ new entrants to government service, of whom there are potentially legions. The private sector does not compete at all well with the public sector in the competition for workers of all skills- taking into account the private medical and pension benefits that the public sector employees draw upon.

But more important in the resistance to private medicine may be the force already prominent in explaining the actions and allocations of budget, commonly taken by state operated agencies in SA. Public hospitals and their procurement practice –definitely not excepted. The taxpayer has been held to ransom by the opportunists who intermediate between the State as payer and the service and goods providers. They have been extracting wealth from the taxpayers on a mind-numbing scale as Zondo our media and the US government has revealed.

The envisaged National Health Service will be a single payer for all the health services provided by the state. The intended budget will be an enormous one and the opportunities to navigate the gaps between the government as payer and the service and goods providers will be many and valuable. That that you can’t do (big) business with the SA government without a bribe or kickback must be regarded as alas, unproven. The evidence, the reality of SA, vitiates the case for a universal health system. But the private interest in such arrangements is a powerful one. That providers of private medicine in SA will have to resist to survive. They must make their case to the voting public- as Netcare has done.

In a previous piece (What can help the Rand and the economy? – ZA Economist) we discussed how ever-changing probabilities make Financial Risk so hard to measure and that investment outcomes are dominated by the return received, with any notion of the past risk faced quickly fading from memory. Thus, if a successful share investment has yielded an excellent return, is the happy result either because the shareholder took on extra risk and got lucky , or because the savvy investor knew the share was undervalued and proved to be so, becomes irrelevant.

Knowing the downside, estimating how much of a loss any portfolio or balance sheet can take and survive a potential loss is an essential task for the risk taking investor. Deciding what is a good bet – improving the odds of success by improving expected returns for any presumed risk -or reducing risks of failure for any expected return -makes every good sense.

Holding gold or perhaps more realistically holding a claim on a stock of gold held in some very safe place, has long proved itself as a sensible way to protect wealth against disasters in the form of war or revolution or more prosaically against inflation and their impact on many other ways to conserve wealth. As the dangers of an economic calamity rise, so typically, as will be expected, the price of gold will move higher.

If so, as will a claim on gold bearing rocks in the ground, that will be gradually turned into gold on the surface by a gold mining company. A share in the expected profits of a gold mining company will then also provide very useful insurance against danger. The gold price and the share price will move in the same direction – but given all the potential gold in the ground, and the risks associate with bringing it to the surface – the share price will be far more variable, hence far riskier than the gold on the surface. The recent sharp upward movement in the gold price provides an appropriate example. The gold price has moved up 10% or so in dollars over the last year. If we take the example of the GoldFields (GFI) share price, this has moved up around 160% (a factor of 1.60times the Gold Price movement) over the same period.

But an investor seeking safety owning gold has still a further alternative. That is to buy an option to buy a share in a well traded gold mining company, at a pre-determined future date, at a price agreed to today. The options can be bought or sold at market determined prices until the expiry date of the option, after which that right or option becomes worthless.

Option prices therefore exhibit a still much greater level of variability (or risk) than the underlying metal or share prices . Because of this character they give investors an excellent opportunity to raise the expected return from an exposure to movements in the gold prices , with a much smaller risk of a loss should the gold price move lower. Give the option price volatility – the factor here

. The availability of gold shares and more so options on gold shares give investors, who want to speculate or to hedge a portfolio of gold bullion against a large contrary or unexpected movement in the gold price make for a very efficient vehicle to hedge the exposure while laying out significantly less capital or incurring expenses to improve the expected return- risk trade-off.

Graham- one needs protection against a fall in the gold price and/or the multiplied fall in the value of a share or an option. One hedges the gold bullion price position by selling (shorting) the shares or selling the option- the puts -to hedge the exposure to the share price. It is cheaper to sell the shares and cheaper still to put the shares. I have tried to spell this out but with difficulty as you will see. A portfolio of gold bullion. Gold price down 10% portfolio down 10%. Bullion price down 10% GFI down 100% – 10 times more. A short of how many GFI shares (1% of the portfolio) would give the bullion portfolio protection against a 10% fall in the gold price. A put option on GFI equivalent to 0.2% of the portfolio in gold would presumably protect against a 10% fall in the gold price.

In recent months a short duration Call Option on GFI, has moved up about 500% (a factor of 50 times greater than the move in the gold price) By agreeing to sell the share and more so an option on the share, one will have exposed (expensed) significantly less actual capital for the same hedging effect. Thatis protection against losses should the gold price move lower rather than higher – as was the expectation. If the gold price had fallen 10%, then one would have lost 10% of the portfolio capital if one had held gold coins (a ten percent fall for ten per cent of the portfolio), 1% of the portfolio for a short on the GFI shares but lost only 0.2% of the portfolio capital, if the outlay was in the form of a put on the GFI shares rather than a short. Therefore, one would have been be unambiguously better off to hold the gold share options (puts) (a 50th of the gold bullion loss). Thus for the portfolio manager who is a gold bull and is already committed to holding a large amount of bullion, he can turbo-boost his investment in gold, with little added risk, by making a relatively small purchase, risking relatively little capital on a highly geared Gold share options. The potential gain (retrun on capital invested in the option) will be very large should the gold price move higher- but the potential loss – compared to the losses incurred by investing the same amount of capital in gold or gold shares – should it all turn out badly – will be much smaller. The return- risk trade-off, calculated looking ahead rather than behind, will have been greatly improved.The fact that at any moment in time judged by observing the random daily nature of the gold price, the gold price has as much chance of rising or falling from its current market determined value, means that the gold bulls are always matched by the gold bears – at the market determined price, or share price, or option price on the shares. The profit seekers in a higher gold price– as in any other actively traded asset – will always be matched by the profit seekers – those who are cashing in on their positions, believing the price will go down. And they will be able to do so at a market clearing price that matches the amounts of bullion or share or options bought and sold. The market makers, including the option providers, will match buyers and sellers. They ideally from their perspective will be rewarded with a fee and not be exposed to the highly unpredictable move in the underlying metal or share prices.

Structuring such risk reducing strategies is complicated for the average private investor. But it may be straightforward for banks or others who provide structured products bought by retail investors. Constructs that trade off less upside gain for less downside risk of losses It should be possible to put together a blended product of say 90% gold bullion and 10% Gold share options of appropriate duration. Such a listed financial security registered for trade on the JSE would exhibit high gearing to the gold price upside but for lower risk of losing capital should the gold price move in the wrong direction, which it may well do. Over to the market place.

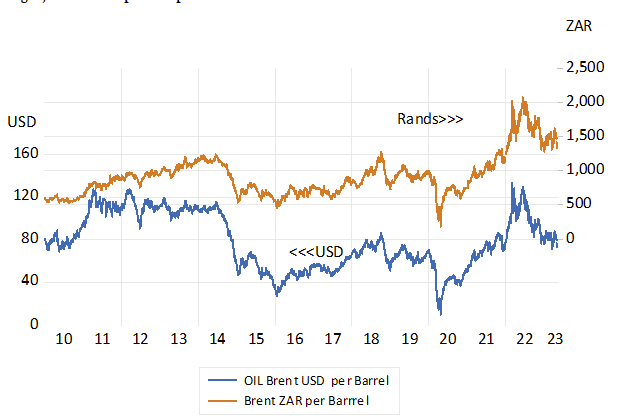

In early 1980 the Rand reached a peak of 1.32 US$ to the Rand; yes, the Rand then bought more than one dollar! This was the time of a very high gold price of $820 per oz. when Russia invaded Afghanistan and WW3 looked like a real possibility. It was but 35 dollars an ounce in 1970. Things have not been as rosy on the exchange rate front since. The exchange rate is currently around 19.2 Rand to the $. This means that in purely nominal terms the Rand is currently 1/25th (against the dollar) of what it was in those heady days of 1980! If the ZAR merely adjusted for differences in SA and US inflation since 2000 the dollar would now cost less than R13. In a relative sense- the ratio of the market to the Purchasing Power Parity was only wider in 2002 when the ZAR was nearly 80% undervalued. At current exchange rates it is about 50% undervalued. Or in other words the rand buys roughly 50% less in NYC than it does in SA as SA visitors will testify. The great deals will now be realised by tourists to SA –until the rand sticker prices in the stores and on the menus are marked higher. See figure 1

Figure1. The USD/ZAR and its PPP equivalent.1 Monthly data to April 2023.

Source; Federal Reserve Bank of St.Louis, Stats SA and Investec Wealth and Investment

In the seventies as the gold price took off- more in USD than ZAR, SA was the largest gold producer in the world and gold mining was hugely lucrative for shareholders in the gold mines and for the SA government who collected much extra revenue from taxes, and royalties paid by the gold mines. Platinum mining was only then getting going and subsequently got a huge boost from the widespread use of catalytic converters in the exhausts of motor vehicles. Coal exports got going after the construction of the huge export terminal at Richard’s Bay, and the rich Sishen iron ore deposit was still to be exploited.

South Africa is now merely the eighth largest producer of gold in the world, producing but a sixth of the gold delivered in 1970. And gold production is now a relatively small part of the South African economy that in the seventies accounted for 60% of all exports from SA and about 16% of GDP. The link between the gold price and the exchange rate

is now correspondingly weak and has done little to save us from facing the second weakest Rand on record and ever higher long-term interest rates.