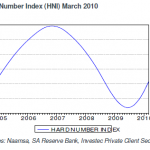

The Reserve Bank on Friday 9 April reported the number of its notes circulating at the end of March. This enables us to update our Hard Number Index (HNI) of the SA Business Cycle that combines vehicle sales, also available for March 2010, with the real money base, that is the note issue deflated by the CPI.

The HNI is pointing firmly upwards, confirming very clearly that the SA economy has entered a new upswing phase in the SA business cycle (see below). Higher numbers indicate that the economy is expanding, that is, the economy is delivering positive rates of growth that will be confirmed in due course by a much wider selection of economic time series. First quarter GDP numbers for example will only be released in June 2010.

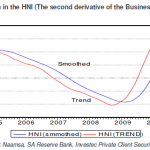

The second derivative of the business cycle, that is the rate of change of the HNI, is also in positive territory and indicates that growth is accelerating. The economy according to the HNI began to grow again in the fourth quarter of 2009, as confirmed by the National Income statistics for the quarter. It is picking up momentum.

image001

image002

As we reported previously, the new vehicle cycle is demonstrating very strong growth. The growth trend in vehicle sales is pointing sharply higher.

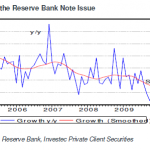

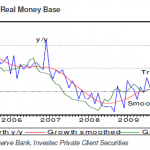

The growth in the note issue picked up in March 2010. However when these numbers are adjusted for the declining trend in the CPI the real money base is indicating positive growth rates at a modest rate (see below).

image004

image005

It should be appreciated that the note issue will grow in line with extra demands for cash that reflect the state of the economy. It is therefore a very good coinciding indicator of the state of the economy rather than a leading indicator. Growth in the supply of cash does not lead the economy but follows it. Nor is it a policy instrument of the Reserve Bank, though we have argued it should be. However the note issue has the great advantage for economic forecasters of being a very up to date indicator of the current state of the economy. Most economic indicators provide only a rear view mirror of the state of the economy.

The HNI overcomes the problem of driving along the economic track through the rear view mirror. The index, as we have shown, tracks the official business cycle indicator of the Reserve Bank very closely. It has the advantage of being very up to date as well as being based on hard numbers – actual vehicle sales and the note issue. The release of the Reserve Bank’s Coinciding Indicator of the SA business cycle by contrast lags behind economic events by three to four months (the latest number is for December).

The HNI therefore estimates the immediate state of the economy and the current estimate leaves little doubt that the economy is in a cyclical upswing and is accelerating.

It seems clear that new Reserve Bank governor Gill Marcus has not yet brought anything of a different point of view to the

Monetary Policy Committee (MPC). The style was much more inclusive and open but the substance was largely the same as

before. She has deferred to the established positions of the MPC of which she is the only new member.

Therefore the sense held by the previous MPC that the economy is at a turning point and therefore needs no further

encouragement for fear of being too procyclical with interest rates (which have declined by 500bp has been maintained). Also

maintained is the concern with second round effects on inflation of electricity price increases – absent of which inflation would not

be regarded as a problem at all by the MPC.

The inflation problem is Eskom and interest rates remain where they are largely because of the Eskom effect on inflation. This

Eskom effect is creating great uncertainty and therefore is affecting inflationary expectations which are presumed to make ever

higher inflation inevitable, unless the Reserve Bank remains vigilant in setting interest rates accordingly.

Had I been at the Media Conference I would have asked this question. Does not the prospect of further electricity price increases

justify lower rather than higher interest rates given the impact of such price increases on domestic spending and therefore on

output and employment?

The answer that would have been provided would unfortunately probably have been something like as follows: no, because higher

inflation following such electricity price increases might lead to even more inflation – because of possible second round effects on

inflation.

That the MPC could still concern itself with second round inflation when the economy is as weak as it is and when the rand is as

strong as it is and when in the Reserve Bank’s view global inflation is not a threat at all to domestic inflation, speaks volumes about

the MPC’s lack of grasp of the causes and effects of supply side shocks on prices. But here nothing has yet changed with Ms

Marcus in the chair – which is the pity.

The right answer would have been yes – because Eskom’s price increase is a tax on consumers and tax increases lead to higher

prices and less spending and in the circumstances, while inflation will go up – profit margins will come down and employment

growth will remain subdued and so the economy will need some encouragement from monetary policy. Or in other words the

distinction between supply side shocks that drive inflation higher and demand led inflation should be emphasised by the

Governor. The Governor should make it clear that Monetary Policy can only be effective against demand led inflation and

monetary policy should not add to the demand reducing influence of higher levels of taxation.

Ms Marcus was also complacent about the negative growth in money supply and credit which other central banks have been very

active in trying, though not yet succeeding in combating. Again the MPC still does not wish to do anything to encourage SA banks

to ease up for the sake of the economy.

But this lack of action by the MPC was surely encouraged by a belief that the domestic economy is recovering. However such

predictions by the Reserve Bank were highly qualified as the quote from the MPC statement below indicates very clearly:

There are signs that the domestic economy will continue on its recovery path but economic growth is expected to remain below

potential for some time; and dependent to some extent on the pace of the global recovery, which still appears to be fragile and

uneven across regions. Economic growth is also expected to be constrained by subdued domestic consumption expenditure. The

domestic outlook for inflation remains favourable as a result of weak demand pressures and the main threat to the inflation outlook

emanates from possible electricity price increases.

We however see no signs of any meaningful revival in domestic spending. Reference was made to the particular unpredictability of

GDP growth this past quarter- of which preliminary estimates will be released next week. However marginally positive quarter-on-

quarter GDP growth may be recorded even as final consumption and investment demands decline. Improvements in net exports

and a reversal in inventory accumulation may yet allow GDP to grow even as final demand remains very weak. Even a modest

recovery in GDP growth would therefore not indicate the likelihood of the SA economy operating even close to its potential over

the next year – something that should concern the MPC greatly.

Should the Reserve Bank be surprised by the lack of economic recovery, it now only has its next meeting in January 2010 to

respond to it. We should not expect any emergency meeting before then and we should expect interest rates to remain on hold for

much of 2010. We can anticipate that a broader mandate for the Reserve Bank is in the offing that would allow it to concern itself

more with the growth outlook and less with the inflation outlook, especially when the inflation is supply side driven, as is clearly the

case now. We would welcome such a development as we would continue to support the independence of the Reserve Bank to act

as it judges – an independence that Governor Marcus will uphold determinedly.

This is not an easy time to be taking over the reins at the Reserve Bank. Spending by households and privately owned firms (which account for a very large part of the economy – up to 80% of GDP) remains in the grip of a very severe recession. More important for Gill Marcus to take into account is that there seems little sign of any imminent recovery in this spending upon which the economy depends for its growth.

For technical reasons the third quarter GDP numbers might look better because exports declined less than imports and the run down in inventories was at a slower pace than it was in the second quarter when an extraordinary reduction in inventories took as much as 10% off the GDP growth rate. But such numbers will indicate just how weak the economy is and there will be little consolation to be found in the trends in spending by the private sector.

The case for a fresh dialogue

The case for the Reserve Bank in these circumstances doing all it can to help the economy by lowering interest rates and pumping in cash to encourage the banks to lend more, might appear unassailable. However the Monetary Policy Committee found reasons at its last two meetings not to lower interest rates or to ease quantitatively.

The arguments that would have supported such inaction would presumably have included the notions that real interest rates in SA were already very low. The argument would also have been made that inflation in SA remains unsatisfactorily high and that elevated inflationary expectations could continue to have an unwelcome self fulfilling impact on inflation itself.

Ms Marcus would do well to question the validity of such arguments. It was such arguments that helped raise interest rates to recession producing levels in the first place and restrained their reversal long after it was clear that the growth in spending by households, particularly on interest sensitive durable goods was falling sharply. The damage caused to the economy is there to be seen. As we have argued before the weakness in the SA economy was of our own making. The global credit crisis made it more difficult to escape from recession.

What exactly are real interest rates?

Firstly let us raise the issue of real interest rates that may be defined as the difference between borrowing costs and inflation. By reference to CPI inflation real money market interest rates in SA may indeed appear very low. However if prices realised by producers, represented by the Producer Price Index (PPI), are taken as the point of reference real interest rates have increased to exceptionally high levels as we show below. The reason for this difference is that while consumers in SA still face inflation, producers have to deal with significant and dramatic deflation.

CPI and PPI Inflation

Source: StatsSA and Investec Private Client Securities

The Consumer and Producer Price Indexes

Source: StatsSA and Investec Private Client Securities

SA Real short term interest rates

Source: StatsSA and Investec Private Client Securities

Real interest rates are very high – not very low

The simple idea behind the importance attached to real interest rates is that higher prices charged for goods sold offset the interest costs of borrowing. In an extreme case, if the prices firms can charge for their goods or services rise faster than the interest rates then doing no more than borrowing (cheap) money to fill up a warehouse with stuff that is bound to increase in value becomes a highly profitable business. For a household taking a loan to buy goods (a car or a house), the prices of which will rise as fast as the interest rates they are charged, may also seem like a good idea.

However as is very apparent SA households are not responding to the prospect of more inflation by borrowing more, even when banks or retailers remain willing to lend. They are borrowing less because the prices of the homes and cars and furniture they might in normal circumstances be in the market for are not expected to rise at anything like their cost of borrowing. They may even be expecting prices to fall. They will know that the rising prices they are forced to pay are for goods and services they cannot store – electricity and other municipal services that could better be described as higher taxes.

The firms that might ordinarily be encouraged to borrow funds to add to stocks and work in progress and to their complement of workers, or to add more plant and equipment, are facing and expecting deflation rather than inflation. For them the idea that their real costs of borrowing have declined is risible. Their real cost of borrowing, that is to say the real interest rates they are paying, has risen dramatically. This is why they are running down inventories, working capital and (most regrettably) workers employed.

The reality is that for producers in SA prices are falling, not rising. The further reality is that higher prices/taxes paid by their customers and themselves for electricity and other services and the higher wages they have been forced to pay their unionised workers have made it harder rather than easier for them to raise prices. The strong rand has most importantly made it more difficult for them to compete on the local or export markets. They have less, not more, pricing power because of the rising trend in CPI and wages. Their operating profits have come under such pressure and this has led them to invest less and employ fewer workers and managers.

Inflation is not a self fulfilling expectation

The notion that in these circumstances producers will not only expect more inflation but that such expectations could be self fulfilling in the absence of support from the demand side of the economy, is surely a damagingly false notion. It means damagingly high interest rates. In the absence of accommodating demands for goods and services inflationary expectations (that is to say in current circumstances, expectations of more supply side shocks for the economy in the form of higher electricity prices) will not lead to still more inflation. Supply side driven inflation expected will however lead to less output and employment. All the Reserve Bank can hope to do in such circumstances is to ease rather than add to the punishment.

The Reserve Bank needs to make the firm distinction between the inflation it does have influence over (demand led inflation) and supply side shocks that cause inflation and even expected inflation to rise – over which it has no direct influence.

Judging the right level of interest rates for SA without full regard to this distinction can prove very damaging to the economy. Interest rates influence the spending decisions of SA households and firms without necessarily having a predictable influence on the supply side of the economy and therefore on prices. The unpredictable link between interest rate changes and the exchange rate makes it even more difficult to know how interest rates will influence the inflation rate in SA.

Ms Marcus would do well to recognise these difficulties for the practice of monetary policy in SA. She should also be under no illusions that the only problem for the Reserve Bank to focus its attention upon for now is the very weak state of demand, not the rate of inflation.

Statistics recently released for new vehicle sales and the note issue of the Reserve Bank in October 2009 do not indicate that any recovery of the SA economy is under way. The data suggest if anything that the SA economy has continued to shrink at a faster rate.

These two very up to date economic series, vehicle sales and the note issue, both actual numbers rather than estimates derived from sample surveys, make up our Hard Number Indicator (HNI) of the state of the economy (we adjust the note issue for consumer prices). As may be seen below our Hard Number Index (HNI) tracks the coinciding business cycle indicator of the Reserve Bank very closely. As may also be seen the HNI calculated to October 2009 is still falling while the Reserve Bank Coinciding Business Cycle Indicator, available only to July 2009, has levelled off.

The Hard Number Index and the Reserve Bank Coinciding Indicator

Source: I-Net Bridge and Investec Private Client Securities

Two measures of the State of the SA economy 2007-2009

Source: I-Net Bridge and Investec Private Client Securities

The HNI and the Coinciding Indicator may be regarded as representing the rate of change of the economy or the first difference of the level of economic activity. When the economy is picking up momentum or accelerating, the indexes should point higher and when the economy is decelerating the indexes should point lower.

The second derivative – that is to say the rate of change of the rate of change – may provide a further indicator of the direction of the economy. However when we review the second derivative of the HNI, it does not suggest that the economy has begun to decelerate at a slower rate. In fact the economy, according to the HNI, appears now to be decelerating even faster than it was. We provide two measures of the direction of the HNI. One is the annual year-on-year change in the HNI and the other the monthly change in the HNI annualised. The monthly move in the index raised to the power of twelve suggests that the economy was deteriorating at a faster rate between August and October.

The HNI – The second derivative

Source: I-Net Bridge and Investec Private Client Securities

While vehicle sales are now declining at a slower rate (see below) the Real Note Cycle or what can be described as the real money base of the system, having tentatively recovered in September, turned down again in October (See below).

New vehicle cycle

Source: I-Net Bridge and Investec Private Client Securities

The real money base cycle

Source: I-Net Bridge and Investec Private Client Securities

The evidence suggests that domestic spending remains very weak. While GDP in the third quarter may have benefited from a less severe run down of inventories and an improvement in net exports, SA households and firms remain highly reluctant to spend more. And while they retain these inhibitions the economy will not be able to make much progress.

The Monetary Policy Committee of the Reserve Bank will be updating its evidence on the state of the economy next Monday and Tuesday under the direction of the newly appointed governor Gill Marcus. The weakness in domestic spending revealed by vehicle sales and the demand for and supply of cash, as well as the slow pace of revenue collected by the Treasury reported on recently, should ordinarily provide every reason for cutting interest rates and quantitative easing, as should the strength of the rand and the lower inflation accompanying the stronger rand.

A newly appointed governor might however prefer to wait and see how the economy evolves before taking any bold action. However any complacency about the ability of a global economic revival to lift the SA out of its current severe recession mire should be actively discouraged by the latest data.

The focus of fiscal policy in South Africa on the long run interests of the economy by living within your means has been admirable. It means building balance sheet strength in the good times when revenue growth is strong rather than indulging in a spending fever. So that when the economy slows down, more debt can be raised to finance government spending to avoid a self destructive resort to higher tax rates. Higher tax rates in a recession can easily lead to less rather than more tax revenue and slow down the economy and revenue growth further.

On reading the Medium Term Budget Policy Statement (MTBPS) one was gratified that the Treasury and its Minister understood these facts of economic life very well. No resort to higher taxes was to be made while government spending was to be sustained. And then the Minister of Finance in comment later last week, in all innocence presumably (hopefully) pronounced on the necessity to raise taxes should the economy not grow as expected.

This is very worrying. The most urgent task facing those responsible for managing the economy is to do all they can to get the economy moving again. This means all the encouragement they can offer households and firms to spend more now. It should mean lower rather than higher tax rates. For example temporarily accelerated investment allowances would help private sector capital formation, which has stalled so badly, as would every effort made to accelerate the award of tenders for the infrastructure programme about which the construction industry is so concerned.

Monetary policy also needs to try a lot harder than it has to get money and credit supply growing again. Lower interest rates might not help much on their own any more, but if accompanied by the quantitative easing practiced everywhere else to pump extra cash into the economy, it would do no harm and might do some good.

Yet despite the recession and the deflation of prices at the factory and farm gates one still hears whispers out of official circles of the danger of self fulfilling inflationary expectations. The theory that inflation can be self perpetuating irrespective of the state of demand in the economy is wanting in ordinary circumstances – it is simply damagingly nonsensical at times like this.

The biggest danger to the recovery of the economy would be the much higher charges Eskom would like to impose on the economy, charges that would allow Eskom to avoid to a significant degree drawing on the government balance sheet to finance its essential capital expenditure. Incidentally this capex is particularly welcome at this stage of the business cycle.

Such price increases well above the cost of supplying additional electricity (costs understood to include an appropriate return on capital to be invested) should be resisted by raising more government debt. That is to say, it should be financed with more Eskom debt, assisted by a further government guarantee, should the considerable guarantees provided for Eskom debt to date be insufficient to the purpose of avoiding excessive price increases.

Increased charges (i.e. taxes) for electricity would continue to add to measured inflation as they have done to date. They will also, as they have done to date, tax away spending on almost everything else. Could the SA authorities, despite the state of the economy, not only raise taxes in the form of excessive charges for electricity but in addition also raise interest rates because of the impact higher electricity prices will have on inflation, and maybe therefore on inflation expected? Such responses are not apparently impossible to contemplate and so represent a most dangerous threat to the long term health of the economy.

The long term health of the economy and the willingness to invest in its long term potential will depend on the confidence investors and households will have in the ability of the authorities to manage the business cycle in a sensible way. They would spend and invest more now knowing that the path back to sustainable growth has been clearly marked out. Some of the signals received from the Treasury and the Reserve Bank about how to make the transition from the short to the long run do not always inspire confidence.

The global recession has led the monetary and fiscal authorities to usefully recall the advice Milton Friedman offered on how to deal with a banking crisis by the central bank acting as the lender of last resort (in his Monetary History of the US published in the late 1960s) and the instruction John Maynard Keynes provided on how to deal with depression with vigorous government spending (in his highly influential General Theory of Employment Interest and Money, published in 1936). Keynes was cynical about the human condition but it might be well for our authorities to be reminded in current circumstances of his celebrated remark that “in the long run we are all dead”.

The presentation of the Medium Term Budget Policy Statement in Parliament yesterday was unusually important for two reasons. It was the public baptism of the recently appointed Minister of Finance, Pravin Gordhan, who would be presenting the revised three year outlook for government spending and revenues in much changed economic circumstances.

The severity of the recession had made nonsense of the Government’s Revenue projections made in February this year. Gross tax revenues estimated for fiscal year 2009-10 have now been revised markedly lower by R70bn from the R659.3bn expected in February to R589bn, or from 26.6% to but 24.5% of a significantly lower expected GDP. Expenditures have been revised modestly upwards by about R16bn, so lifting the budget deficit from an estimated R95.6bn in February to the latest estimate of -R181.6bn and requiring additional, not previously planned, debt issues of R85.5bn. Government expenditures are now equivalent to an unhealthily large 35% of GDP. Unhealthy in normal circumstances but temporarily helpful in offsetting the sharp decline in private spending

The unknowns to be resolved yesterday were about style: how would the Minister present himself and be received, and about content, and how would the government address the much more difficult economic circumstances in its plans for revenue collection and spending?

Comfortably in command

On the question of appearance and reception the Minister was very well received. South Africa, one would suggest, has found a worthy successor to Trevor Manuel. The rookie Minister was comfortably in welcome command of his brief. Especially welcome since the content of his proposals and projections were eminently sensible and represented the continued commitment to fiscal conservatism of the SA government.

The immediate recessionary dangers facing the economy were well recognised – no pro cyclical increases in tax rates are proposed – and the extra borrowing requirement is to be wisely tolerated, given the strength of the balance sheet.

While, as was pointed out, the financial situation of the SA government has deteriorated more severely than almost anywhere else, the ratio of government debt can be allowed to increase from the currently low 23% of GDP to an estimated, much less comfortable 41% of GDP in 2012-13 when the economy will have recovered to a degree. The interest expense on the Budget will have risen by about R40bn or around R100bn a year. But importantly the plan thereafter is to reduce dependence on debt finance to reduce spending on interest and to restore the still highly valued balance sheet strength. This will allow spending on much more valuable other services to the hard pressed South African public. It should be appreciated that fiscal strains in the developed world will see government debt to GDP ratios rising above 100% within the next year or two – a much more difficult condition than that faced by South Africa.

A very conservative U-shaped recovery is predicted by the Treasury, though its forecasting credentials will not have been improved by the recent underestimates of economic activity. GDP is estimated to decline this year by 1.9% and to grow next year by only 1.5% and to then pick up to a still modest 3.2% rate of growth in 2012. Such an economic outlook, taken with the established and appropriately careful approach to issuing more debt, make for highly constrained plans for extra expenditure and revenue between now and fiscal year 2012/13.

The framework allows for government expenditure to grow at a compound average growth rate of 7.8% per annum and for revenues to grow faster, to partially close the deficit of 11.9% a year. The deficit is thus planned to decline from an estimated R183.8bn in 2009/10 to R131.5bn in 2012/13. Since inflation is expected to average around a still high 6% a year this will mean minimal growth in real government spending, though much faster growth in real government revenues is predicted.

The intention to reduce deficits and to contain real government expenditure is admirable. Whether such revenue estimates will prove consistent with macro-economic stability remains to be seen, especially if Eskom is allowed to tax the hard pressed consumer to the extent it has proposed. The Treasury has set its face against further debt issues by the central government and further guarantees of the debt issued by state enterprises including Eskom. Over R170bn of additional Eskom debt has already been guaranteed by the Treasury and we may hope that this will allow for electricity prices that make long run economic sense and do not damage the economy in its current fragile state. Perhaps in the strained circumstances actually selling off a power station or two, accompanied by an attractive enough price for the electricity to be fed to the grid, will seem like a good financial deal.

The strained financial conditions would also seem to have ruled out expensive health care innovations at least for the foreseeable future. They have also led to grave concerns about the size of and employment benefits of what has become an increasingly well paid government employee. The scope for further improvements in public sector conditions of employment are being recognised as very limited.

Hamlet without the Prince

The government in this Budget Review could not have been more frank about the large scale failures of its own administration and then the need to address its inability to service the community. To quote the Budget Statement: “The functioning of the public service requires fundamental reform to obtain better value for public money, to do more with less, and to build a culture of responsible stewardship so that citizens trust the institutions of service delivery…..”

Such self recognition is very welcome as a starting point to reforms that are essential to the purpose of a better South Africa. Also welcome is the recognition of the extreme gravity of the employment problem that is graphically illustrated in the Statement. South Africa’s ability to offer employment, that is to say its ability to absorb labour, appears weaker than almost anywhere else in the world with only 42% of the age group 15-64 in employment. To quote the government again, “creating jobs, particularly among millions of relatively unskilled South Africans, is the country’s greatest economic challenge….” A number of interesting innovations are proposed to this end, but a discussion of this issue without reference to the employment destructive role of unions – or how such employment objectives can be met without the essential services of labour brokers – is bit like Hamlet without the Prince.

Helpful to the goal of a stronger economy are the steps taken and intended that will enhance the flexibility of monetary policy. Also signalled by the Treasury was a more flexible approach to inflation targeting that took account of forces acting on inflation that was beyond the influence of monetary policy.

The significant exchange control reforms announced have been timed to counter an unwanted degree of rand strength. The Brazilians have imposed a tax on capital inflows to this purpose. More impressively South Africa has provided greater freedoms to move savings in and out. The currency market however did not react at all to the news – though the rand had responded earlier yesterday with weakness and again today to the downward pressure being exerted on emerging equity and commodity markets accompanied by the stronger US dollar. We show below how little reaction to the Budget statement made at 14h00 was observed in the currency market, while the market in RSA debt reacted favourably to the news.

R157 bond

Rand/US dollar

Graph sources: Bloomberg

Clear evidence that the government continues to budget conservatively and wisely under capable guidance is very welcome. Very welcome too is the recognition of its own failures to deliver services and employment opportunities as an essential starting point for reform. But the state of the economy remains very fragile and every effort will still have to be made to encourage domestic spending for the sake of incomes employment and government revenue.

By the end of this year, it will have been 20 years in which long dated bonds will have registered superior returns over equities in the US and South Africa. As may be seen in the tables below long dated government bonds have outperformed the equity index in the US and the RSA on both dimensions – they have provided significantly extra annual returns for less risk – as measured by the standard deviation of these returns.

Unexpectedly equities have failed to provide long term investors with a risk premium over long dated bonds. Equities and bonds have returned more than cash over the period though the competition from cash for equities in SA has been very strong over the past 20 years. Encouragingly all asset classes in both economies have provided in returns well ahead of inflation over the past 20 years. Especially so for SA investors (it was not as if equities performed poorly): in real terms they provided excellent average returns of over 5% pa. However, as may be seen, long dated bonds did even better for somewhat less risk.

Annual Returns Equities, bonds and cash calculated monthly 1990-2009

USA

Sample: 1990:01 2009:09

S&P 500

US 10 Y TBONDS

US SHORTS

US INFLATION

Mean

7.2

10.6

4.1

2.8

Median

11.1

12.9

4.7

2.8

Maximum

41.6

62.1

8.3

6.3

Minimum

-59.6

-30.4

0.3

-2.3

Std. Dev.

18.2

15.3

2.0

1.3

Observations

237.0

237.0

237.0

237.0

RSA

Sample: 1990:01 2009:09

JSE

SA LONG RSA

CASH

SA INFL

Mean

13.7

16.2

12.1

8.0

Median

14.8

18.7

11.7

7.7

Maximum

54.3

41.1

21.7

16.6

Minimum

-43.4

-18.8

6.8

0.1

Std. Dev.

19.2

12.2

3.4

3.9

Observations

237.0

237.0

237.0

237.0

Source: Investec Private Client Securities

The prices of long dated bonds generally rose over the 20 years as they benefited greatly from low inflation. Long dated interest rates fell back as less inflation was priced into their yields. Clearly the monetary and fiscal authorities consistently surprised the bond market in their ability to reduce inflation – and even more so in the US than in South Africa as we show below. Less inflation expected was good for equity returns and for the real returns from cash – but it turned out to be even better for investors in long dated bonds.

Fixed Interest yields 1990-2009

Source: Investec Private Client Securities

The caveat – past performance is not necessarily a guide to future performance – may be particularly apt when we contemplate expected returns from bonds, equities and cash over the next 20 years. Equities will always be valued to realise an expected premium for the extra risks associated with them. The yield on long dated bonds will always carry a premium to cover expected inflation. But as always, markets may be surprised or disappointed as evidence changes the temporary beliefs captured in current valuations giving rise to unexpectedly good or poor returns.

There is no guarantee that over the next 20 years inflationary expectations will be revised generally downwards as they have been over the past two decades. Given the much deteriorated recent state of government finances in the developed world, the temptation will have risen to print money to finance government expenditure – rather than cut expenditure or raise taxes and or pay market interest rates for funds borrowed. The share of government tax revenues that will have to go to pay interest rather than used for much more popular spending will be rising inexorably over the next few years at least.

Yet the bond markets in the developed world remain highly sanguine about the inflation outlook. The yields on US and other developed country bonds are currently offering inflation compensation of less than two per cent per annum on bonds maturing in 15 or more years, that is nominal bonds issued by Uncle Sam are currently offering near record low yields (about 3.5% pa) and less than two per cent more than the inflation linked bonds that would secure investors a real return over the long run. Currently these long dated inflation linkers also yield less than a two per cent per annum real yield. In SA the bond market is compensating for expected inflation by offering more than six per cent more on vanilla government bonds over their inflation linked equivalents.

We would regard the vanilla government bonds in the US as dangerously exposed to a revival of inflationary expectations. Accordingly holding inflation linked US government bonds seem like the superior alternative for now. By contrast in SA the higher yields on RSA vanilla bonds do now offer more attractive compensation for inflation to come. An average rate of inflation of over 6% per annum now priced into the bond market may well again prove overly pessimistic about the ability of the SA government to contain inflation in the years to come. Perhaps the history of declining bond yields in SA over much of the past twenty years should encourage SA investors to pay more respect to long dated bonds as an asset class.

The strength of the rand has astonished many. The rand is now more than strong enough to bring down inflation, which it is helping to do. The stronger rand and the downward pressure it has put on prices in the shops and showrooms is providing some encouragement to still very depressed domestic spending.

Further rand strength would not be very welcome. The gains made by consumers in the stores are at the expense of domestic manufacturers and their employees competing for shelf space. Their rand costs, especially their wage costs, are still rising while their pricing power in rands is under pressure from cheaper imports. It would greatly help if the trade unions moderated their wage demands accordingly, but such assistance has been sadly lacking and job losses continue as the manufacturers and miners attempt to reduce their costs to counter the pressure on their operating margins caused by the strong rand.

It needs to be appreciated just how strong the rand is; why it is so strong and what implications for economic policy should be drawn from it. The rand, as we show below, has not only gained against the weak US dollar and the not-so-weak euro, but has held its own against the growing strength of the emerging market and commodity currencies represented below by the Brazilian real (BRL) and the Australian dollar (AUD). We show this below and also that rand strength this month against the US dollar and euro is accompanied by strength in emerging market and commodity currencies, of which the rand is clearly one.

The rand in 2009, daily data

Source: I-Net Bridge and Investec Private Client Securities

The rand in October 2009 (Sept 30=100), daily data

Source: I-Net Bridge and Investec Private Client Securities

Why the rand is so strong

The most obvious explanation for rand strength is the hugely increased flows out of the dollar and to emerging market and commodity fund managers, of which SA receives a consistent share. Citibank analysts report very large net flows into emerging markets of US$45.5bn this year, of which US$4bn flowed in the past week up to 14 October 2009.

The JSE offers very convenient exposure to emerging and commodity markets for offshore fund managers. It is exposed much more to the state of the global economy than the SA economy, which given the depressed state of the SA economy, is just as well. The correlation between moves in the benchmark MSCI Emerging Market Index and that of the JSE when converted into US dollars is very close (about one to one) as we show below.

The JSE ALSI (USD) vs the MSCI EM (January 2009=100), daily data

Source: I-Net Bridge and Investec Private Client Securities

The JSE ALSI (USD) vs The MSCI EM, September to October 2009 (October 2009=100), daily data

Source: I-Net Bridge and Investec Private Client Securities

What it means to be a global market

This correlation shown above as indicated is no co-incidence. It is because JSE listed companies are fully exposed to the expected and improving trends in the global economy and especially the emerging market share of it, which is growing and is expected to grow at well above average rates. Hence the demands for shares in companies exposed to this promising growth found on the JSE.

How to capitalise on the opportunity presented by abundant capital

The question then is how best to take advantage of these inflows of capital that have brought with them rand strength. Or, to put it another way: what can and should be done to increase the demand for foreign exchange from SA, to perhaps hold back rand strength and in ways that will serve the economy and all those dependent on it?

Just grow faster and do all we can to encourage faster growth

The short answer is to use the opportunity presented by the abundant supplies of foreign capital behind rand strength to encourage the economy to grow much faster. The abundance of foreign capital and the strength of the rand scream out for faster SA growth. Faster growth might inhibit rand strength – though this is not certain given the influence of faster expected growth on the willingness to invest directly in SA. But even should faster growth not lead to a degree of accompanying rand weakness (due to the prospect of faster SA growth attracts more foreign direct investment), faster growth will surely be very welcome even if not accompanied by a degree of rand weakness.

Our call for policies to promote growth will not be surprising to our readers since we have been calling for such responses all year. We have called for urgent steps to be taken to revive household spending in the form of lower interest rates, accompanied by faster money supply growth: that is for quantitative easing to encourage the banks to lend more. The Reserve Bank therefore should be active in buying forex and by so doing adding cash to the system, and the extra cash should be accompanied by lower interest rates.

Perhaps one of the investments the Reserve Bank could usefully make with the dollars it buys in the market would be in foreign currency denominated RSA debt. This would improve both the government balance sheet and provide a very useful reserve for the time when SA government debt becomes less actively sought offshore

Encourage outward investment by institutional investors

The other steps to be taken to counter rand strength would be to encourage outward investment by SA fund managers. Listings of foreign companies on the JSE in which South African fund managers can invest freely – without limitation of foreign investment allowances – should get every encouragement. This is a very good time surely for the managers of SA retirement and pension funds to diversify some of the exposure to the SA economy of their clients. This will help build reserves in the form of offshore investments which can be drawn upon when circumstances in SA become less favourable. If such flows off shore help restrain rand strength for now, so much the better.

We have updated our indicator of the current state of the economy we call the Hard Number Index. It is based on hard numbers, namely vehicle sales and the Reserve Bank note issue adjusted for the Consumer Prices Index extrapolated for an extra month. The advantage in applying these hard numbers is that they are updated within a week of month end. All other published indicators of the state of the economy are as much as three or more months behind the times. Moreover the numbers that make up our very up-to-date Hard Number Index of Economic Conditions are actual accurate numbers not estimates based on sample surveys.

We have demonstrated that the Index tracks the business cycle represented by the coinciding business cycle indicator of the SA Reserve Bank very closely and the relationship has been an especially close one recently, as we show below. The Reserve Bank business cycle indicator however is only updated to June 2009 as is also shown.

Hard Number Index: Compared with the Reserve Bank Coinciding Business Cycle Indicator (2000=100)

Source: I-Net Bridge, SA Reserve Bank and Investec Private Client Securities

A closer inspection of the Hard Number Index and its annual rate of change (which should be regarded as the second derivative of the business cycle) indicate that the SA economy is now finally showing signs of a bottoming out. The Index itself, while still in decline, is now falling less rapidly. If present trends continue we can look to an actual increase in economic activity within the next month or two.

The Hard Number Index: The first and second derivates of economic activity

Source: I-Net Bridge, SA Reserve Bank and Investec Private Client Securities

A recovery despite further declines in the growth in Reserve Bank cash

This promised revival in economic activity owes little to the supplies of cash provided by the Reserve Bank to the system. No such assistance of the kind offered by many central banks has been made available to SA banks. The growth in the SA money base defined as the supply of notes issued by the Reserve Bank plus cash reserves banks held with the Reserve Bank, less required reserves, continues to slow down as we show below. But as we also show, the growth in the Real Money Base has stopped declining because the inflation rate has slowed down; and promises to slow further. Less inflation to come will add impetus to household spending in the months to come.

Real and nominal money supply growth

Source: I-Net Bridge, SA Reserve Bank and Investec Private Client Securities

The vehicle cycle has reached a deep bottom

Vehicle sales, having first turned negative in early 2007, now also appear to have bottomed out as we show below. What higher interest rates took away from vehicle sales, lower interest rates are very slowing adding something back, though if recent trends are to be extrapolated until year end 2010 the revival in sales will be a modest one (See below).

New Vehicle sales

Source: I-Net Bridge, SA Reserve Bank and Investec Private Client Securities

The sources of recovery are to be found outside of the Reserve Bank

The long awaited recovery in the SA economy will have little to thank monetary policy for, especially if the impulse of monetary policy is measured by the growth in money supply or bank credit rather than policy determined interest rates themselves. These have declined by 500bps since December 2008 but as yet lower interest rates, in the absence of quantitative easing, have not revived bank lending or the money supply. The economy has suffered a deep recession and the recovery prospects are for at best a slow recovery.

The recovery will be encouraged by the confidence that comes with the knowledge that the global credit crisis is over and the global economy is recovering. Relief of this kind also percolates through to SA business and their investment decisions while also encouraging the foreign demand for goods and services from SA. The improved global tolerance for risk has boosted values on emerging equity markets and the JSE, realising positive wealth effects. By boosting the value of the rand these improving trends have also helped lower inflation in SA and will continue to do so. We can look to lower inflation to boost the real money supply even if the Reserve Bank, unfortunately in our opinion, continues to resist doing so.

A most interesting article in the latest Barron’s by Michael Santoli (Leaving With the One Who Brought You, Barron’s Online, Monday 12 October) points to the opportunities and pitfalls provided by a highly receptive market for high grade corporate paper. Santoli observes:

Any CFO of a high-investment-grade large company who reaches for a phone to call his or her banker in the morning will have multiple hundred millions of cheap, no-strings debt financing offered up by bond-fund managers before happy hour. Or so it seems. Companies that really don’t need the money can – and are – selling bonds at will.

While the bond market is highly solicitous of new paper the share market can be very critical of the purposes to which this newly found balance sheet strength is being put.

To quote Santoli:

In the recent wavelet of M&A action, a particular sort of corporate transaction has been applauded. To specify: When large, self-financing, market-leading companies have deployed their balance sheets to opportunistically grab for unique and easily digested assets, investors have celebrated.

Moving from the warmth of the market’s hearth to its chilly woodshed, we can find the would-be acquirers swiftly punished by investors for the transgression of bidding generously for a business in an adjacent market and, in so doing, negating the reasons so many shareholders owned the shares in the first place.

Recent deals that have earned the strong disapproval of the market referred to were the moves made by Kraft Foods and Xerox, for Cadbury and Affiliated Computer Services respectively.

As Santoli opines: “In both cases, a shareholder base that owned the buyers’ stocks for their steady, cash-flow-generating attributes woke up in alarm as management opted to pay large premiums for companies that the shareholders could themselves have owned more cheaply the prior day, and whose integration might not be effortless.”

In other words shareholders have been rudely reminded that they do not control the free cash flow generated by the companies they invest in. These cash flows remain largely at the mercy of management who have their own interests to pursue that are not necessarily consistent with the interests of shareholders.

This reminds us of M&A activity on the JSE and in particular the attempt by MTN to buy a big chunk of Bharti, which was frustrated by regulatory issues. The deal falls decidedly into the category of free cash flows at risk. MTN is a company with a strong balance sheet and one presumably easily able to issue more debt. Its free cash flow from its current operations is growing rapidly and is expected to increase from an estimated R8.6bn at 2009 year end to over R16bn at year end 2011 (by Jonathan Kennedy Good of Investec Securities).

This improvement in free cash flow, absent of acquisitions, is estimated despite an ambitious accelerated programme of capital expenditure over the next few years designed to roll out its network in under serviced Nigeria and Iran. Capital expenditure would then be expected to taper off in the absence of acquisitions or, less likely, to till large new green fields for voice or data transmission.

It should be fully appreciated that MTN in its dealings with Bharti was decidedly on the trail of the utilisation of cash and borrowing facilities. While MTN planned to issue more equity to Bharti (issues of approximately R59bn of equity was proposed) MTN had additionally committed to pay cash of some US$2.9bn (approximately R22bn) for its stake in Bharti. Clearly additional MTN debt would have had to have been issued to this purpose and we understand negotiations had been entered into with banks to this purpose. Bharti, in its turn, proposed to exchange newly issued shares as well as cash with MTN shareholders for part of their stake in MTN.

Presumably shareholders in MTN are not surprised by MTN’s appetite for acquisitions, especially in the light of much improved credit market conditions. Shareholders in MTN would have even less reason than those of Kraft or Xerox for believing that the cash flows that emerge from maturing operations will increasingly flow their way.

The big issue for shareholders in MTN is not whether or not they will control the free cash flow emanating from MTN, but rather how much return on capital they should expect from management exercising their ambitions. Will the assets they buy prove “opportunistically cheap and easily integrated” or will MTN overpay “for businesses in adjacent markets that shareholders could access cheaply on their own”.

MTN’s great value added for its shareholders by rolling out operations in South Africa, Nigeria and Iran could be regarded as of the first kind of investment. But the scope to exploit virgin telecom territory is increasingly limited. The Investcon acquisition, an investment in adjacent markets, might well be regarded as value destroying, judging by the returns so far realised on the extra capital employed.

Shareholders in MTN should seek good answers to this question of prospective return on debt and equity capital when MTN management comes around again, as they are most likely to do, to seek approval for an acquisition that would commit a large proportion of the potential cash flows from operations. Strong balance sheets that comfort debt holders are always a powerful temptation for managers – they allow managers to raise and invest capital both internally and externally derived – with often unfortunate consequences for shareholders.

Growth in earning that comes with the expectation of improved returns on capital at risk is the magic that drives share prices higher. Growth in earnings that promises to reduce the return on shareholders capital below its opportunity cost clearly punishes the value of a company to its shareholders, though not necessarily its managers.

MTN has made great value adding investments that shareholders have applauded. MTN may well be embarking on a growth course through acquisition that will realise below cost of capital rewards. This fear is presumably holding back its share price.

The MTN’s share price does not appear to carry any optimistic forecasts of improved flows of cash to shareholders. What would happily surprise the market would be an indication that MTN would not be making major acquisitions, and or that it intends to be much more demanding of a high return on capital from any acquisition it might make – including that of Bharti shares.

Ideally for shareholders, MTN would announce it is no longer interested in acquiring other established telecom companies and that it intends to focus entirely on realising the organic growth or green field opportunities that still present themselves. Then shareholders could anticipate a very healthy flow of cash over the next few years that they could hope to deploy in cost of capital beating ways should MTN be unable to do so.

The gold price is at record levels when measured in US dollars. When measured in the mighty rand it is however well below its record levels of November 2008. Part of the strength of gold is the weakness of the US dollar.

The gold price in US dollar and rands; Daily data

Source: I-Net Bridge and Investec Private Client Securities

But gold lately is not exceptional

In recent months the gold price in US dollars has not behaved exceptionally: it has closely tracked commodity prices in general as the dollar weakened and the signs of a global economic recovery were read (See below).

Gold Price vs All Commodity Prices CRB Index (January 2009=100), Daily data

Source: I-Net Bridge and Investec Private Client Securities

Gold was very special a year ago

Gold was special when the credit crisis reached its apogee with the failure of Lehmans in September 2008, when it showed admirable defensive qualities and performed very much as a safe haven.

Gold vs Commodity prices 2008-2009 (Jan 2009=100), Daily data

Source: I-Net Bridge and Investec Private Client Securities

History tells us that gold, that barbarous relic (as Keynes described it with characteristic intellectual scorn), is more than just another commodity – it has always been a special store of value and is especially useful when the value of all other assets is threatened by war or financial crises, as has again been proved.

It took very special events to prove that gold is special

But as we show below, a sharp divergence between the trend in gold and other commodity prices, as occurred between September 2008 and March 2009, has been a unique occurrence over the past 30 years. It took the fear of a melt down of the banking and credit system to lead to a rush to gold and a liquidation of other commodities. Mere inflation fears, if that were the driver, would be common to precious and ordinary metals and minerals.

The gold price and the commodity price index (CRB) (Jan 2009=100), month-end data

Source: I-Net Bridge and Investec Private Client Securities

In ordinary times gold is very likely to behave in line with other metals and minerals

The state of the global economy and the balance between the real demand and supply of commodities will be a primary driver of real (after adjusting for inflation) commodity prices. However all asset prices, including especially hard assets in the form of gold and other metals and minerals that can easily be stored, are influenced by inflationary expectations, or more particularly by the prices of these commodities that are expected to prevail in the months and years ahead.

The cost of storing gold and metals is very important for speculators

These price expectations have to be compared with the cost of storing metals and minerals which in the case of precious metals largely comes in the form of financing costs. The cost of storing precious metals – unlike the cases of copper, coal, iron ore or even oil – is almost all financing costs, given the high value to size ratio that determines the cost of storage.

Financing costs rise with inflation too

Financing costs, that is interest rates, however also rise with more inflation expected, so increasing the costs of storage and discouraging the demand to hold commodities. Thus there has to be more to a rising price of gold and other commodity prices than inflationary expectations. The price of gold, to make it worth buying at current spot prices, has to be expected to rise faster than the costs of owning gold in the form of interest rates paid or foregone. Or in other words, the price in the future must be expected to rise faster than the costs of financing that is explicit in the ratio of the spot and future price of gold.

It is real interest rates, not inflationary expectations, that matter

Thus a key determinant of the current price of gold will be the relationship between inflationary expectations and interest rates – that is to say real interest rates. Real interest rates have fallen to very low levels in recent years and months. They are at half the levels prevailing in the early years of this century. These real rates are best measured explicitly in the yields on offer from government bonds that come with complete cover against inflation – the inflation linkers – known as TIPS in the US, for Treasury Inflation Protected Securities (See below).

The purchasing power of the fixed coupon payments to be made to the owner of a conventional bond will be fully diluted by inflation. Thus inflation exposed bonds have to offer compensation for expected inflation. Thus the yield gap between the lower yield on inflation linkers and the higher yields on long dated conventional bonds is explicitly the compensation on offer for bearing inflation risk.

The bond market is very complacent about inflation to come

This compensation currently on offer to the holder of a 30 year US Treasury Bond is but an extra 2% pa. Thus it may be said that investors in 30 year bonds are highly vulnerable to losses should inflation in the US average more than 2% pa over the next 30 years – that is to say there is very little inflation expected or little cover against higher inflation currently on offer in the conventional government bond market as we also show below. Thus there is very little inflation expected in the bond market where the fear of deflation rather than inflation is dominant. That the idea that the gold price is being driven by inflationary expectations that are absent in the bond market, does not seem at all consistent.

US government bond yields and inflation compensation, month-end data

Source: Federal Reserve Bank of St. Louis, I-Net Bridge and Investec Private Client Securities

A consistent explanation for the rising gold and other metal prices

It would be far more consistent to conclude that the gold price, as with other commodity prices, is being driven by a global recovery and low real interest rates, that is abnormally low costs of storing gold and other commodities. The evidence in the relationship between the gold price and real interest rates in the US, represented by the yield on 30 year US TIPS is very supportive of this explanation. The gold price rose consistently with the equally persistent decline in real interest rates after 2000. It may also be seen that the gold price fell away as real yields rose temporarily as deflation fears gripped the markets in 2008 and then recovered as real interest rates fell back again.

Real interest rates and the Gold price 2000-2009; Month end data

Source: Federal Reserve Bank of St. Louis, I-Net Bridge and Investec Private Client Securities

A better case for gold in portfolios

The case for gold cannot be based on inflationary expectations alone. If inflation rises unexpectedly, interest rates and so the financing costs in owning gold will also rise, taking the gloss off gold and other metals. Thus it will take lower real rates – or interest rates lagging well behind actual inflation – to drive the price of gold and other metal prices higher. Unexpectedly strong global growth especially when coupled with relatively low real interest rates will be especially helpful to the gold price as it will be to all commodity prices. Gold may not prove special in a world of rising commodity prices as real demand presses against real supplies but yet well worth holding.

The case for an insurance premium for gold

But the recent evidence that gold can still provide insurance against calamity is surely reason to keep more gold in portfolios than before as insurance against true calamity. The experience of the defensive quality of gold in 2008 when gold held up while the price of all other metals fell away could add to its long term attractions so adding a little special lustre compared to the more prosaic other metals. Global portfolios still contain but a sliver of gold – should portfolio managers decide that a little gold may provide useful insurance as it did in 2008 – the gold price could move permanently higher relative to other metals and minerals and maintain such a premium. Brian Kantor

We remain optimistic about equities generally, yet we do not expect JSE Resources to out- or under -perform the market generally.

JSE performance is often in the mix of resources vs other sectors

South African managers of balanced equity funds usually stand or fall by their judgments about the mix of resources, industrial or financial stocks in their portfolios. Resources can out or under perform by large orders of magnitudes as we show below.

JSE Resources Vs Industrials vs Financials (18 Sept 2008=100)

Source: I-Net Bridge and Investec Private Client Securities

Extreme relative moves were experienced in 2007-2008

Fifteen months ago, by mid 2008 when compared with a year before, the JSE Resource Index had outperformed the Financial Index of the JSE as much as 60% and had gained 40% on Industrials. Within a few short months, when the credit crisis was at its height and commodity prices collapsed, Resources had fallen more than twice as far as Industrials or Financials.

The JSE sectors have moved in line over the past twelve months

Over the past twelve months after the fall and with the strong recovery from March 2009 in commodity prices and emerging equity markets, all the major sub sectors of the JSE have performed more or less in line. The annual return on JSE Financials and Industrials have been about five per cent ahead of Resources and all sectors have moved into positive annual return territory.

Resources/Industrials and Resources/Financials (Sept 2008=100)

Source: I-Net Bridge and Investec Private Client Securities

What matters for relative and absolute JSE performance is not rand strength or weakness – but the causes of rand strength or weakness

The key to the out- or under-performance of the Resource sector is not simply, as many would be inclined to suggest, simply rand weakness or rand strength. Rand weakness will only be especially helpful to Resources and harmful to Financials and Industrials if the cause of rand weakness is South African specific. For example if some SA political development causes investors both locally and abroad to raise their risks of doing business in South Africa causing an outflow of funds and rand weakness, Resources will do better than Financials or Industrials. Vice versa if an improvement in sentiment causes the rand to strengthen, when the rand plays will outperform the rand hedges.

Mid 2006 to mid 2008 was an ideal time to be exposed to JSE resources

A combination of the kind of rand weakness experienced in 2006-08 coupled with stronger commodity markets represents ideal circumstances for JSE resource valuations. We show in the figure below how the rand weakened against the Aussie dollar (another commodity currency) in 2006-07 despite commodity price strength; and so Resources performed well absolutely and in a relative sense, outperforming handsomely the other JSE sectors. We also show how the rand recovered some of its losses and has held its own against the Aussie dollar over the past 15 months. Resource valuations came under particular pressure from the combination of weaker commodity prices and a relatively stable rand.

JSE Resources/Industrials, Commodity Price Index and the ZAR/AUD (Sept 2008=100)

Source: I-Net Bridge and Investec Private Client Securities

Rand strength for fundamental reasons is good for the JSE, but not especially good or bad for JSE Resources

When the source of rand strength or weakness is to be found outside South Africa, in the form of global economic strength which leads to stronger global commodity and emerging equity markets, there will be no reason to expect resources to out- or under-perform other sectors of the JSE. This has been the case recently. The rand has strengthened because of the recovery of the global economy led by emerging economies. The rand is stronger because of much firmer emerging equity and commodity markets.

The recent strength in commodity prices has been helpful for Resource company valuations on the JSE as well as those of the rand hedges (companies with a substantial part of their business outside South Africa). The strength in commodity and emerging equity markets has simultaneously boosted the rand and so the South African economy plays listed on the JSE have kept pace with the JSE generally.

The case for increasing exposure to the JSE equities at the expense of bonds must be based on a belief in rand strength for global reasons. What is good for the rand in the global economy will be good for the JSE, resources included. Rand weakness for global and SA specific reasons would be a reason for seeking less exposure to equities generally even though resources are likely to suffer less than average damage in such unhappy circumstances.

Our view is that the recovery in the global economy will continue to be helpful to JSE equities and the rand and so there are no SA specific reasons for strongly preferring resources over the other sectors or for reducing exposure to them. While continuing to overweight equities we would continue to recommend a broadly neutral mix of Resources, Industrials and Financials.

Brian Kantor, Professor Emeritus, University of Cape Town, Investment Strategist, Investec Private Client Securities.

and

Chris Holdsworth – Analyst, Investec Securities

Abstract

This study demonstrates with the aid of single equation regression analysis the role global capital markets play in determining the behaviour of the Johannesburg Stock Exchange (JSE ALSI) the Rand/ US dollar exchange rate (ZAR) and long term interest rates in South Africa on a daily basis represented by the All Bond Index (ALBI) or long term government bond yields represented by the R157. It will be shown that since 2005 the state of global equity markets, represented in the study by the MSCI Emerging Market Index (EM) has had a very powerful influence on the JSE. The EM Index is shown to have had a less powerful yet statistically significant influence on the ZAR while it is also demonstrated and that conditions in global capital markets, and the ZAR have had some weak but statistically significant influence on the direction of long term interest rates in South Africa. It will be demonstrated that movements in policy influenced short term interest rates, have had very little predictable influence on share prices, the ZAR or long term bond yields. The causes as well as the consequences of the ineffectiveness of policy determined interest rates for monetary policy are further analyse.

Introduction

This study demonstrates the role global capital markets play in determining the behaviour of the Johannesburg Stock Exchange (JSE ALSI) the Rand US dollar exchange rate (ZAR) and long term interest rates in South Africa on a daily basis represented by the All Bond Index (ALBI) or long term government bond yields represented by the R157. It will be shown that since 2005 the state of global equity markets, represented in the study by the MSCI Emerging Market Index (EM) has had a very powerful influence on the JSE.

The EM Index is shown to have had a less powerful yet statistically significant influence on the ZAR while it is also demonstrated and that conditions in global capital markets, and the ZAR have had some weak but statistically significant influence on the direction of long term interest rates in South Africa. It will be demonstrated that movements in policy influenced short term interest rates, represented by daily changes in expected short term interest rates, represented by daily movements in the implicit JIBAR 3 month forward rate (Jib3f3) have had very little predictable influence on share prices, the ZAR or long term bond yields.

The MSCI EM Index may be regarded as a proxy for conditions in global capital markets that affect South Africa. JSE listed shares are included in the EM Index with a current weight of about 7%. The more abundant the capital available for emerging market capital raisers, that is to say the less risk aversion prevailing, the higher would be the level of the EM Index – and vice versa.

Changes in the forward JIBAR rate are used as our proxy for short term interest rates on the presumption that it is interest rates expected, rather than current actual interest rates that drive the value of shares, bonds and currencies and that therefore changes in expected short term rates rather than changes in actual rates- that may well have been anticipated – have significance for the financial markets.[1]

Exchange rates inflation and the implications for monetary policy

The implications of this finding for monetary policy are surely serious ones. It would strongly suggest that policy determined adjustments to short term interest rates, when unexpected, will not influence the exchange rate in any consistent way. If so adjustments to short term interest rates cannot be regarded as a reliable anti-inflationary tool, given the influence exchange rates have on measured inflation rates in SA. The feed back effect of the exchange rate on import export and domestic prices is clearly a very important influence on the measured rate of inflation

The case for interest rate changes as the principle instrument of monetary policy is furthermore not enhanced by the evidence that short term interest rates have not had any consistently important influence on the direction of long term interest rates in South Africa nor on the direction of share prices and therefore on these components of household wealth. However it would seem to be the case that movements in actual short term interest rates can have a significant influence on aggregate demand in South Africa and perhaps also on house prices without necessarily reducing inflation rates. These relationships between interest rates and aggregate demand are not tested here.

Estimation procedures

This study utilises daily data to model and estimate the behaviour of the JSE ALSI the rand/USD exchange rate and the RSA All Bond Index bond index or long dated RSA bond yields (between January 1st 2005 and August 31st 2009. The models using daily data are supplemented with similar models utilising month end data from the mid nineteen nineties to help confirm the strength of the hypotheses tested and to test for structural changes in the economy.

The models are single equation models of daily or monthly percentage movements in the ALSI, the ZAR and the ALBI or as an alternative to the ALBI of daily changes in long term interest rates represented by the long dated RSA 157. The estimation method applied is single equation least squares regression analysis.[2]

The data – represented in figures

The dependent and independent variables of the models are pictured below in level and daily percentage change form. It may be seen that daily changes in all the dependent and independent variables are highly random and that prices, exchange and interest rates they have drifted both higher and lower since 2005. It is also shown below how much more generally volatile share and bond prices and interest rates became during the financial crisis that reached its apogee in September 2008 with the collapse of the large investment bank Lehman Bros. We have measured the volatility of the variables in the form of a 30 day moving average of their Standard Deviations and present this information in graphical form. We demonstrate how similar has been the behaviour of volatility on the different markets. That risks appear so similar in the different markets is further evidence of the globalisation of capital markets. We show that the increased volatility did not materially influence the estimates of the coefficients of the models

Fig1. The JSE All Share Index Daily Levels and % changes 2005 – Aug 2009

Fig2. The ZAR Daily levels and % changes 2005 – Aug 2009

Fig3. The SA All Bond Total Return Index Daily levels and daily % changes data 2005-Aug 2009

We compare in figure 4 below the performance of the rand to both the USD and the AUD to indicate that the rand while holding its own against the weaker US dollar in 2006-07 lost significant ground against what may be considered other commodity and emerging market currencies.

Fig4. The rand Vs the USD and the AUD Daily data (Jan 1st 2009=100)

The independent variables

The explanatory variables considered for inclusion in the models comprise (surprising) daily or monthly movements in forward short term interest rates (JIB3f3) and daily or monthly percentage changes in the MSCI Emerging markets equity index (EM) or in the S&P 500 Index to represent share prices in New York, As shown below the correlation between daily moves in the EM and S&P 500 is very high and other than reporting this correlations with the S&P 500 we did not apply the S&P 500 in the models. Also considered and applied in the various models were percentage movements in global commodity prices in USD, represented by the commodity price index of the Commodity Research Bureau (CRB) and percentage moves in Australian/USD exchange rate (AUD) or (AUS$). The additional explanatory variable applied in the models were changes in US long dated 10 year treasury Bonds.

Fig.5 Emerging equity markets (MSCI EM) and the S&P 500; Daily levels and daily % movement 2005-2009

Fig.6 Expected short term interest rates (Jibar 3 month implicit forward rate) Daily levels and daily changes

Fig7. Commodity Prices and US TB yields. Levels and Daily or daily % changes

Fig8. The Australian/USD exchange rate Daily Levels and % changes. 2005-2009

Representing volatility in graphic form

Fig 9. Volatility of Share and commodity markets. 30 day moving average of the Standard Deviation (SD) of daily % movements

Fig 10. Exchange rate volatilities; 30 day moving average of the Standard Deviation (SD) of daily % movements

We show below the measures of implied option price volatility on the S&P represented by the Vix Index and on the JSE represented by the SAVI

Fig11. Implied volatility – The Vix (on the S&P) and Savi on the JSE Daily data 2005-2009

Volatility and share prices

The increase in the volatility of share prices globally, including on the JSE, that provide indicators of the risks in the markets appears to have had a very negative impact on share prices. The negative correlation between daily percentage moves in the Index of Implied Volatility on the S&P 500, the Vix and daily moves in the S&P 500 itself has been a high negative (-0.76) and between daily moves on the JSE and the SAVI an almost equally negative (-0.73) since May 2005. (See Table 1 below)

Statistics for the SAVI, the implied options price volatility indicator of the JSE, are only available since then. It is surely volatility that drives the share market up and down. It is a much more difficult task to explain and predict volatility. Volatility in share markets may be regarded as abnormally high before 2007 when the global glut of capital was holding down interest rates and encouraging risk tolerance. The financial crisis as we well know reversed all this and produced much higher degrees of risk aversion and volatility as the likelihood of defaults and bankruptcies increased so dramatically, especially after the failure of Lehman Bros.

Table 1. Correlation statistics of daily % changes in volatility indicators with the Share Markets (May 2005- August 2009)

Correlation Statistics and their interpretation