New York, November 21st 2018

It is Thanksgiving this Thursday in the US – a truly inter-denominational holiday when Americans of all beliefs, secular and religious, give thanks for being American – as well they should.

This is a particularly important week for American retailers. They do not need not to be reminded of the competitive forces that threaten their established ways of doing business. Nor do investors who puzzle over the business models that can bring retail success or failure.

The day after thanksgiving is known as Black Friday, when sales and the profit margins on them will hopefully turn their cumulative bottom lines from red to black. It has been black Friday all week and month and advertised to extend well into December. Presumably, to bring sales forward, that is to make retailers less dependent on the last few trading days of the year.

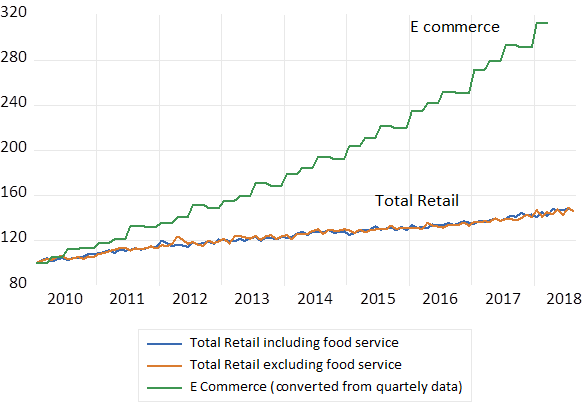

The competition as we all know has become increasingly internet based from distributors of product near and far, and yet only a day or two away. E commerce sales have grown by over three times since 2010 while total retail sales including E commerce transaction are 50%up since 2010. Total US retail sales, excluding food service are currently over $440b and E commerce sales are over $120b (see figures 1 below)

Fig 1; US Retail and E Commerce sales (2010=100) Current prices

Source; Federal Reserve Bank of St.Louis (FRED) and Investec Wealth and Investment

The growth in E Commerce sales appears to have stabilised at about 10% per annum. (see figure 1)

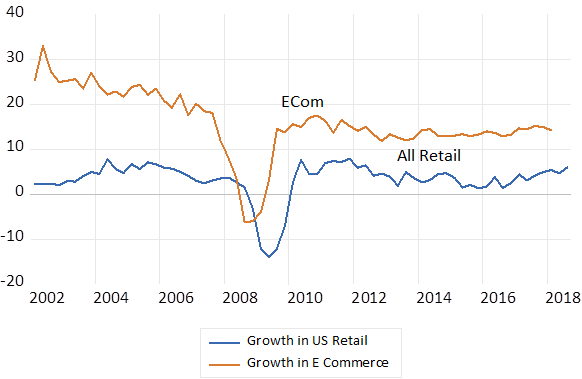

Fig 2; Annual growth in total retail and E commerce sales in the US (current prices)

Source; Federal Reserve Bank of St.Louis (FRED) and Investec Wealth and Investment

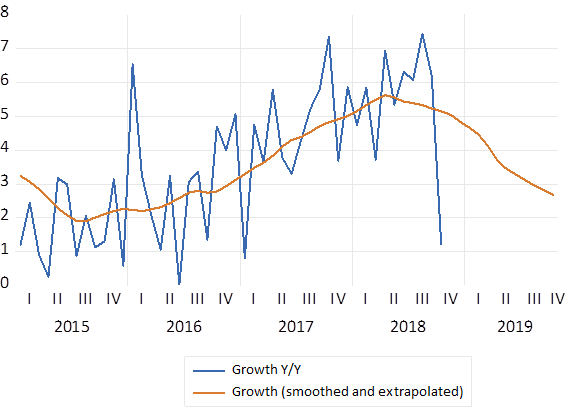

Retail sales of all kinds have been growing strongly – though the growth cycle may have peaked- as may have GDP growth- leading perhaps to a more cautious Fed. How slowly growth rates will fall off the peak is the essential question for the Fed as well as Fed watchers and answers to which are moving the stock and bond markets. (see figure 3)

Fig.3: The US retail growth cycle

Source; Federal Reserve Bank of St.Louis (FRED) and Investec Wealth and Investment

The inportance of on-line trade is conspicuous in the flow of cardboard boxes of all sizes that overflow the parcel room of our apartment building. Including boxes of fresh food from neighbouring supermarkets. The neighbourhood stores of all kinds are under huge threat from the distant competition that competes on highly transparent prices on easily searched for goods on offer as well as convenient delivery. As much is obvious from the many retail premises on ground level now standing vacant on the affluent upper East side of New York. The conveniently located service establishments survive, even flourish, while the local clothing store goes out of business because they lack the scale (and traffic both real and on the web) to offer a credible offering.

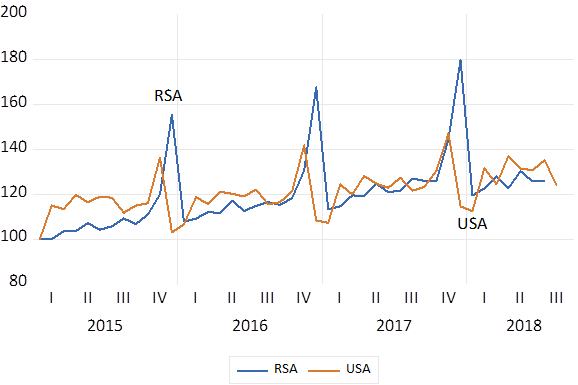

But spare a thought for SA retailers for whom sales volumes in December are much more important than they are for US retailers. November sales for US retailers – helped by Thanksgiving promotions – are significantly more buoyant than December volumes. According to my calculations of seasonal effects since 2010, US retail sales in December are now running at only 90 per cent of the average month while November sales are well above average, at 116% of the average month. Retail sales in the US however include motor vehicle and gasoline sales that are excluded from the SA statistics. December sales in SA are as much as 137% above the average month helped as they are by summer holiday business as well as Christmas gifts. (See figure 4 below that shows the different seasonal pattern of sales in the US and SA)

Fig.4; The seasonal pattern of retail sales in SA and the US (2015=100)

Source; Federal Reserve Bank of St.Louis (FRED) and Investec Wealth and Investment

In the black Friday for SA retailers thus comes later than it does in the US. And perhaps makes the case for adding promotions in November to smooth the sales cycle and reduce the stress of running a retail business. They may also hope that the Reserve Bank is not the grinch that spoils Christmas- though the answer to this will come on Thanksgiving.