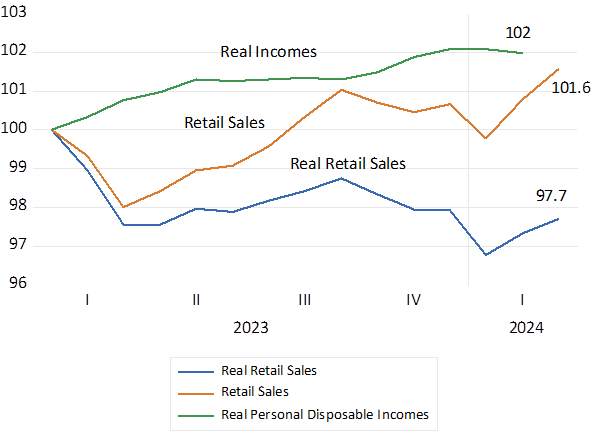

The Trump Triumph demonstrates why inflation in the US and in much of the developed world is persistently low. Inflation is unpopular- it can cost you the next election – especially when the growth in incomes of the workers, wage and salaries, lag the increase in prices. Which they have done in the US until recently, despite the high levels of employment.

The recipe for controlling inflation is well known and usually well practiced. Simply put it requires that the increase in the demand for goods and services be closely matched to the increase in the real supply of goods and services that are the source of all incomes. If demand appears to be growing too rapidly in ways that add to the ability of firms to easily raise their prices, the remedy is to raise the cost of credit – raise interest rates to discourage borrowing to spend more. Actions not beyond the with of a modern, data dependent and politically independent central bank.

A temptation not generally avoided in the persistently high inflation economies, Africa provides many examples, of a central bank and its cohort of retail banks, to fund a large proportion of additional government spending. Then consistent increases in the supply of money ( of bank deposits) and bank lending, stimulate demand for goods services and assets and continuously higher prices, inflation persistently in the high teens, are the inevitable rationing mechanism.

Yet this was the classic way inflation ran out of control in the US post the Covid lock down shocks to supply and incomes. The spending of the US government rose dramatically and generously to compensate workers for their enforced idleness. With the strong backing of the Fed and its willingness to buy the extra government bonds being issued, on a huge extra scale. It was classic money creation and a burst of inflation – more demand and less supplied- followed.

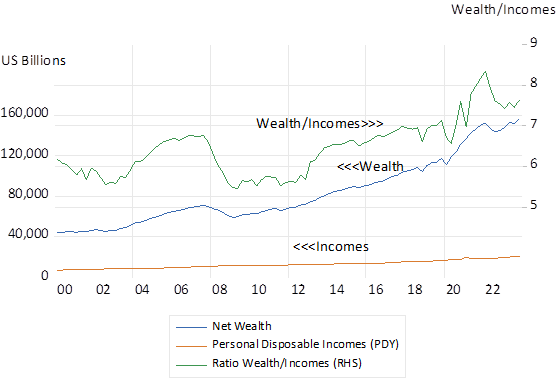

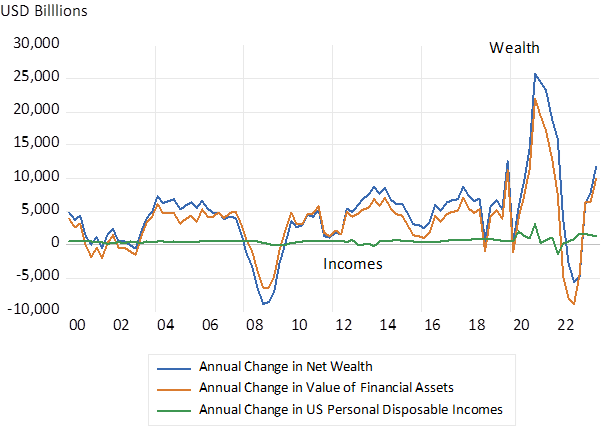

Seemingly, unforgivingly, to the surprise of the Fed who then had to play catch up with much higher interest rates that naturally were very unpopular with potential house and car buyers. The flow of money into financial assets raised their prices and were much welcomed by the minority of wealthy Americans who have enjoyed a massive improvement in their balance sheets. US household wealth is up by over 50 trillion since Covid. US household incomes have barely increased since then- and are barely highr when adjusted for inflation.

But there is now every reason to expect US inflation to stay down around the 2% p.a level it is falling towards. Even should Fed Chairman Powell be replaced. The political case for low inflation has been reinforced. Ironically what the responses to Covid took away from the second Trump campaign- gave it all back in the third.

The South African authorities, especially its independent central bank would like to aim at lower, developed world type inflation rates. South Africans would welcome such outcomes. But is it a realistic objective? The inflation outcomes will depend critically and unavoidably on the path of the exchange rate. If for example, the ZAR more or less retains its exchange value with the Aussie dollar- as it has been doing lately – SA could enjoy similarly low Australian type inflation and interest rates. It would then be a very smooth ride to lower inflation.

But the ZAR is clearly not under the control of the Reserve Bank. It is determined by SA politics and the outlook for SA growth. It is the political risks to the growth outlook for the SA economy and the ability to fund government spending without money creation that drives exchange rate weakness and generally higher prices. Too much spending has not been the reason for SA inflation. The exchange rate shocks for our very open economy have driven prices higher and inflation expectations higher. Limiting demand to counter these forcers acting on prices has meant less growth and not much less inflation.

We must hope that the new political dispensation gives SA more growth and more exchange rate stability. If it does persistently low inflation will follow painlessly. If not chasing the inflation tail will just add to economic misery.

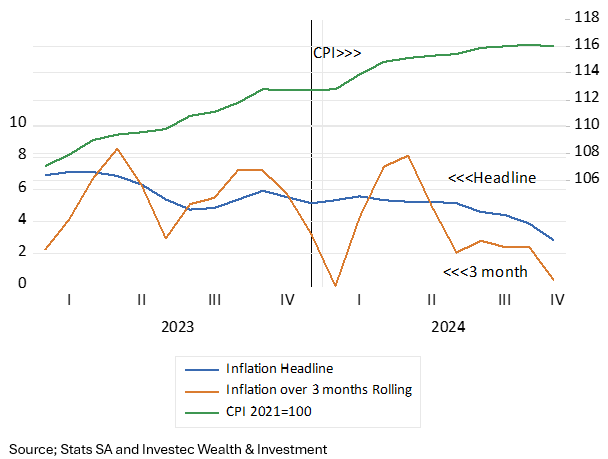

Inflation in SA has nearly halved since June. From 5.1% p.a then to 2.8 in October. Indeed average consumer prices have hardly risen at all since June. In October they fell marginally, and over the past three months the CPI has hardly budged, and price increases were close to zero.

Inflation and the SA CPI; Monthly Data

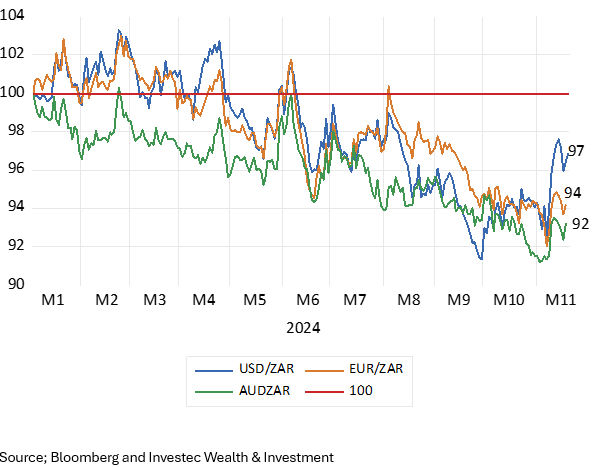

One observation that one can make is that such price stability could not have occurred without a very strong rand. A rand that has gained value against a range of low inflation currencies. This year to date the rand is worth four per cent more USD, can buy six per cent more Euros and seven per cent more Aussie dollars. The year before the rand had weakened VS these currencies by over 10%. Its surely no surprise that inflation in SA accelerated in 2023 and has sharply decelerated this year.

The ZAR Vs the USD, the Euro and the Aussie Dollar. Daily Data (2024=100)

One can also conclude that the exchange value of the ZAR drives the direction of prices in SA – rather than the other way round. SA is a very open economy. Flows of exports and imports account each for about 30% of GDP- of total supply and demand in the economy. What we pay in rands for imports and receive for exports helps determine all prices in a systematic way. You can tell as much at the petrol pump.

And so how then can SA achieve currency strength and low inflation? The answer would also seem obvious enough. Form a government of national unity that is expected to raise growth rates, improve the outlook for SA bonds and equities and so more capital will flow in more than out leads to less rand weakness and inflation expected in the future. Lower long term bond yields, lower costs of capital generally, all reinforce the growth momentum. And with lower inflation short term interest rates decline just as predictably, as they can be expected to rise with rand weakness. Yet expectations of faster growth have to be reinforced with consistent growth enhancing actions. Investors can be encouraged, they can as easily be disappointed.

It is not only in South Africa that politics and the economic policies and outcomes associated with a change in leadership drive the direction of the exchange rate. And depending on the degrees of openness to foreign trade that will then drive the direction of all prices. The exchange rate leads and prices follow, and the exchange moves in response to changes in expectations of returns in the capital market. The exchange value of the USD, the essential reserve currency, is subject to large changes in direction, persistently so, that have little to do with differences in inflation between the US and its principle trading partners. And everything to do with expected returns on capital invested. But will have a significant impact on the profits and growth prospects of businesses that engage in foreign trade.

The DXY is a weighted Index of the exchange value of the USD Vs the major currencies, the Euro, Yen etc.. It gained nearly 50% additional exchange value between 1995 and 2000. It then declined from an Index value of 120 to 70 by the time of the Global Financial Crisis. The dollar since has been on a mostly upward tack since and clearly has received a boost from the Trump ascendancy. From which the ZAR has not be immune but has behaved broadly in line with all other currencies. Dollar strength will be far more easily managed provided the ZAR holds its own with the other low inflation currencies, as it has been doing.

But for the Trump administration the impact of the potentially stronger dollar on trade flows may be far more important than the impact of higher tariffs on imports and the retaliation that may follow and on prices US consumers will pay. The unpredictability of exchange rates, despite low rates of inflation in the developed world, especially of the exchange value of the USD, is a fundamental flaw of global trade and finance that all economies including SA have to cope with.

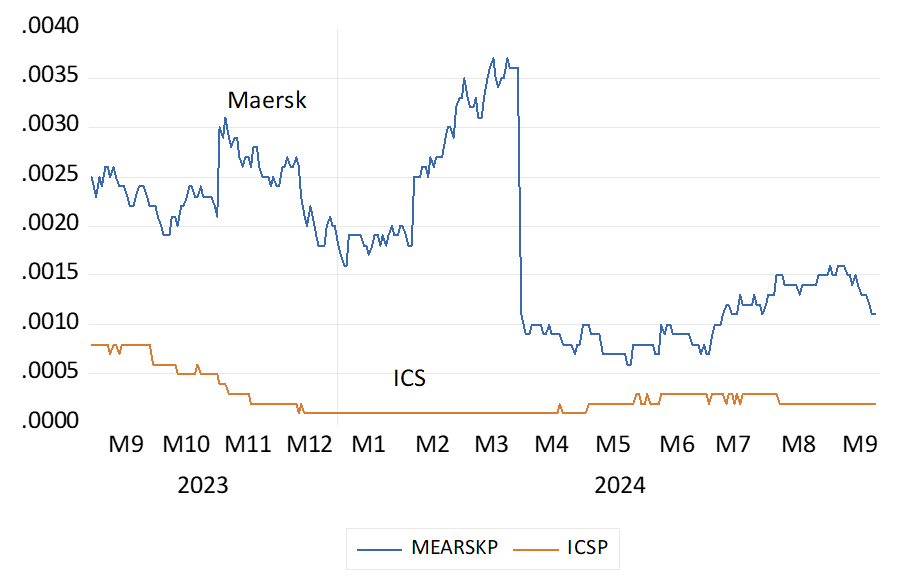

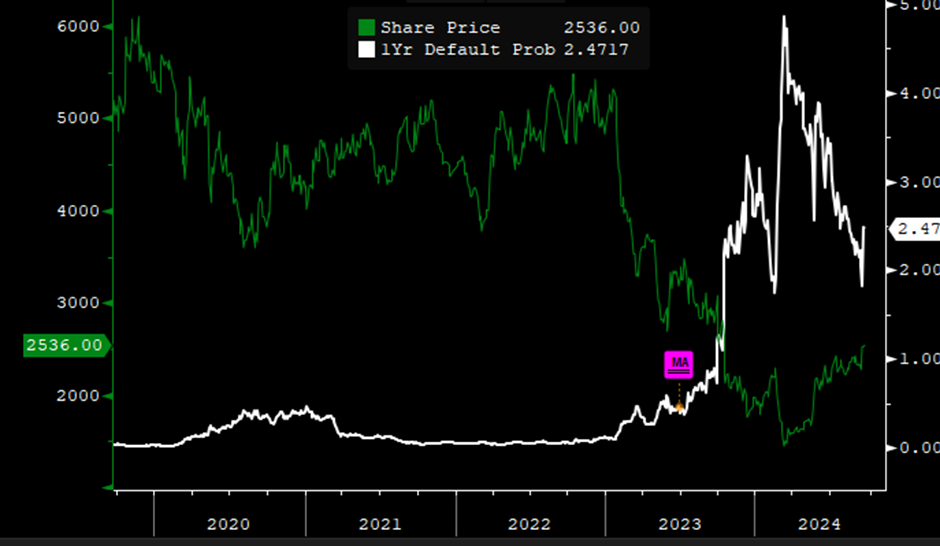

I read with some astonishment, (BD Dineo Faku 22nd September) about the court action taken by shipping company Maersk to overturn the award by Transnet of the Durban Container Port Tender to the Philippine Company International Container Services (ICS) On the grounds that the ICS tender should have been disqualified because it, only it, used its share market value rather than its book value to calculate and report its “solvency ratio”

It would seem obvious that a borrower is solvent when the value of its assets, should they have to be realised, is expected to exceed the value of debts it has incurred. And the closer the ratio of market value to debt the greater the danger that the company would be forced to wind up. If the company is listed its market value is clear and explicit and continuously available. The book value of a private company might be the best initial and readily available estimate of what the assets might realise. If the accountants for the firm have following recommended good practice and have been consistently marking the books to market.

As I write the market value of shipping giant Maersk is 25.9 billion dollars with total debts of 16.7 billion US dollars ( 1.6 times) and that of ICS with a market value of 15 billion dollars, with total debts of 4.16 billion dollars. (3.6 times) The earnings before taxes to interest paid ratio is similar for the two companies 4.5 times for Maersk and 4 times for ICS.

There is a rigorous test of Corporate Default Risk applied to any listed company anywhere, more than 65000 of them, including Maersk and ICS. A test no further away than your nearest Bloomberg Terminal. A click or two calling up the company and the DRSK model will give you an immediate probability of default. And one that will be closely allied with the conventional ratings provided by the debt rating agencies. The Bloomberg model easily downloaded is adapted from the original financial economics of Nobel laureate, Robert C Merton, and is very well known in financial economics. The theory as adapted by the Bloomberg team in 2021 is elegant and is very well tested by the evidence presented of its predictive power. Science, that is theory with predictive power for a large sample is at work here.

The Bloomberg model uses the market value of the assets of a company as the basis of its assets to debt ratios. But with an important proviso. The market value of a company in the model is adjusted for the volatility of its share price . The market value is estimated as a “down and out” call on the assets with a maturity date. Hence providing a highly realistic estimate of what you might realise the assets for. The more volatility, the less predictable the share prices and the less the company may be expected to fetch

The Bloomberg model gives very similar measures for the very low probability of either Maersk or ICI defaulting over the next twelve months. (see below) Both companies, as predicted by Bloomberg, would enjoy a comforting Investment Grade rating. The market value of ICS has risen strongly over the past twelve months while that of Maersk has changed little. The volatility of the two share prices- until recently higher for Maersk, is now very similar. The improved value of ICS may well have much to do with winning the tender. It clearly is a valuable contract worth fighting over.

The Maersk and ICI share prices. Daily data (2023-2024) US dollar value.

Source. Bloomberg and Investec Wealth & Investment

Maersk and International Container Services. Probability of Default; over the next 12 months. %

Source. Bloomberg and Investec Wealth & Investment

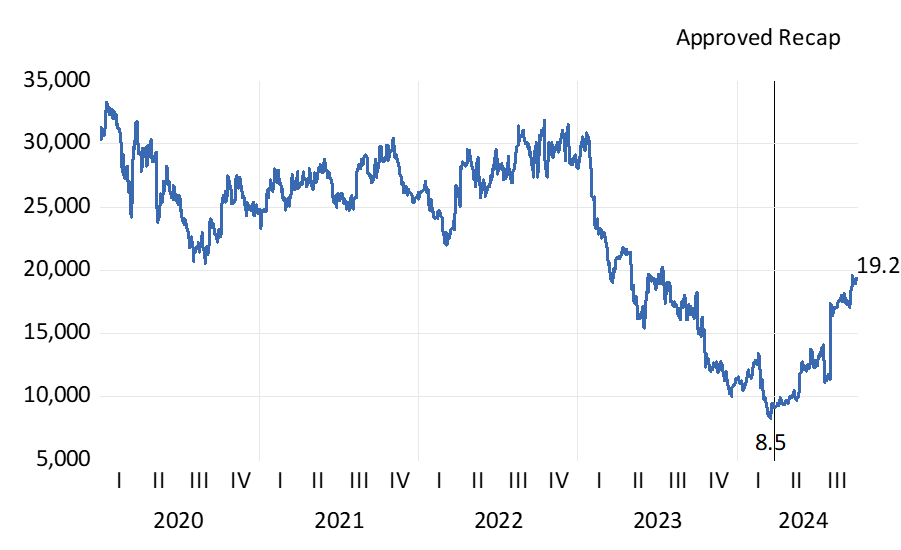

A South African Case Study Pick N Pay (PIK)

Underperforming companies raising more debt do not necessarily go broke when the market value of their assets approaches the barrier of debt. They may be rescued by shareholders willing to subscribe additional equity capital. When shareholders prove unwilling to provide support a company will go under. Hence the market value of a highly indebted company, close to default, will always reflect the chances of a rescue.

South African retailer Pick ‘n Pay (Pik) has provided a very clear example of the benefits of shareholders coming to the rescue with additional share capital necessary to avert the dangers of a default. The operating performance of the company had deteriorated significantly in recent years. A drain of cash had been funded with much additional debt. Net debt had increased from R3.8 billion in August 2023 to R7.2 billion by January 2024. As the market value of Pik declined from 28.02 billion in January 2023 to R11.48 billion by year end 2023 with elevated daily volatility.

A recapitulation of the business had become essential for the survival of the business and was announced in January 2024. The plan was to raise R4 billion from existing shareholders in the form of a rights issue. To be followed by the listing of and an offering of shares in its profitable subsidiary company Boxer. Bankers also agreed to modify their debt covenants in February 2024.

On the 27th February 2024 the company announced the approval of the capital raising and debt reduction scheme. At which point in time the market value of Pik bottomed out at R8.5b. The rights issue when concluded on July 30th raised the number of shares in issue by as much as 51%.

The market value of Pik is now approximately R19b. Thus, the capital raise of R4 billion must be regarded as having added much value for the shareholders subscribing the extra capital. The value of Pik is now up by approximately R10.7b (19.2-8.5) March 2024 after an investment of R4 billion That is for the initial subscription of R4 billion the shareholders have gained R6.7b. (10.7-4)

Source; Iress and Investec Wealth & Investment

The recent history of Pik – its share price and probability of default as calculated by the Bloomberg model – is shown below. As may be seen the probability of default rose sharply as the share price fell away with heightened volatility. The probability of a default in 12 months has now receded sharply placing Pik debt if it were to be rated in the High Yield category. (see below)

Pick ‘n Pay Probability of Default and Share Price. Daily data

In years to come the 2023-24 years will be recognized as very special ones for share owners. Something to toast over what may prove to be an equally special Grand Cru. One that, thanks to the exceptional draw up in market values, has become more affordable to the patient investor. A case of what the wine cognoscenti might describe as linearity- from much extra wealth created to the wine cellar. Though why a straight uncomplicated line from lips to throat, should be regarded as an attribute of a fine wine escapes me. I thought one pays up for complexity in wines, never simply described.

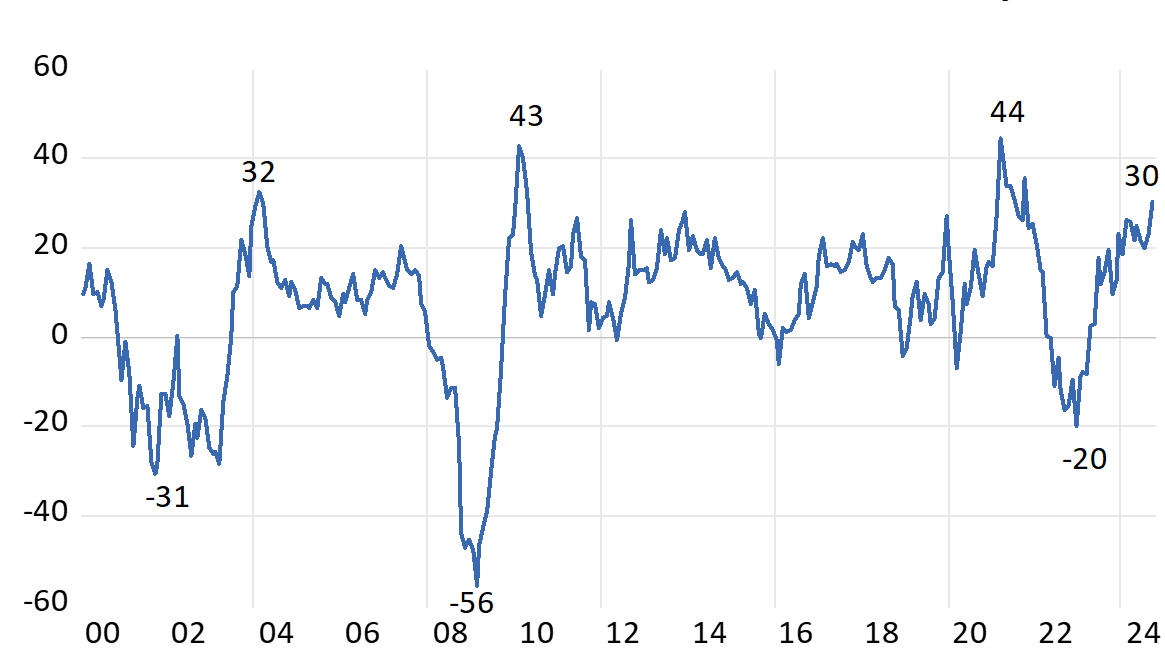

This past year the S&P 500 delivered the best annual returns this century. Comparable to the recovery from the panic drawdowns of 2008 (GFC) or 2020 (Covid) The Index, up 30 % in the twelve months to September 2024 was very generously valued a year ago -at 21 times earnings. It is now even more expensive and valued at 25 times reported earnings. The average S&P P/E since 2000 has been 19.7 times. Unusually It has not taken a draw down to lead a strong recovery. This time has been different. Strength on Strength.

The S&P 500 Index Annual Returns – calculated monthly 2000-2024

Source; Bloomberg and Investec Wealth and Investment.

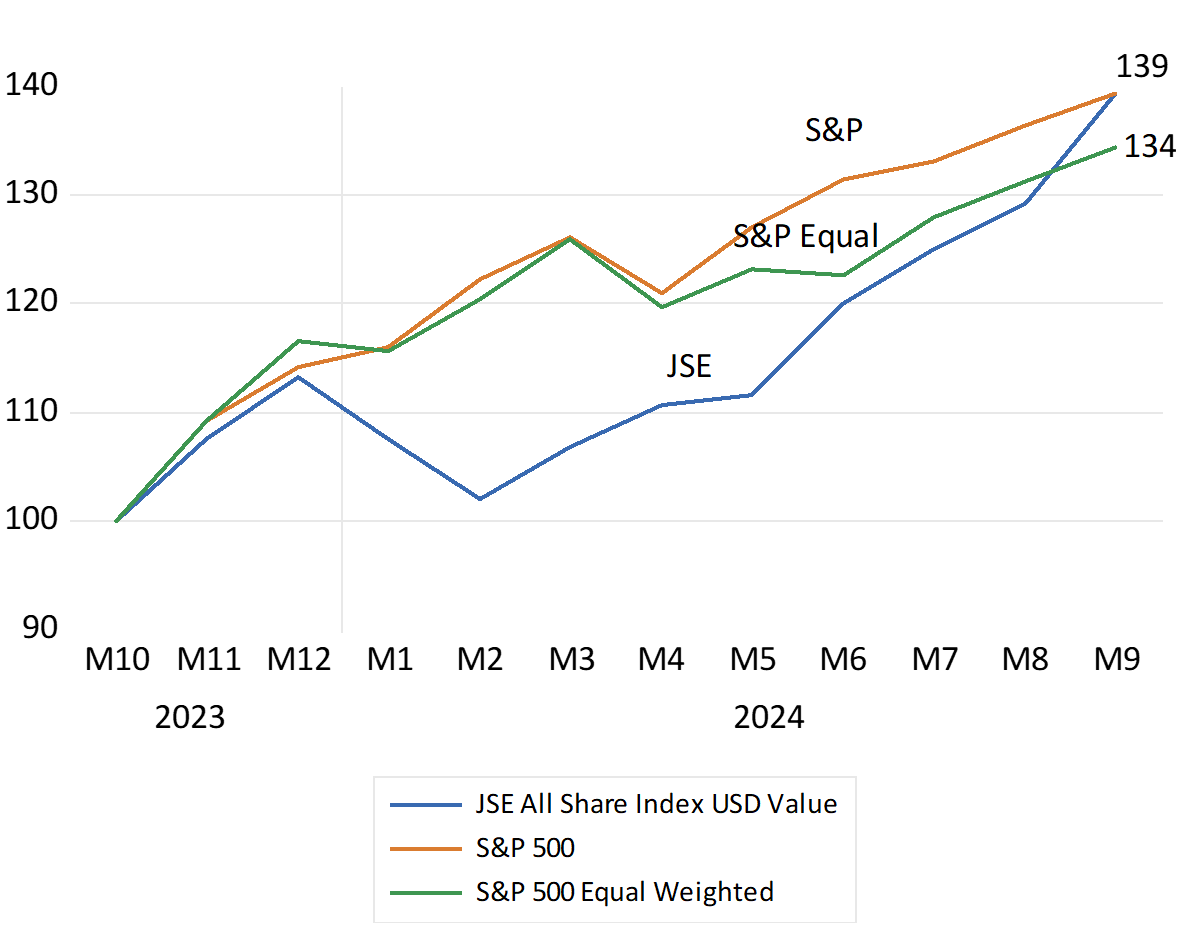

The upward direction of the S&P Index recently has been dominated by a few stocks- the so described magnificent seven- making the Index unusually concentrated, less diverse and therefore more risky than usual. The top three by market value Microsoft Corp., Apple, Inc., and Nvidia Corp., constituted 20% of the S&P 500 this year, while the top seven stocks accounted for 32%.

Yet while the S&P 500 is up 22% this year to September, the equal-weighted S&P 500, the average listed company, is up by less – a mere 14.9%. During the first half of the year, the S&P 500 rose by 15.2%, and by 5.9% in Q3, while the equal-weighted S&P 500 increased by only 5% over the same period. This greater than 10% performance gap between the weighted and unweighted indices was the widest in nearly 30 years. Only about a quarter of S&P 500 stocks kept pace with the market’s overall return during the first half of this year, with over a quarter experiencing negative returns. If you did not own the very largest stocks and own them in size, you likely underperformed the indices. Risk (less diversification) and return were as usual well correlated.

The “magnificent seven” and so the market are valued for the prospective growth in the demand for artificial intelligence that they supply the backbone for. But their investment case so strongly appreciated will only be fully revealed over time. This makes their valuations less dependent on near term earnings and so on the essentially short-term business cycle. They are valued much more idiosyncratically than your average value company on their own recognizances. They have also grown earnings and cash flows at well above the average rate to date. These super growers with impressive track records are allocating truly massive volumes of internally generated cash flows to supplying the essential facilities that the average firm will be drawing upon and hopefully paying up for. They also have the financial strength to pay dividends and buy back shares. In contrast, the average S&P 500 company is valued more heavily on the short-term outlook for the U.S. economy. About which there has been and perhaps will always be considerable uncertainty.

The S&P 500 Index, the equally weighted S&P Index and the JSE All Share Index. Total returns to October (2023=100) USD Values

Source; Bloomberg and Investec Wealth and Investment.

The JSE has also enjoyed a very good year. Up by as much as the S&P since October 2023. 40% in USD and still impressively 28% higher in the mighty ZAR. The JSE All Share Index measured has added as much to SA portfolios as would have holding the S&P Index. A wealth adding outcome for old-fashioned reasons. The prospect of faster growth has fired up the share market and the value of RSA bonds and the exchange rate. Less inflation, lower interest rates and faster growth in GDP and government revenues has been very heady stuff. Enough perhaps to add to the prices bid at the Wine Guild Auction and deserving of an early toast to the GNU.

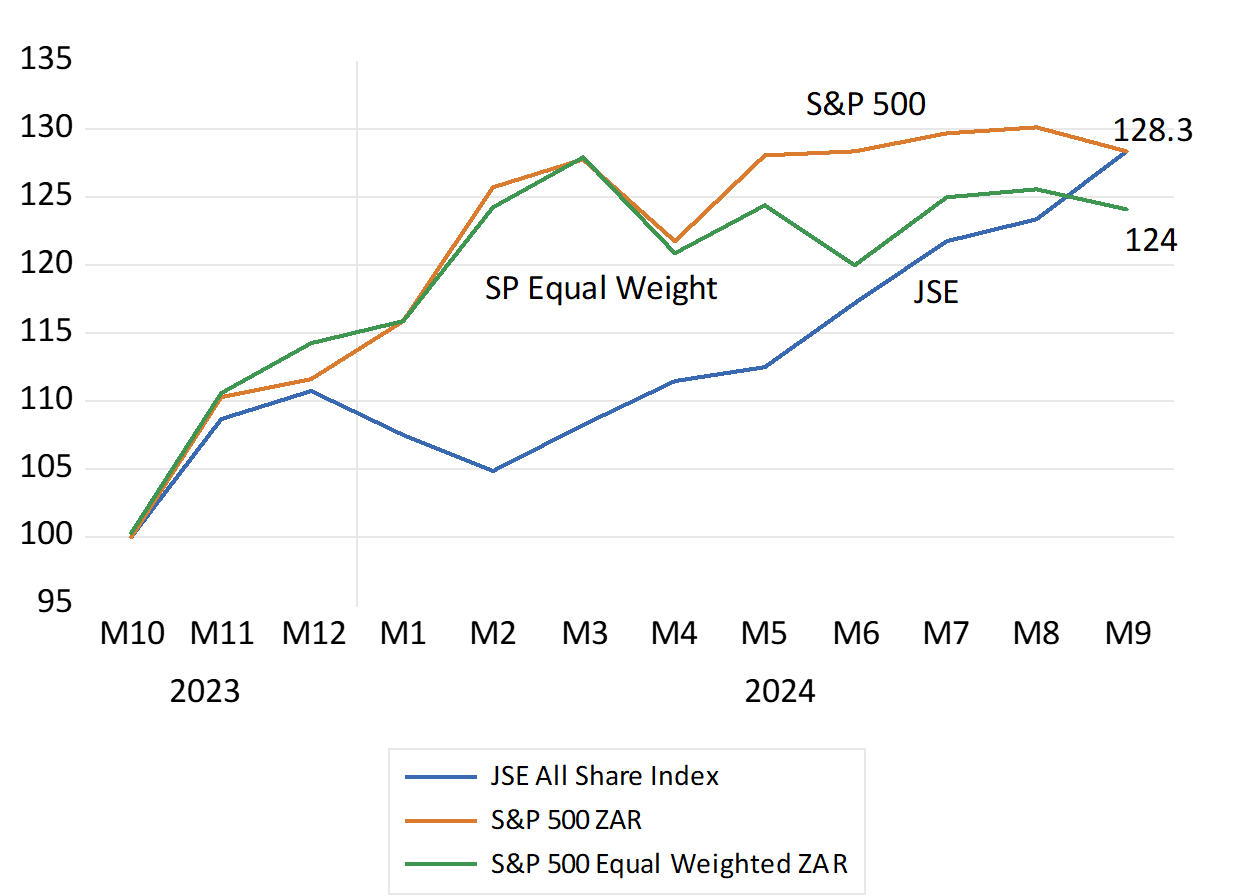

The S&P 500 Index, the equally weighted S&P Index and the JSE All Share Index. Total returns to October (2023=100) Rand Values

Source; Bloomberg and Investec Wealth and Investment.

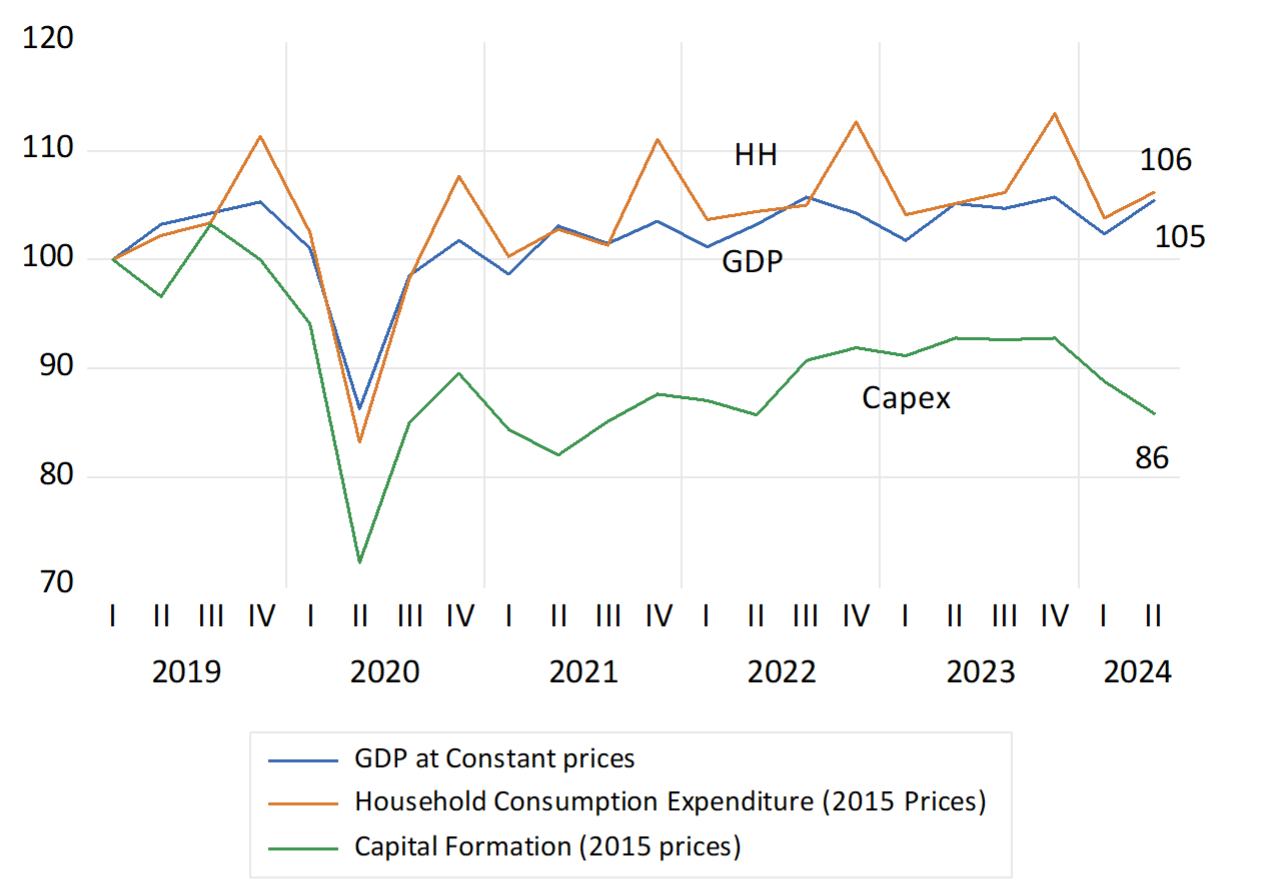

Looking back at the economy reminds how tough it has been in recent years for households and businesses dependent on the state of the SA economy. Since those pre-Covid days the economy has hardly grown at all. Compared to Q1 2019 GDP by June 2024 had gained a mere 5% over the five and a half years. (growth of less than 1% p.a) Households are spending but 6% more than they did then and capital formation is down by about 14% in real terms. How could such a deterioration be allowed to take place?

Vital SA Economic Statistics. Supply and Demand. (2019=100) Quarterly Data.

Source; SA Reserve Bank and Investec Wealth and Investment.

Clearly the supply side of the economy performed poorly – led by the well documented, confidence sapping failures of the State-owned enterprises and of government generally, including those of the provinces and municipalities. But demand management by the Reserve Bank can also be held responsible for at least some of the weakness. Much of the period since 2021 has been accompanied by much higher interest rates both absolutely and relatively to inflation. That is despite the grave weakness of demand for goods services and labour.

The Reserve Bank’s Monetary Policy Committee provides a full explanation on a regular basis for these interest rate settings. It has been fighting inflation and only inflation that rose after 2021 as the rand weakened so significantly after 2021. The idea of a dual mandate of the US Fed kind – low inflation and employment growth being the combined objective of monetary policy – has been anathema to our determined inflation fighters.

Shocks to the price level caused by exchange rate weakness – unrelated to immediate monetary policy settings and inflation trends – are clearly not ignored when interest rates are set. Yet such shocks- decidedly not of the Reserve Bank’s doing- lead inevitably to more inflation – then higher interest rates – and in turn still weaker demand – already under pressure from higher prices. Higher prices have their complex causes- but they also have (rationing effects) on the willingness to spend more- given minimal growth in income

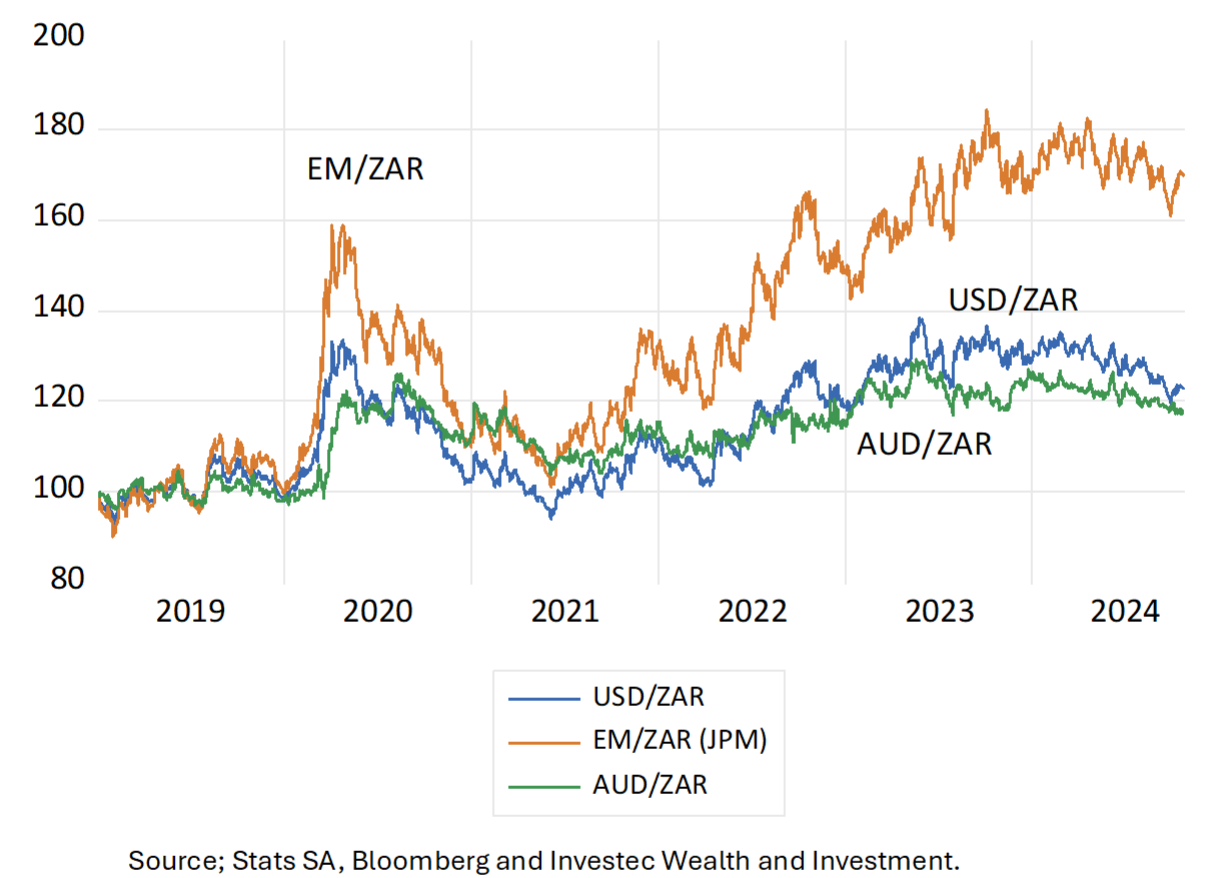

The problem for SA and the Reserve Bank was that the ZAR weakened decidedly after 2021- and weakened against not only the US dollar but also vs other EM and commodity currencies. It was SA specific in nature clearly linked to the failures of government and the failure of the economy to grow that added to SA specific risks. The USD/ZAR, as had the average EM/ZAR and AUD/ZAR had recovered well from the Covid linked risk aversion that brought pressure on the ZAR and the market in SA Bonds. SA appears particularly vulnerable to Global Risk aversion. It may be recalled that the USD/ZAR had recovered to as little as R14 in early 2021. But then the sense of South African failures to realise economic growth took over the currency and Bond markets . And the weaker rand inevitably forced prices higher at a faster rate. Given the MO of the Reserve Bank.

The ZAR Vs the USD, the EM Basket and the Aussie Dollar. Daily Data 2019-2024 (2019=100)

Source; Stats SA, Bloomberg and Investec Wealth and Investment.

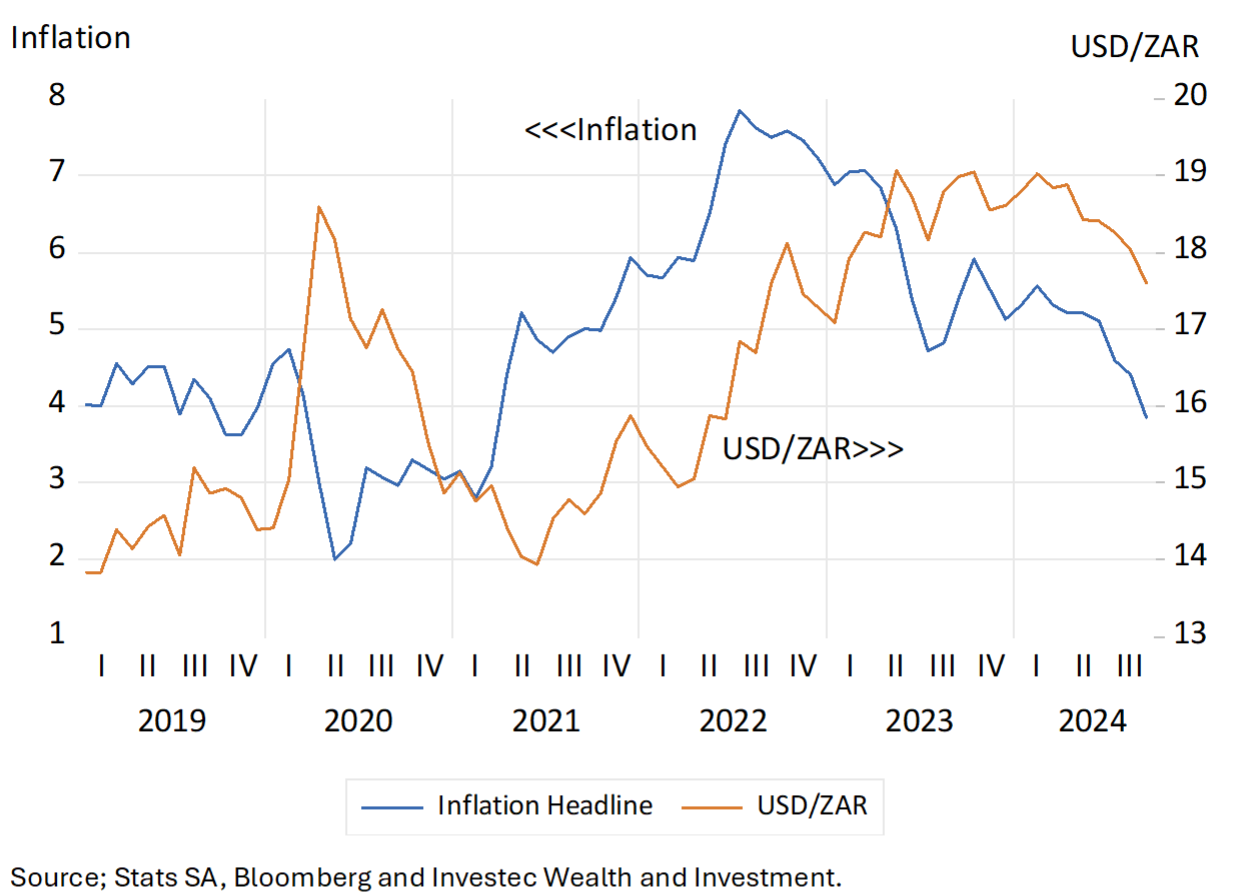

Interest rates and the USD/ZAR 2019-2024. Monthly Data to September 2024

Source; Stats SA, Bloomberg and Investec Wealth and Investment.

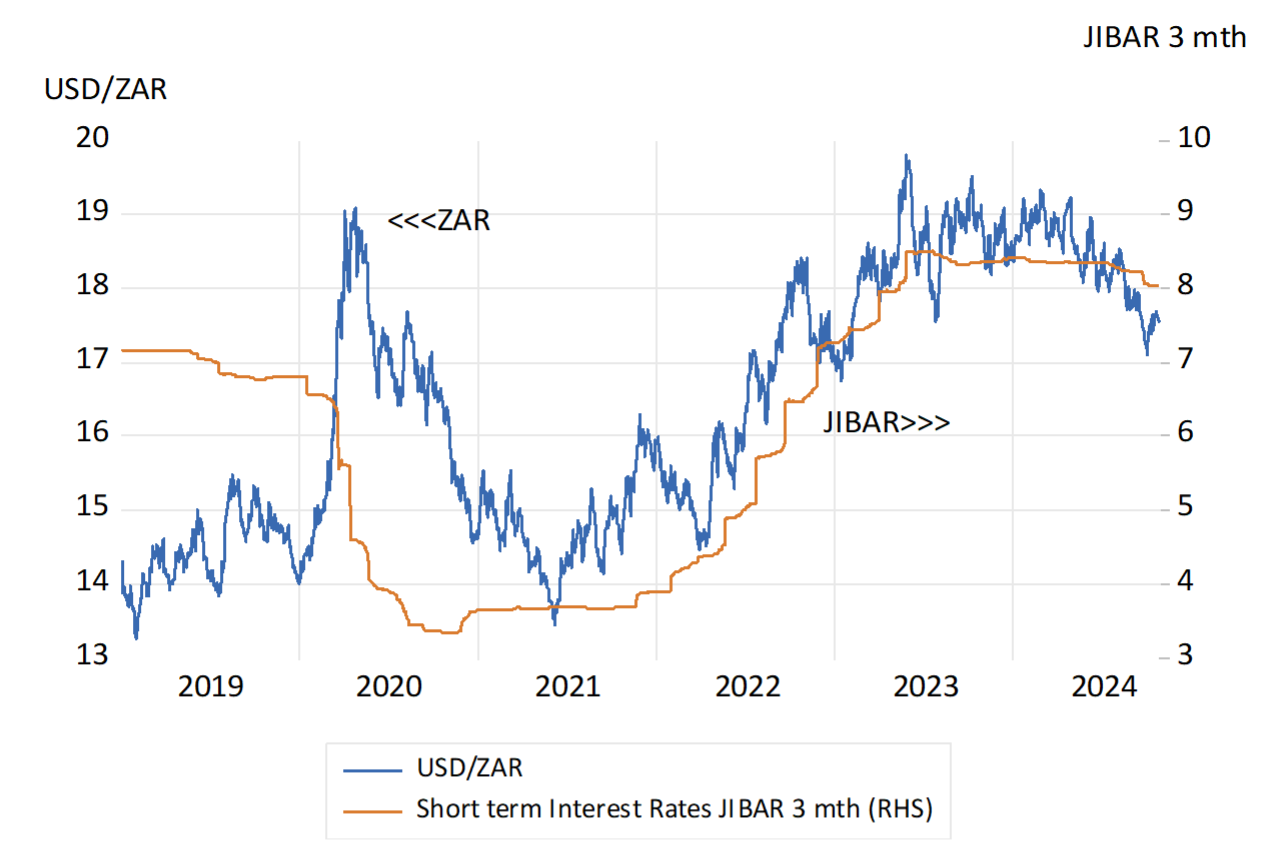

The ZAR and Short-term Interest Rates. Daily Data (2019-2024)

Source; Stats SA, Bloomberg and Investec Wealth and Investment.

The connection between the foreign and domestic exchange value of the ZAR and the outlook for the SA economy has never been clearer. The GNU has raised the prospects for growth and the ZAR and the bond and equity markets have responded accordingly. Inflation is therefore on the way down. Over the past three months it has averaged but 2.4% p.a. Interest rates at the short end of the market have come down and will come down further provided the ZAR holds up. Not so much vs the US dollar, that may be getting a Trump boost, but also against the other currencies similarly affected by the USD. We should not expect the Reserve Bank to change its pro-cyclical approach. We should but insist and hope that the supply side weaknesses of the SA economy are well addressed. Raising the GDP growth rates to a modest 3% p.a. will not only promote economic and political stability, it will bring lower interest rates and less inflation.

I like to visit the local supermarkets. And not only for the usual reasons. It helps confirm my faith in the power of market forces. Fully evident in the impressively wide range of goods and services on offer.

The SA retailers very adequately fulfil the all-important task that we have delegated to them. That is to deliver a wide range of goods, including food and medicine essential to life and happiness. The retailers are left mostly alone to manage a highly complex supply chain that involves, farms, ports, roads, trucks and ships, factories and warehouses, banks, landlords and regulators. And they manage the always complicated relations with workers and their supervisors to pack the shelves and fill the checkout counters and increasingly to deliver directly to homes.

They are serving us well for highly robust reasons. That is to make a living. Mostly modest but some very impressive. Generating incomes for the owners and staff that will bear a close relationship to the difference between the costs of providing the essential service and the revenues generated. To generate profits they will have to prevent the corruption of the supply chain.

Such profits will also depend on how well the retailer manages the promotion or demotion of managers and workers- including the succession plans for senior executives. The retailer as must any business manage successfully the relationship between the efforts of and rewards for the work force. Providing the right incentives to work harder or smarter remains highly relevant for containing costs, enhancing revenues, and the margins between them. Without which the firm would not survive the competition for the household budget.

The apparent “chasm” between the pay of the CEO and the average worker should be regarded as an important part of the market in action. To be admired rather than resented as representing the natural outcome of the supply and demand for very different capabilities and talents at work. As explaining the wide difference between what Taylor Swift and her hair stylist takes home after a show, given their very different contribution to the bottom line. Such inequalities of rewards are part of the necessary incentives for the best and brightest to ascend the highly competitive and greasy corporate poles to make a better fist of it. We can’t all hope to be as good as a Taylor Swift, or an exceptional CEO. Yet whose contribution to the bottom line will never be as obvious as that of a Prima Donna.

Moreover, the resulting flow of profits realised will largely be retained by the owners and invested in the firm to improve the offers to households. Profits are good for customers. But the profits they realise are not fully under the control of the retailer. They depend heavily on the purchasing power of their customers, their incomes, that in turn depend on how well the economy at large is being managed. The SA economy has acted as a serious headwind for the retailers and even more so for their local suppliers. A headwind revealed in the form of declining returns on capital employed, and in goods that move more slowly off the shelves for want of demand. And call for more working capital to back up delays in the ports and distribution centres and by load shedding. The result of which are poorer returns on all the extra capital employed and less invested in new plant and equipment and in the work force.

The failures of the SA economy have much to do with the unwillingness of the economic power brokers to follow the example of the retail sector. As in the persistent but unrealistic, given past performance, faith in a reformed SOE’s and government departments to raise their games. Rather than contracting out much more of production to the private sector- honestly selected and helpfully incentivised to deliver as are our retailers.

They refuse to do so for their selfish reasons, as well as misguided notions of how an economy works best. Yet they must know that the slow growth outcome is a consistent threat to their influence. “As hulle net geweet het wat ek geweet het…” (if only they knew what I know) learnt shopping with eyes and minds open to the evidence, SA would be, could still be, in a much happier state for retailers and their customers.

JSE listed companies have been beating down on themselves very heavily. Kabelu Khumalo reports some R250 billion of recent write offs and write downs of assets. (BD August 12th) It will mean that the book values recorded on the balance sheets perhaps will accord more closely with the market value of the company. Yet the cash flows of the business would be unaffected by the action and there are unlikely to be any taxes saved on the losses because they will not be recognised as a business expense. And the bottom line will be even less meaningful.

The prior damage done to cash flows and market value by poor investments or acquisitions will long have been recognised and deducted from the value of the company by investment analysts and the investors they advise. They will have made their own diminished sum of parts calculations of the present value of the divisions of any company. And they may still have a very different view of what the underlying assets might bring shareholders in the future.

Notice something important about these adjustments to the books designed to align book and market value. There is very unlikely to be an equivalent urgency to upvalue the assets on the balance sheets that have proved to be market value adding. The great new mine that has proven to be so valuable to shareholders is likely to remain on the books at something close to its historic costs. Not written up in the books to enhance earnings and equity capital employed and the strength of the balance sheet. And when an excellent acquisition was made paying above the book value of the company acquired, this goodwill is very likely to be amortised against earnings, so reducing book value and the capital employed by the business. Rather than logically seen as adding to the amount of valuable capital employed by the business.

The benefits of writing off capital employed in a business, rather than writing it up, will show up in an important measure, and that is as Return on Equity Capital employed (ROE) The less capital recognised the better the return on equity all other operating details remaining the same. And the managers of the business are very likely to be rewarded directly on the basis of ROE. Shareholders will benefit when the company they entrust their savings can deliver a return on the capital they employ that exceeds the opportunity cost of capital employed. That is the returns shareholders might expect investing in an alternative company with similar operating risks.

Making poor investment decisions reduces ROE. Recognising past failures will not change past performance. It might however indicate that milk has been spilled, that costs have been sunk, that bygones are bygones and most important that more good money is less likely to be thrown away on lost causes. And if the managers are surprisingly contrite might help add market value by improving expected performance.

But what could be more helpful to an incoming CEO, also to be measured on future ROE’s than to begin a reign with less capital? True kitchen sinking, recognising the mistakes made by predecessors, could be managers wealth enhancing, if future rewards are to be based on higher ROE’s, as indeed they should be.

If the actual capital entrusted to the incoming CEO and the team of operating managers is accurately measured, it is only then that improvements in ROE can be properly recognised and encouraged. And rewarded appropriately in all the operating divisions whose managers can be held responsible for the capital they are given to manage, again accurately estimated.

South African directors of companies now burdened with justifying not only what they pay their senior managers, but with also justifying the absolute difference between the rewards at the top and bottom of the pay scales, may point to the example of Starbucks. Changing their CEO yesterday immediately added over 20 billion dollars to the market value of Starbucks. Paying the right CEO enough, not too much, nor too little, rewards based predominantly on improvements in ROE, properly calibrated and communicated, should be the primary task of any Board of Directors. And when put into good practice with successful and well and competitively paid CEO’s, will deserve the approval of shareholders.

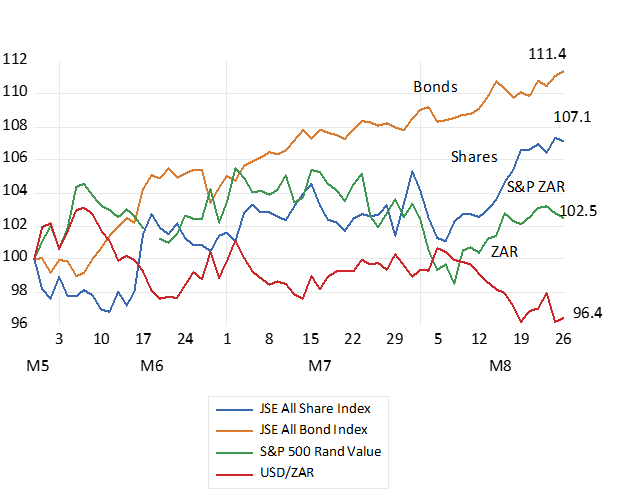

The financial markets have welcomed the Government of National Unity (GNU) The reactions in the bond market have been particularly favourable. The JSE All Bond Index on August 26th was up by 11.4% since the election of May 2029. The share market was up by 7.1% while the ZAR has gained 4% vs the US dollar and vs other EM currencies. Given the importance of equities and bonds held by SA households in unit trusts and pension plans (some 15.2 trillion rands worth at year end 2023) representing 85% of all the assets held by SA households) such market moves have already had a very significant impact on the wealth of South Africans.

The promise of faster growth has added close to 10% or over 5 trillion rands mutual funds to the SA household balance sheet. Extra real money indeed and helpful for stimulating additional household spending, of which SA has had too little of for many years now. [i]It is not only the supply side constraints that have held back the economy. Demands from households and the firms that serve them have been insufficient to drive growth above an immiserating 1% a year.

The importance of the judgments of the global capital market of SA economic policy for the average South African, their hopes for employment and a comfortable retirement, for which they sacrifice heavily, cannot be underestimated.

Post election movement in the Financial Markets. Daily Data – May 29th – August 26th 2024. May 29th=100

Source; Bloomberg, Investec Wealth & Investment.

The strength of the ZAR is particularly welcome. It brings with it lower inflation and lower short-term interest rates essential for a recovery in the economy. The positive link between the outlook for growth and the behaviour of the ZAR has again been emphasised, (more growth stronger rand and vice versa) as has the link between a stronger rand and inflation.

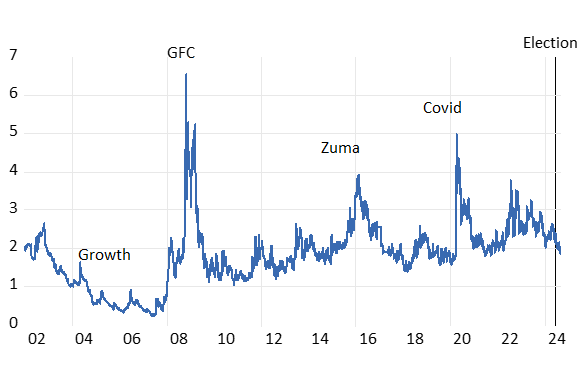

There is no room for complacency. The status of RSA debt has improved, but interest rates and the cost of capital remain elevated. Our credit rating remains significantly weaker than it was between 2002 and 2008 when our economy did grow at close to 5% p.a. (see below)

The RSA Credit Rating. The CDS spread between the yield on RSA 5 year USD Denominated Bonds and a 5 year US Treasury Bond

Source; Bloomberg, Investec Wealth & Investment.

There is much room to further impress investors. By taking economic policy decisions now, that by promising faster growth over the longer term, could immediately further strengthen the bond and currency market.

The National Health Initiative, now being actively promoted, does the opposite. It promises more of the same fundamental weaknesses that have infected all the State directed enterprises to date. The direction of health care reforms should also be one of seeking partnerships with the private sector- with private hospitals and practitioners. It calls for experimenting with the private control and management of hospital services. Hospitals currently funded by the State that perform so poorly on all metrics, including the costs of supplying inferior service.

A helpful positive note was offered by the Transnet CEO. Michelle Phillips who said yesterday that “…the entity’s move to maintain run and invest at Ngqura and the 670km container corridor would be reworked after potential bidders complained that the conditions attached to the tender were too stringent and costly for the private sector to fully participate..” (BD August 28 Thando Maeko)

The public sector in SA, in all its guises, needs to come to realistic terms with the potential providers of private capital and skills that are essential to our economic purpose. Their managers need to fully understand how to deal with potential private sector partners who operate globally. Such knowledge applies to plans for ports and railways and refineries, for the supply of water and the transmission of electricity. And for bringing minerals, oil and gas to the surface. And to recognise the terms and conditions, no more or less than internationally competitive terms, that would bring potentially abundant and truly economic game changing offshore gas, onshore. Offering credible deals of this kind would be enough to move the markets. And so immediately, with lower interest rates and a stronger rand and less inflation, would help realise the growth in incomes and employment necessary to re-elect a GNU in 2029.

[i] I am drawing on a recent comprehensive analysis of the SA balance sheets by J.Makoena and K Setshedi published in the SA Reserve Bank Quarterly Bulletin, June 2024. The study shows how very well developed are pension and retirement savings in SA (120% of GDP) are compared to other emerging economies. And so the importance of investor sentiment for SA wealth owners.

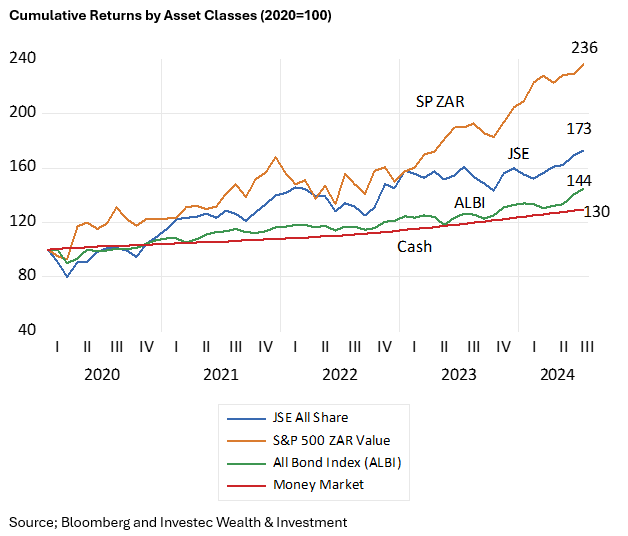

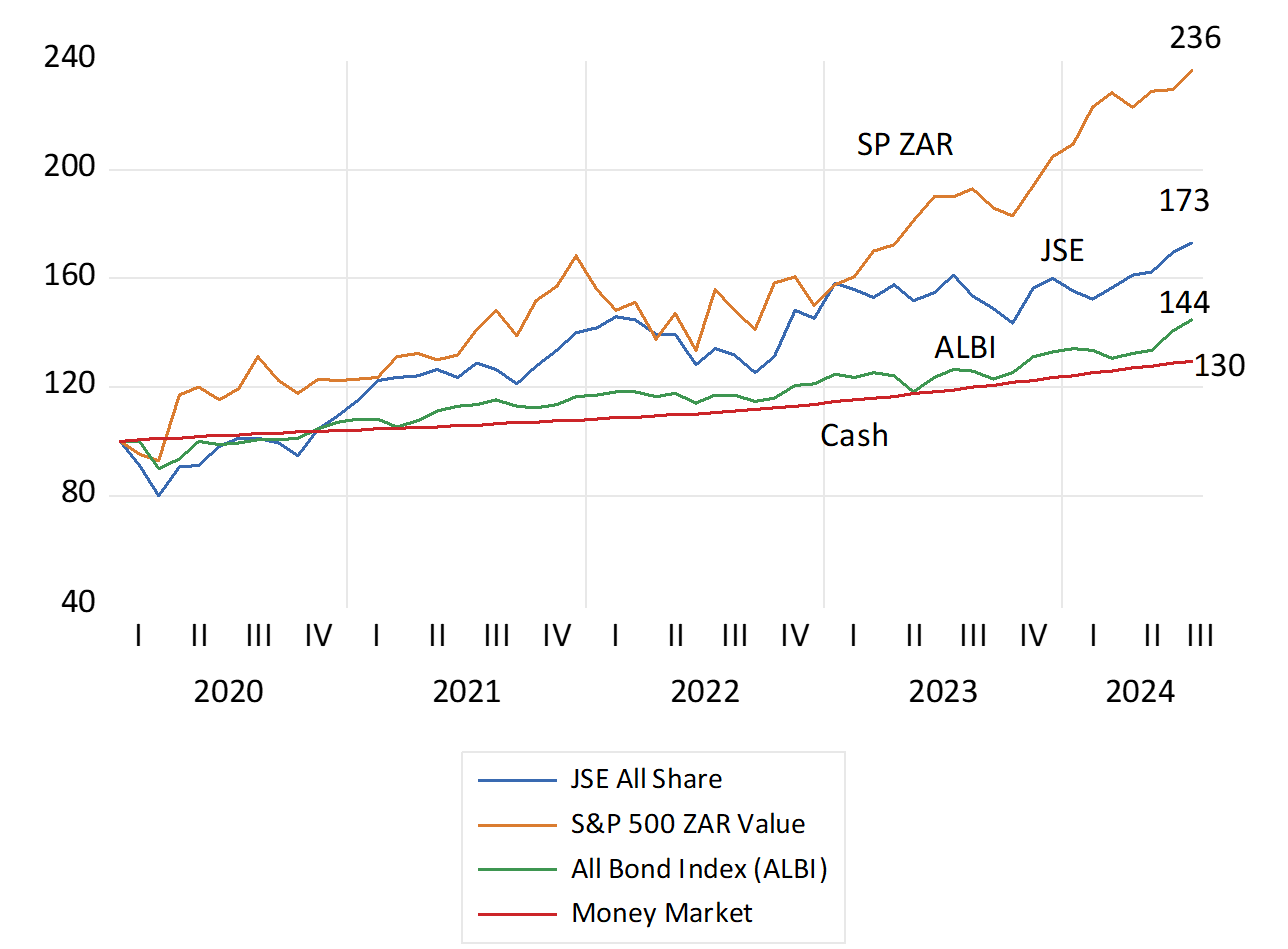

Dealing with Covid in 2020 was a frightening episode. The JSE All Share Index lost 20% of its value by March that year and the S&P 500, suffered a very similar drawdown, of 20% in USD. Yet something predictable then followed. Between January 2020 and July 2024 share markets have given very good returns and they have outperformed bonds and cash by large margins. R100 invested in the JSE immediately pre Covid with dividends reinvested, would now be worth R173. Had the R100 been invested in the S&P 500 it would now be worth significantly more R236. The same R100 if invested in the Bond Index or in a money market fund with interest reinvested would have grown to only R144 and R130 respectively.

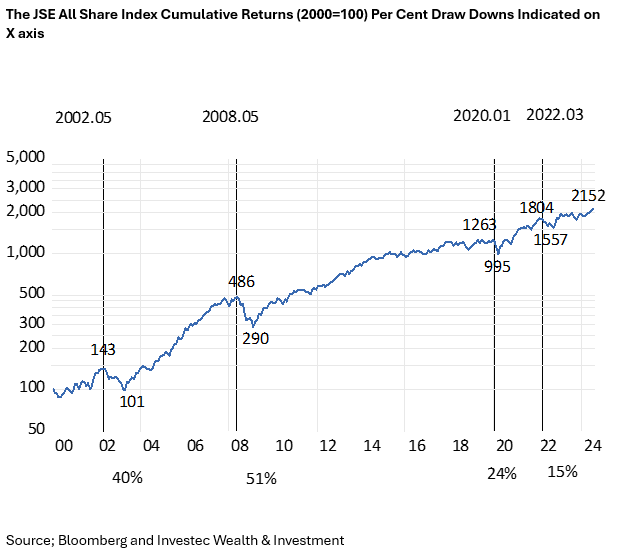

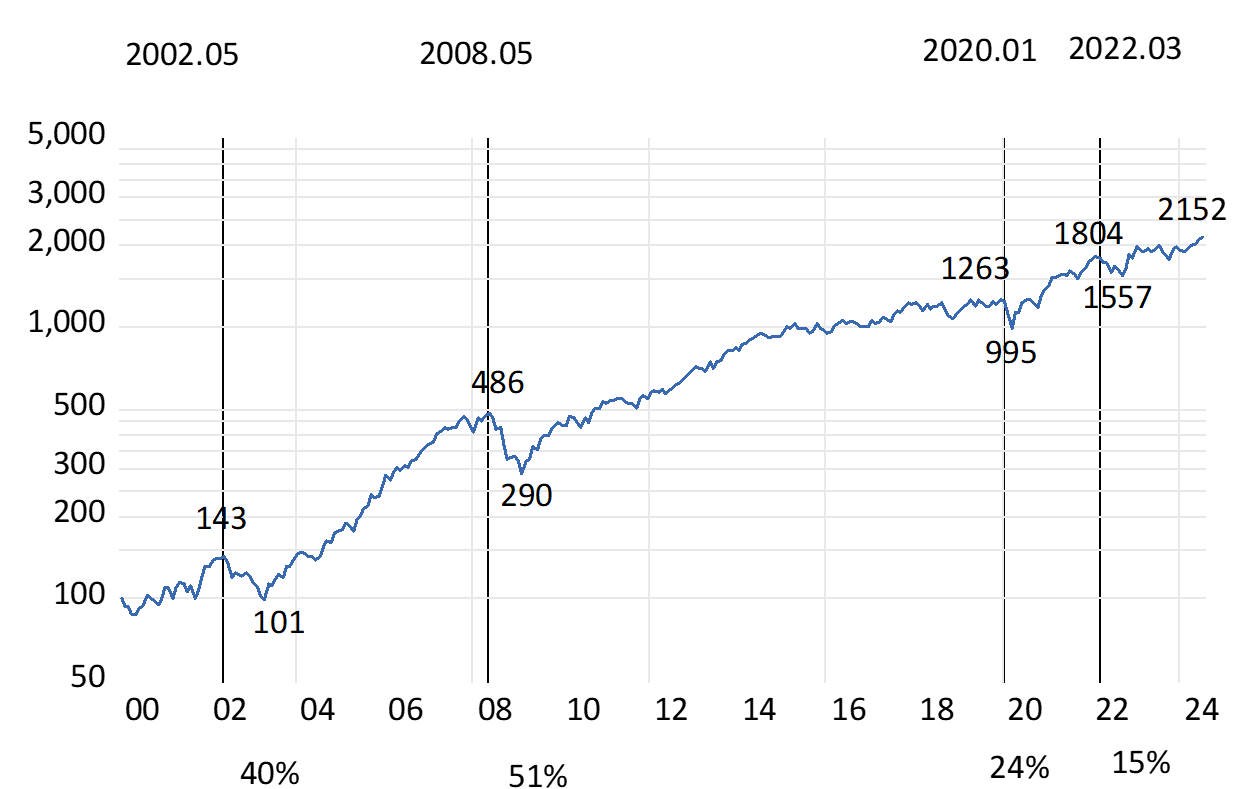

A predictable outcome–given the large outperformance by a representative share portfolio on the JSE since 2000, or for that matter also since 1980 or 1960. The R100 invested in the JSE Index in 2000 would have grown to R2152 that is by 21 times at an annual average rate of return of 13.12% p.a. The R100 in money market would have grown by 6.3 times and the Bond Index by 10.6 times over the same period. Incidentally the JSE has kept up with the S&P also measured in rands over these 24 years. The JSE outperformed significantly until 2010 and has underperformed since.

The JSE has therefore recovered very well from significant periodic drawdowns since 2000, 40% down in 2002, 51% in 2008, 24% after Covid and 15% with Fed tightening in 2022.

Equities are expected to give superior returns because they are more risky to hold than cash or bonds. The higher returns expected of equities compensate for the different risk of losses investors believe they are exposed to holding shares. Higher expected returns mean lower entry prices for investors, all else remaining the same. And these expected extra returns have been delivered to date by most Stock Exchanges.

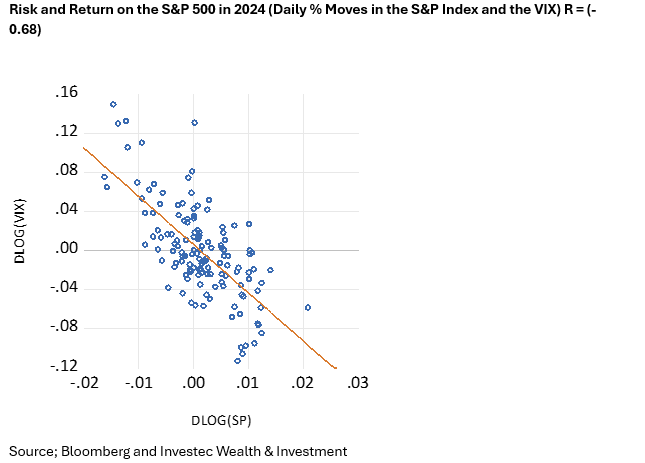

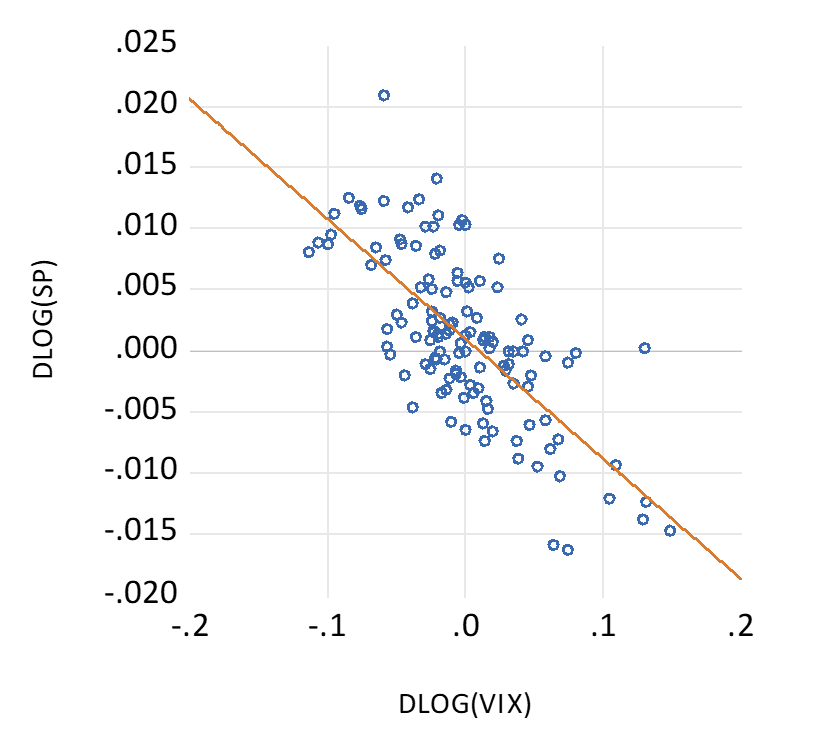

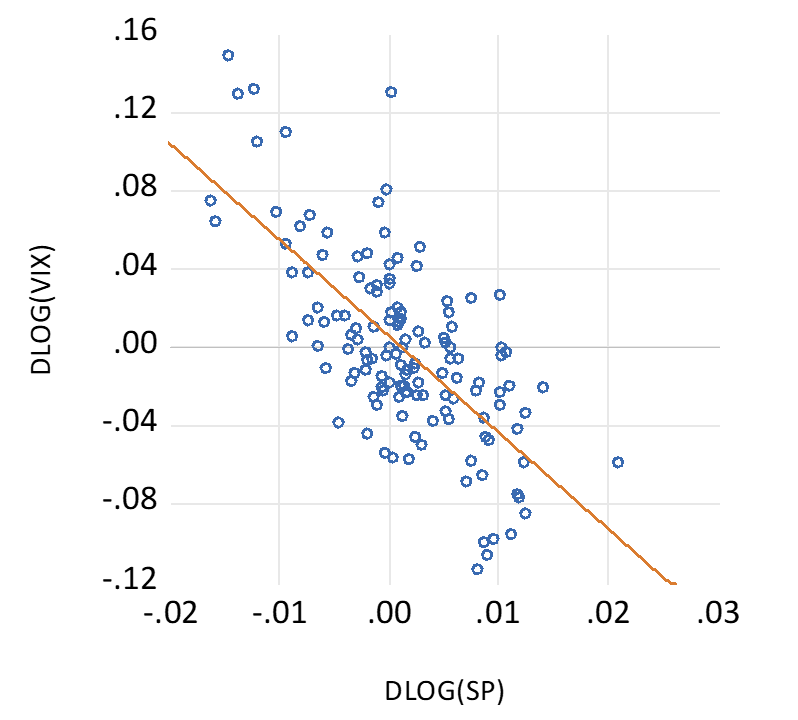

Share prices move each day about an average of close to zero. They demonstrate a random walk with hopefully upward drift to give the expected positive returns over the long run. The more difficulty investors have in interpreting the news about a company or an economy, the wider are the daily swings in prices in both directions. This volatility gives rise to an objective measure of risk. It will be reflected in the cost of an option to insure against volatility. Investors can buy or sell a volatility index, the VIX, based on the underlying volatility of the S&P 500. When S&P volatility (risk) rises share prices fall. And vice versa They do so to improve or reduce prospective returns, in a statistically significant way. As has again been the case this year.

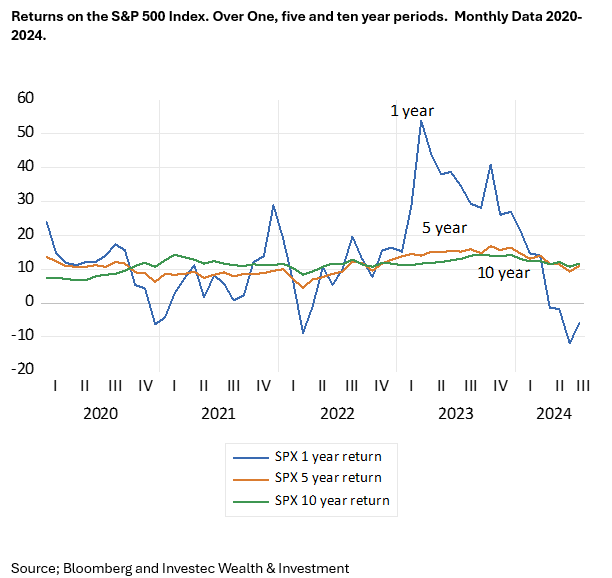

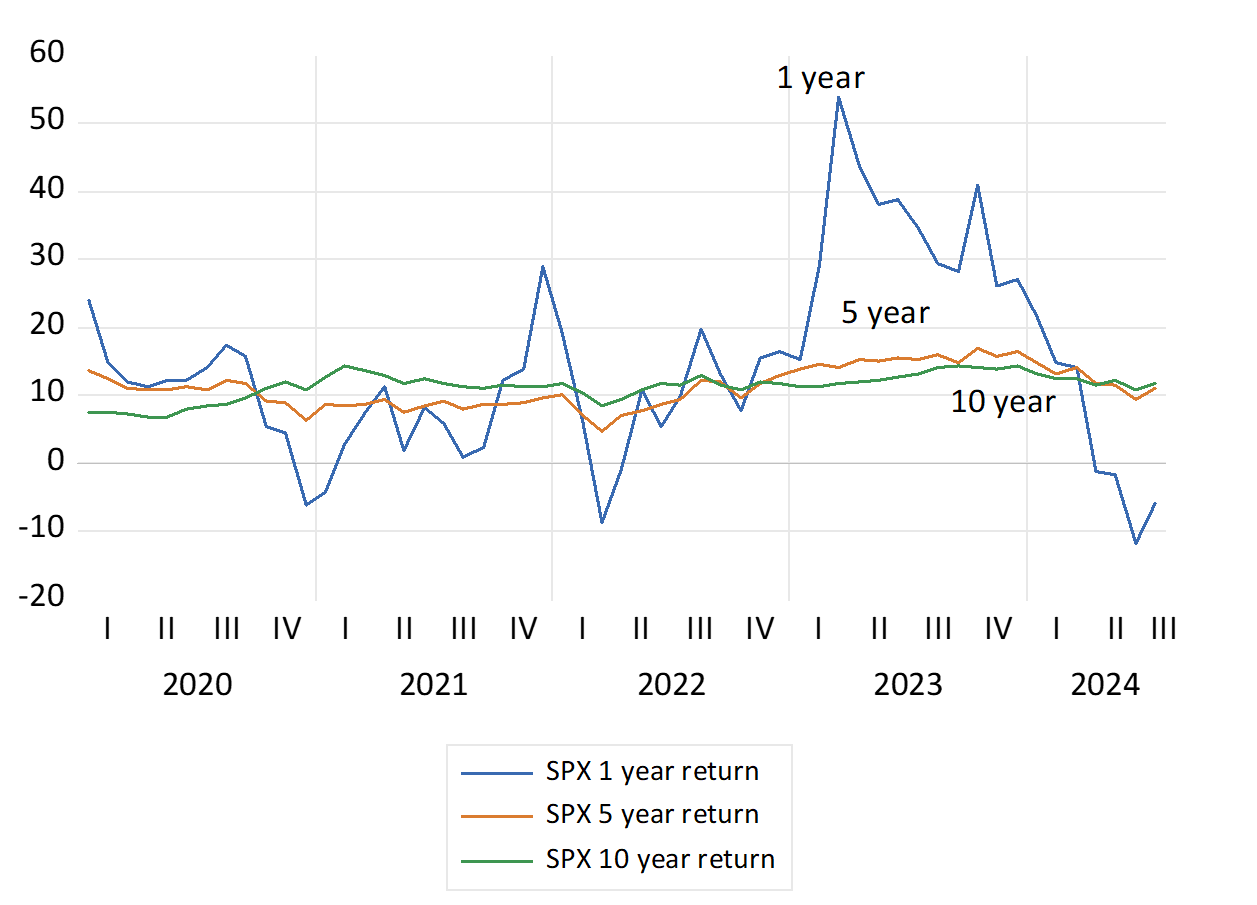

Yet were share market returns measured over longer periods, the risk of an in period loss falls significantly. The average returns when investing on the JSE or S&P market are very similar when returns are measured over one, five or ten year holding periods. Since 2020 returns for holding the S&P Index have averaged about 14% over one year and 11.1% p.a. and 11.2% p.a. when calculated over consecutive five year and ten-year periods respectiverly. However, the Standard Deviation (SD) of returns about the average has been much higher for one-year returns (13.87) than for five or ten year returns with SD’s of 2.93 and 1.96. The same relationship holds when the analysis is taken back to 2000. Risks (the SD or volatility of returns) have fallen sharply when the investment period is extended beyond one year. Absolute losses when returns are measured over five- or ten-year periods occur rarely. It took a Financial Crisis to do so.

The extra expected returns for extra equity risk applies to the averagely risk-averse investor with limited wealth. When you are investing for you children and grandchildren and their children, and are wealthy enough not to have to worry about being forced to cash in your shares, you can invest without much risk -and you can expect to pick up the money left on the table by the more risk averse. Further support for time in the market – not timing the market.

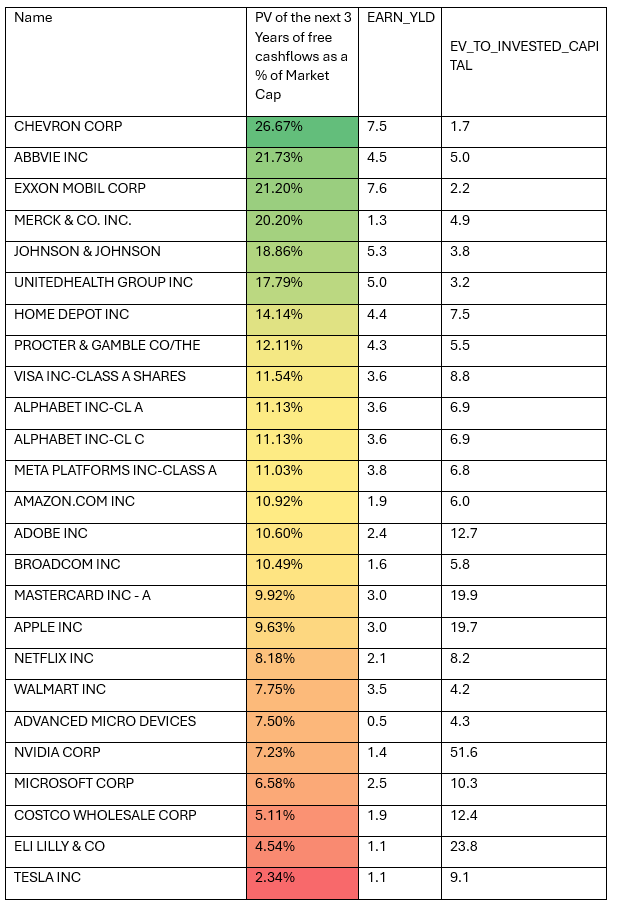

Much of the value of any company can be attributed to profits expected over the long run. If we discount the next three years of Microsoft’s (MSF) free cash flow- cash flow after capex- (FCF) as estimated by Bloomberg- discounted at 8% p.a. – we can explain only 6.6% of its current value. Nvidia has 7.2% of its present value explained this way. The 97% dependence of Tesla on growth beyond the next three years is greater still. By contrast 27% of oil producer Chevron and 22% of Exxon Mobile can be explained by the immediate short-term outlook. They are clearly value stocks.

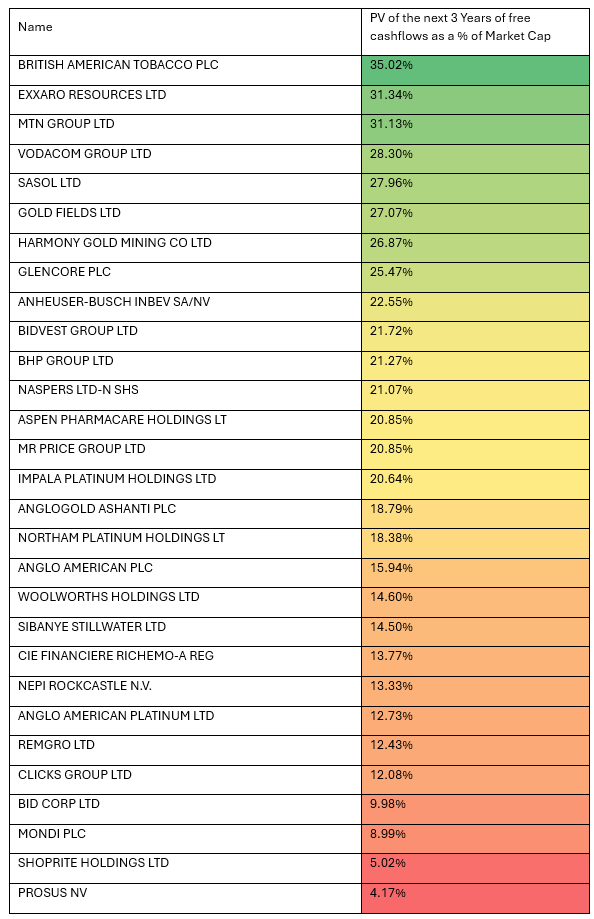

Most of the Top 40 stocks listed on the JSE, fall into the value category. A relatively high 32% of MTN and 28% of Vodacom, depend on the next three years of FCF – discounted at a much higher 14% p.a. While about 21 per cent of Mr Price and Bidvest can be explained this way. Anglo at 16.13% is therefore expected to deliver on its restructuring plans.

Table; Share of Market Value (July 2024) explained by Present Value of next 3 years of Free Cash Flow (FCF)

US Companies – FCF discounted at 8%

JSE Listed Companies. Discounted at 14%

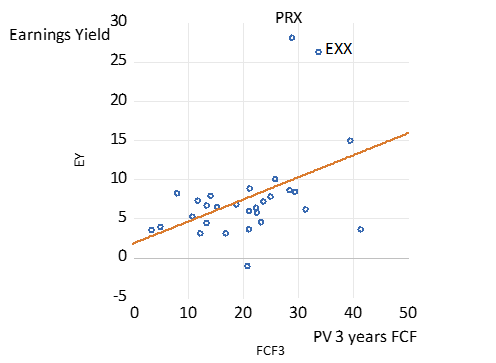

A scatter plot for the JSE Table. Earnings Yield and PV of FCF. Sample 29 companies in Table.

But as may be seen there are notable exceptions on the JSE that are priced for growth. The value of Clicks registers a mere 12% dependence on the next three years of performance while Shoprite with a 5% ratio, is even more of a growth stock by this measure. There is a strong link on the JSE between the PV of the FCF over the next three years and the initial earnings yield- the reciprocal of the P/E ratio as shown in the scatter plot.

Note, a 100 dollars or rands expected in 20 years’ time is worth 21.5 today at a discount rate of 8%. And worth only a third as much (7.28) if we raise the discount rate to 14%. The way to raise the value of SA economy facing companies is to lower the discount rate. As would follow faster economic growth. With a stronger economy the numerator of the SA Present Value calculation- operating profits – would rise and the denominator, the discount rate would fall, to provide a double whammy for present values.

Clearly the share market takes a long-term view. The observed day to day volatility of share prices is explained by the difficulty of forecasting profits or earnings or cash flows over the long run. And the longer the run, the more dependence of present value on future growth, the more that can go wrong or right for shareholders.

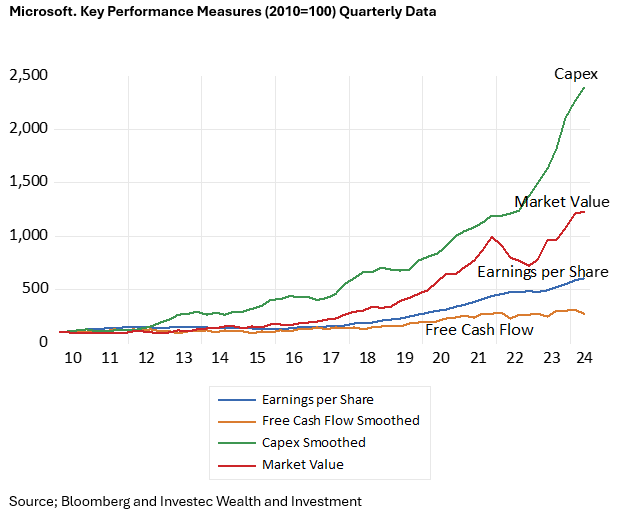

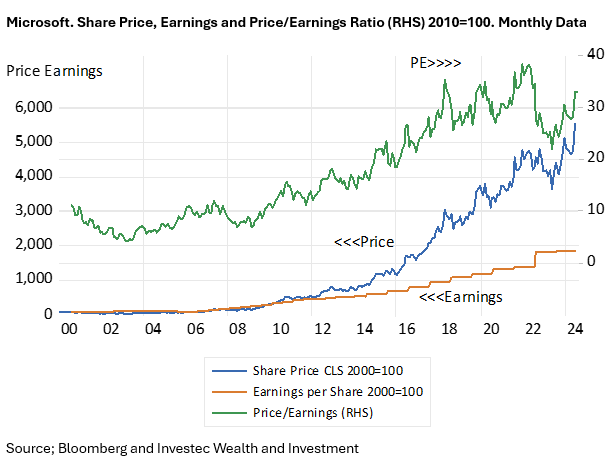

There is always the danger that investors will overestimate the growth potential of a growth company and the disappointment will reveal itself in much lower valuations. But even a very expensive growth company, by the usual metrics, can prove to be a great buy. Take the extraordinary case of MSF itself. It is a hugely successful company that transformed itself after 2010. And was rerated accordingly. In January 2010 MSF was worth $247 billion with a price to earnings ration of 11. By early 2019 the value of MSF had grown to over $800 billion and was then valued expensively and demandingly of growth at 26 times current earnings. The company is now worth over $3.3 trillion, an increase of 142% or by an average 25% p.a. since 2019.

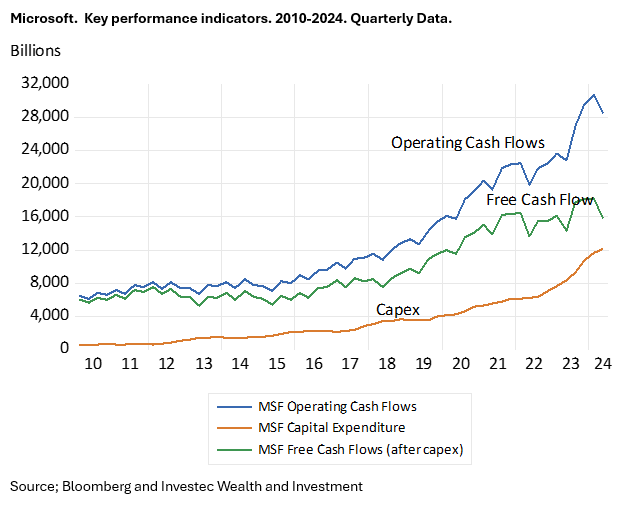

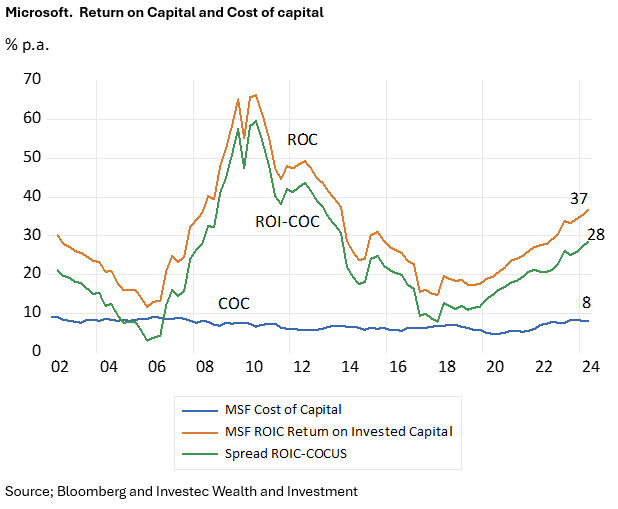

And MSF is now trading at about 38 times earnings after it reported yesterday 30th July. Is it still a buy? The answer will depend on just how well its extraordinary growth in Capex continues to transform into profits – by filling the cloud with data centres powered by microchips and by charging for generative IT. How well will this extra capex be monetised is the essential question? MSF Capex is now 25 times higher than it was in 2010. MSF Capex increased from $8943b to 13873b or 43%, this quarter compared to a year ago. While net cash from operations was up impressively by 29%. And accompanied by a large value adding margin between the return on Capital Invested by MSF – now 28% p.a. The largely unchanged MSF share price (down today by about 1%) indicates that MSF has satisfied very demanding expectations. The expectations of fast and profitable growth remain as they were. The same question is being asked of all the IT companies and not only the Magnificent Seven [1] that are adding aggressively to their plant and equipment.

[1] The original cast of the 1960 production of the Magnificent Seven included Yul Brynner Eli Wallach Steve McQueen Charles Bronson Robert Vaughn Horst Buchholz James Coburn

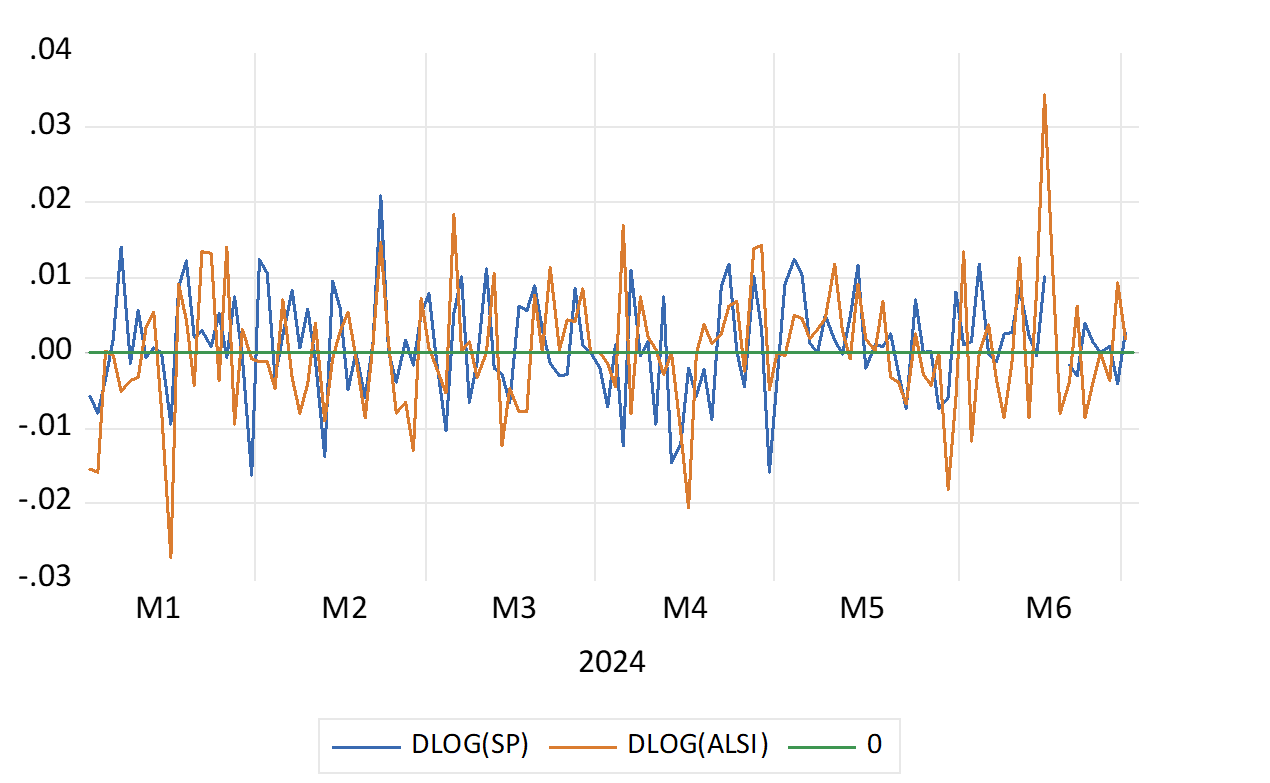

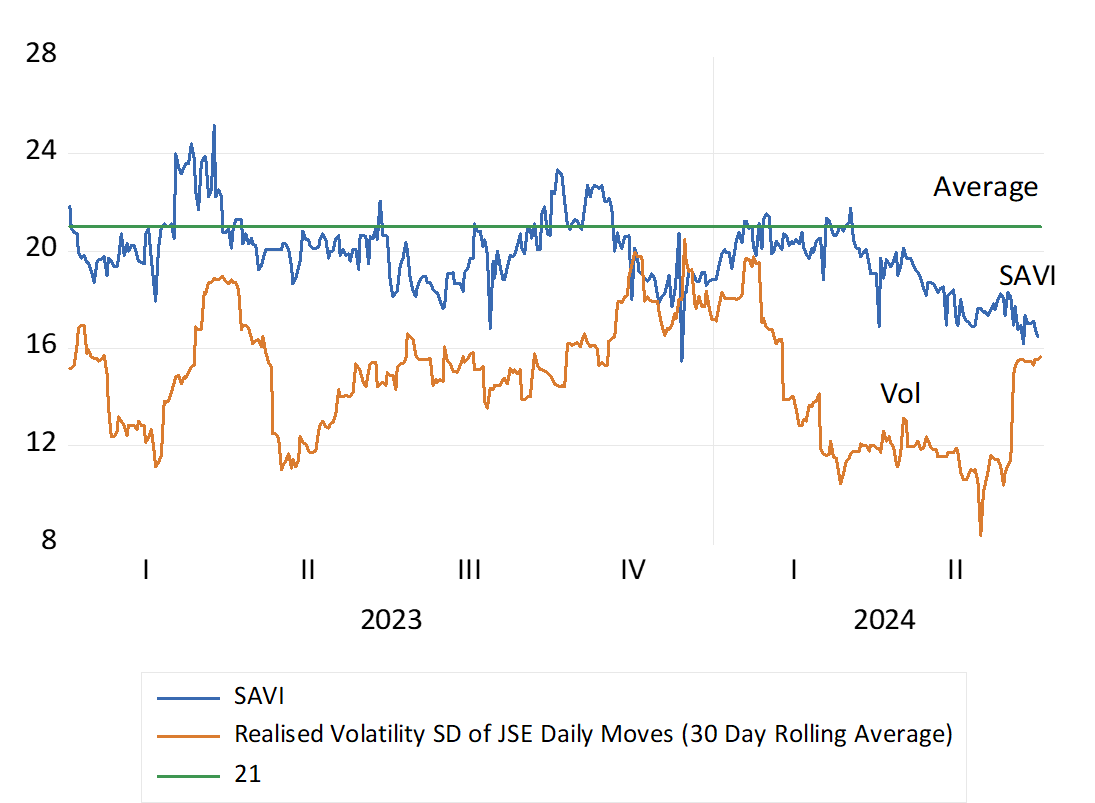

You might have expected more volatile markets, in this election year. The evidence however suggests otherwise. Investors on the JSE and the New York Stock Exchanges have coped comfortably well with the potential dangers. Daily volatility on both share markets, the scale of daily ups and downs in average share prices, has been unusually subdued, and well below long term averages in the US. Electing a scoundrel or a cognitively challenged US President has not made much of a difference to stability in the US markets The coalition outcome in SA proved welcome but not much of a surprise, again as judged by volatility trends. The Volatility Index for the S&P 500 – the VIX- also known as the Fear Index- has averaged 13 this year well below a daily long-term average 2000-2024 of 19. The equivalent construct for the JSE, the SA Volatility Index (SAVI) – with a similar long-term average of 21, has also trended lower this year.

As may be easily observed the chances of an Index or any well traded share moving higher or lower on any day are about the same. The pattern is thus of a random walk, of ups being matched by downs of roughly the same average magnitude. Yet happily for shareholders these movements have come with a slight upward bias, above a daily average of zero, to provide shareholders with positive returns over the longer run. If they stayed invested in the share market the end result has been strongly positive annual returns over five or ten year periods rolled back each month.

(See below the daily moves of the S&P 500 and the JSE All Share Index in 2024. We also show the Daily SAVI in 2023-24 as well as actual volatility of the JSE – calculated as the rolling 30 day Standard Deviation about the Daily Average Share Pirce Move)

Daily % Share Index Movements on the JSE and the S&P 500 in 2024

Source; Bloomberg and Investec Wealth & Investment

Daily Moves in the SA Volatility Index (SAVI) and Volatility Measured as the Standard Deviation of the JSE (Annualised as a rolling 30-day average)

Source; Bloomberg and Investec Wealth & Investment

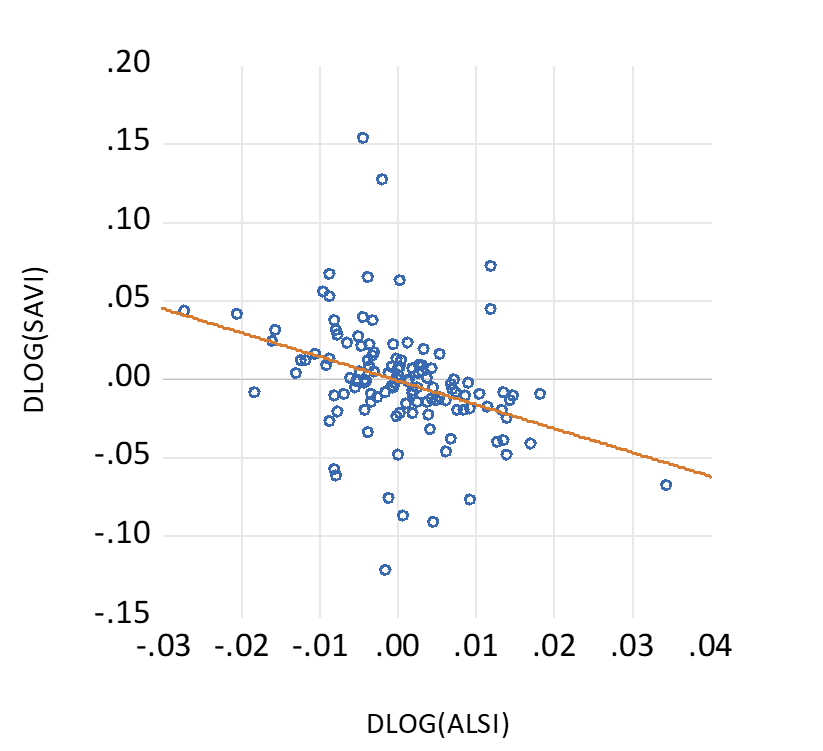

When daily volatility is more elevated, share prices will change consistently in the opposite direction. When the VIX or SAVI goes up share prices go down most days. They do so to improve the chances of higher risk adjusted returns- off a lower entry price- to compensate for more risk incurred. And vice versa. In 2024 it has been vice versa in the US and in SA- risks have fallen and values have improved. Extra risk comes with more returns and vice versa as nature intends. (see below)

The average move for the JSE in 2024 in the six months to June 2024 was an encouraging 0.27% per day. The S&P did only half as well- providing an average gain of 0.11% per day.

Daily % Changes in the VIX and the S&P 500 in 2024. Scatter Plot

Source; Bloomberg and Investec Wealth & Investment

Daily % Changes in the SAVI and the JSE in 2024. Scatter Plot

Source; Bloomberg and Investec Wealth & Investment

It is the quality of economic policy, more than the presumed certainty of such policies, good bad or somewhere in between, that will matter much more for financial markets in the long run. Any willingness of investors to accord a SA facing business an extended economic life will also add to present values. Provided the Return on Equity (ROE) exceeds the opportunity cost of capital, faster expected growth for a longer term, can explode the current present value of a share and market multiples. Price over Current Earnings or Cash flows and Market to Book ratios.

An accompaniment of lower ROE’s and a lower discount rate attached to future surpluses would also add much additional market value to SA companies. And to their willingness and ability to undertake and fund growth enhancing capex and employment. Faster growth if realised will add to an extra flow of cash to the government, bringing less risk to the fiscal outlook. And be reflected in lower interest and discount rates across the board and in higher share prices.

Extra wealth created in the bond and equity markets, is a game played by all with formal employment and retirement plans, and not only the richer few. The capital markets will provide an objective measure of the performance of the government of national unity (GNU) The score will be continuously kept and updated. While investors have not been frightened by the GNU, they have still to give approval. Over to the GNU.

Dealing with Covid in 2020 was a frightening episode. The JSE All Share Index lost 20% of its value by March that year and the S&P 500, suffered a very similar drawdown, of 20% in USD. Yet something predictable then followed. Between January 2020 and July 2024 share markets have given very good returns and they have outperformed bonds and cash by large margins. R100 invested in the JSE immediately pre Covid with dividends reinvested, would now be worth R173. Had the R100 been invested in the S&P 500 it would now be worth significantly more R236. The same R100 if invested in the Bond Index or in a money market fund with interest reinvested would have grown to only R144 and R130 respectively.

Cumulative Returns by Asset Classes (2020=100)

Source; Bloomberg and Investec Wealth & Investment

A predictable outcome–given the large outperformance by a representative share portfolio on the JSE since 2000, or for that matter also since 1980 or 1960. The R100 invested in the JSE Index in 2000 would have grown to R2152 that is by 21 times at an annual average rate of return of 13.12% p.a. The R100 in money market would have grown by 6.3 times and the Bond Index by 10.6 times over the same period. Incidentally the JSE has kept up with the S&P also measured in rands over these 24 years. The JSE outperformed significantly until 2010 and has underperformed since.

The JSE has therefore recovered very well from significant periodic drawdowns since 2000, 40% down in 2002, 51% in 2008, 24% after Covid and 15% with Fed tightening in 2022.

The JSE All Share Index Cumulative Returns (2000=100) Per Cent Draw Downs Indicated on X axis

Source; Bloomberg and Investec Wealth & Investment

Equities are expected to give superior returns because they are more risky to hold than cash or bonds. The higher returns expected of equities compensate for the different risk of losses investors believe they are exposed to holding shares. Higher expected returns mean lower entry prices for investors, all else remaining the same. And these expected extra returns have been delivered to date by most Stock Exchanges.

Share prices move each day about an average of close to zero. They demonstrate a random walk with hopefully upward drift to give the expected positive returns over the long run. The more difficulty investors have in interpreting the news about a company or an economy, the wider are the daily swings in prices in both directions. This volatility gives rise to an objective measure of risk. It will be reflected in the cost of an option to insure against volatility. Investors can buy or sell a volatility index, the VIX, based on the underlying volatility of the S&P 500. When S&P volatility (risk) rises share prices fall. And vice versa They do so to improve or reduce prospective returns, in a statistically significant way. As has again been the case this year.

Risk and Return on the S&P 500 in 2024 (Daily % Moves in the S&P Index and the VIX) R = (-0.68)

Source; Bloomberg and Investec Wealth & Investment

Yet were share market returns measured over longer periods, the risk of an in period loss falls significantly. The average returns when investing on the JSE or S&P market are very similar when returns are measured over one, five or ten year holding periods. Since 2020 returns for holding the S&P Index have averaged about 14% over one year and 11.1% p.a. and 11.2% p.a. when calculated over consecutive five year and ten-year periods respectiverly. However, the Standard Deviation (SD) of returns about the average has been much higher for one-year returns (13.87) than for five or ten year returns with SD’s of 2.93 and 1.96. The same relationship holds when the analysis is taken back to 2000. Risks (the SD or volatility of returns) have fallen sharply when the investment period is extended beyond one year. Absolute losses when returns are measured over five- or ten-year periods occur rarely. It took a Financial Crisis to do so.

The extra expected returns for extra equity risk applies to the averagely risk-averse investor with limited wealth. When you are investing for you children and grandchildren and their children, and are wealthy enough not to have to worry about being forced to cash in your shares, you can invest without much risk -and you can expect to pick up the money left on the table by the more risk averse. Further support for time in the market – not timing the market.

Returns on the S&P 500 Index. Over One, five and ten year periods. Monthly Data 2020- 2024.

Source; Bloomberg and Investec Wealth & Investment

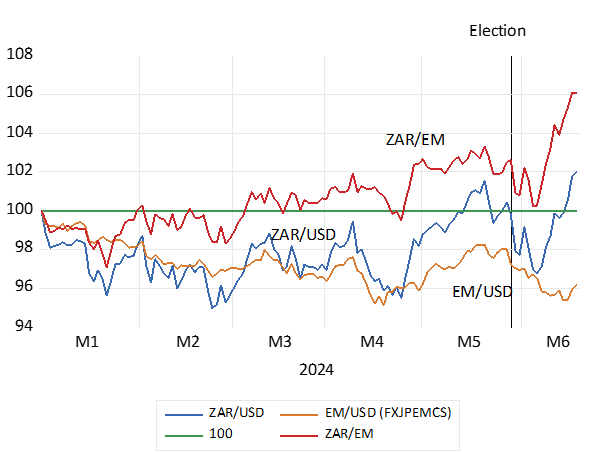

That the Government of National Unity would include the Liberal DA and exclude the EFF (extreme left or is it extreme right?) has been well received by investors. That this would be the new shape of government in SA was only known late on Friday 14th June after the markets were closed and that were only to reopen on Tuesday 17th June. The run up to the election had seen SA listed shares and bonds and the ZAR well up from their mid-April lows. On the presumption that the ANC would be able to do business as usual with the assistance, if necessary, of one or two minor parties. A sense of better the devil you know seemed to characterise market sentiment. That the ANC collected a surprisingly low 40% share of the votes cast, rather than 45-47 per cent expected, raised more uncertainty about the future course of economic policy. The markets in SA assets reacted typically to the new dangers by falling back from pre-election valuations.

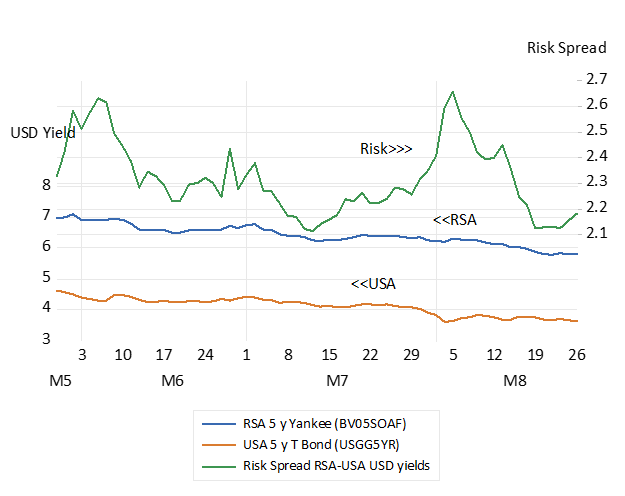

Early days surely yet the share and bond markets are now ahead of their immediate pre-election highs and have both gained about 7% in USD’s from the post-election aftermath. The ZAR has gained ground against the stronger USD and against the other EM currencies, the true measure of rand strength for South African, rather than US reasons. Of further encouragement is that the risks foreign investors attach to their SA assets have also narrowed. These sovereign or country risks are best measured by the spread between the yields on a RSA dollar denominated bond and those offered by a US Treasury Bond of the same duration. The spread between a five-year RSA Yankee bond had narrowed to 2.3% p.a. from 2.7% in the run up to the election. Then post-election the risk spread had widened to 2.6% p.a. and is now helpfully lower at about 2.2%. A good first impression but much more is called for the move the markets higher (see the charts below)

South African Stocks and Bonds in 2024. Daily Data to June 18th (January 2024=100)

Source; Bloomberg. Investec Wealth&Investment

The ZAR in 2024. Daily Data to June 18th January =100

Source; Bloomberg. Investec Wealth &Investment

Interest Rates – Dollar denominated Five Year RSA’s (Yankees) and US Treasury Bonds and the Risk Spread. Daily Data; April to June 18th 2024.

Source; Bloomberg. Investec Wealth &Investment

The DA will now carry a heavy responsibility for realising faster growth. Will the party and its leaders and followers be up to the task? Will they be able to manage change in an environment where the support of senior officials may not be fit for purpose? And when time spent in parliamentary debate and on the hustings may not have been the best possible preparation for expertly and vigorously executing the tasks at hand?

What specific government departments will be allocated to the DA members of the cabinet remains to be revealed. The DA should not be at all shy in coming forward to serve and be accorded a heavy responsibility for executing economic policy. There is apparently agreement on the initial economic policy reforms to be pursued, not surprisingly, given the weaknesses of government departments obvious to those who have sat for so long on the opposition benches and in parliamentary committees.

The Treasury and its Budget is in safe hands and can be supported by the DA in cabinet. It is the other economically vital Ministries that offer great scope for much improved governance and in executing policy and delivering value for the sacrifices taxpayers make to fund their government. The management role to be played by the Ministers to be held responsible for Mining, Industry, Energy, Transport Water and Municipal Services, in and out of Parliament, will be all important promoting economic development. That is the essential growth stuff to truly add value to SA capital from which all South Africans will benefit, those in and out of work.

Will the new appointments be up to the task? Businesses in South Africa can surely be a source of managerial talent. And a source of technical and financial advice to help fashion public-private partnerships to attract the necessary and available capital to revive the infrastructure. The best and brightest will be needed and will not be found wanting. A government that regards SA business as a partner in progress rather than a threat to its power and privileges will be a huge asset value and growth promoter.

How much better would the governing ANC have been received by the voters everywhere had they been supported by a rising tide of incomes and jobs, painfully absent since 2019? Including a scarcity of good jobs in the public sector (teachers, nurses, doctors) that have proved unaffordable, absent the growth in government revenues that comes painlessly with growth?

Yet even impressive and necessary fiscal austerity has not soothed the investors in SA government debt that have to cover our lack of tax revenue. They continue to demand high nominal and after inflation returns funding the RSA for fear that slow growth in the economy and in tax revenues makes printing money and more inflation much more likely sometime in the future.

And households have had to ante up the extra taxes needed to pay the extra interest on their national and on more costly personal debt. And to support a growing dependence on poverty relief provided to half of all SA households. Leaving less spending power available to households to encourage businesses to supply them with more of goods and services they much desire. And businesses, largely bereft of growing markets, have hired fewer workers and added to their growth enhancing plant and equipment, at a slower pace. High interest rates have meant high costs of funding businesses- that further discourage the essential work providers.

Welfare rather than work has been the SA poverty relief programme – and unintendedly but inevitably -discouraged the supply of labour. With regulated minimum wages adding further dis-incentives to the demand for and supply of labour. A potentially very valuable economic resource thus goes wasted and potential workers become highly frustrated. 11 million South Africans are formally employed outside of agriculture, out of an adult population of 40 million. Many middle income participants in formal employment with access to excellent privately supplied medical benefits, apparently were put off by the promise of equally good health care, provided publicly. Their trust in effective government delivery has understandably been lost and will not be easily regained. A fact of SA political life that any political party, that depends existentially on support from the centre, should recognise.

Slow growth has its own vicious spiral downwards and faster growth lifts all boats including those piloted by government agencies. And any governing party chastened by their electorate would surely look to the economy to improve their own re-election prospects next time, as well as the prospects of the citizenry. They would put both Party and SA in joint first place encouraging a stronger economy. The ANC government, recently, especially it’s Treasury, has not wanted for plans for reform. Private-public partnerships to invigorate the failing infrastructure feature prominently and are welcome. And its Budget deserves support from the economically literate. Being allowed to proceed on its announced path, with the hope they could do much better in executing its plans, would clearly be a relief to SA business and its funders. The largely stable stock, bond and currency markets suggest that it will be so allowed.

The essentially market friendly DA party and its fellow travellers, with about 120 of the 400 MP’s under its wing, would offer the much preferred partner for the ANC in government were growth and re-election prospects front of the ANC mind. The EFF and the MK do not offer or even promise faster growth -they have other growth destroying re-distribution objectives.

The very different approaches to racially biased interventions in the labour market, rather than merit based value for money contracts for labour, goods and services, is a serious difference between the ideologically interventionist ANC and the instinctively more market friendly DA. Yet the interference in the SA markets based on racial identity and preferments of one kind and another has been a primary contributor to persistently slow growth. Both by making business less efficient and confident and less valuable than they would otherwise have been. And indirectly when the economic agenda- what government does – is set by rent seeking opportunists – rather than determined by a national interest in value for tax money. Any political development in SA that leads to more meritocratic efficiency and less crony capitalism would be growth and vote gathering.

Chairman Trevor Manuel is “very proud” that Old Mutual has raised the minimum it pays employees to R15,000 a month, “so taking a decisive step towards narrowing the wage gap” One presumes that this minimum does not apply to the cleaners, security guards and canteen staff contracted to supply such services. Fortunately because, if so extended, it would mean many fewer of them would be employed in these humble categories.

I would be much more inclined to share the pride in firms paying more if it was accompanied by a growing pay roll. An outcome difficult to realise when improved rewards must be accompanied by improved performance– if the firm is to survive – productivity augmented by computers, robots and AI and on the job training. The true employment heroes are the firms that can grow salaries and the numbers employed, especially at entry level, enabling the young to begin a lifetime journey up the salary scales.

It appears that this new Old Mutual minimum is very close to industry wide practice, sensibly so. It is reported that the equivalent minimum at Standard Bank is a cost-to-company salary in 2023 was R231,050 (R19,254 a month). Santam, another insurer, has also announced a comparable minimum wage of R15000 per month, noting that its “….remuneration policy has ensured that we remain competitive against market salaries, so as a result of this policy we had a very low number of employees below the living wage. However, as part of our commitment to fair pay, we formally adopted the principle of paying a living wage at minimum.”

It makes good sense for a business to be competitive for all the skills it requires, including how it rewards its senior management and also the Board of Directors who appoint the CEO’s and approve their packages. The more competitive the packages on offer, the more selective the company can be in hiring the best and the brightest. And in firing. Paying market related wages and salaries and bonuses, is not an act charity, at least in the private sector. They must be earned and continuously justified. Though proving the point to those who have never had to meet a payroll, or survive a performance review, and who may not be especially well rewarded, despite their superior intelligence, may be very difficult. Think of convincing envious academics with tenure.

The notion that there will be some gap or ratio between the rewards of those at the top and the bottom of the ladder acceptable to public opinion, is an economic nonsense that needs to be resisted in the interest of any company with an eye to the bottom line. That is given the very different supply and demand forces, sometimes global (visas permitting) that apply to top managers and entry level employees alike.

South Africa’s problem is not the lack of benefits earned by those employed in the formal sector. It is the absorption rate in SA (employed/ population) a tragic 40.8% and lower for the youngest cohorts. Absorbing the entrants to the labour force is the huge challenge for economic policy. But it will surely not be solved paying those in good jobs ever more, after inflation, as has been the practice. And thinking how wonderful it all is to do so.

There are many potential workers who might accept the minimum wage –that is not offered to them or accept even less if allowed to do so. These regulated minimums however exceed the contribution they are thought likely to make to potential employers. Because many potential workers are just poorly equipped by training or education to do so. Yet others, classified as unemployed, might find the minimum wage below their reservation wage. That is below the wage that makes it sensible for them to go to work, that will not exactly be fun, and possibly expensive to get to. That is given benefits in kind, perhaps occasional work, perhaps only a bare subsistence, provided for by an extended family.

Such potential workers are not unemployed, they are just not working – for their own good And foreign workers, with a lower reservation wage, in unknown numbers, take up the employment opportunities.

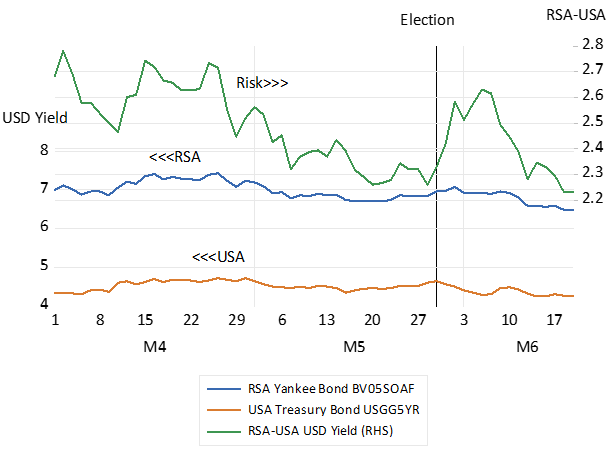

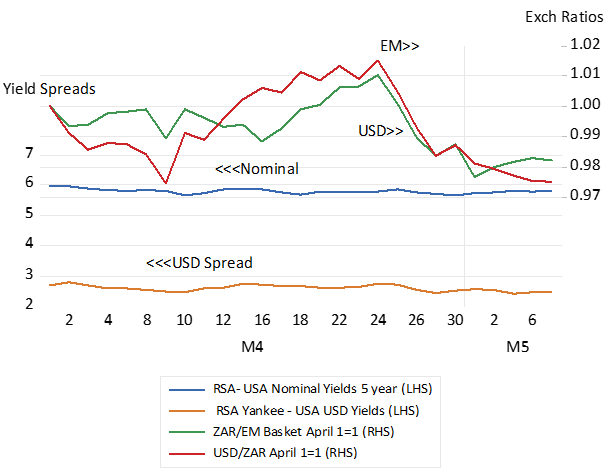

There is a confident calm in the SA financial markets despite the upcoming election the outcomes of which are surely uncertain. Since about two weeks ago the premium for accepting the risk of a SA debt default, measured as the spread between the yields on RSA dollar denominated debt and USA Treasury yields, narrowed marginally to 2.5% p.a by May 7th. It was 2.71% on April 25th. The spread between RSA and USA 5 year bond yields, has remained stable though it is still a discouragingly wide 5.8% p.a. as US and RSA interest rates moved lower off recent highs. Very recently the US dollar has become a little less expensive and value of the ZAR has improved when exchanged for other EM currencies, both by about 2% between since April 25th – which appears as the recent turning point in sentiment – and May 7th

Interest rate spreads and exchange rate ratios. April – May 2024- Daily Data

Source Bloomberg and Investec Wealth & Investment

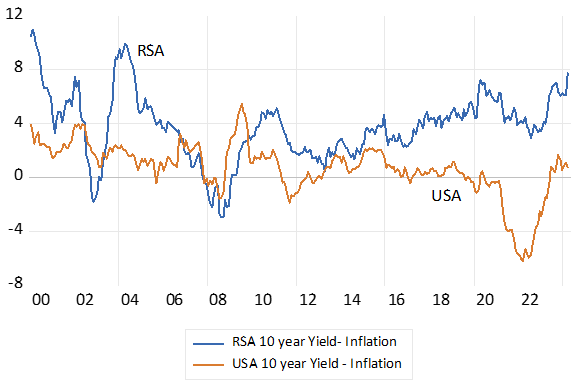

Interest rates, by themselves, tell us little about the rewards for saving or the cost of borrowing. It is after inflation interest rates, that reflect the real rewards for saving and the real cost of issuing debt. Real rates have declined with inflation in the developed world since the mid-eighties. Post covid the long decline in real and nominal bond yields appears to have reversed accompanied by higher inflation. Inflation and nominal and real interest rates in SA have remained comparatively elevated, even as inflation has receded. Since 2000 the real after realised inflation rate for an RSA 10 year Bond has averaged 3.7% p.a. while a US Treasury has offered on average a real less than 1% p.a. The current RSA-USA real yield gap is a large 6% p.a. for ten-year money. Making for undesirably expensive capital for the SA public and private sectors.

Real (after inflation) Long term Interest Rates in SA and the USA

Source; Bloomberg, Federal Reserve Bank of St.Louis, SA Reserve Bank, Investec Wealth & Investment

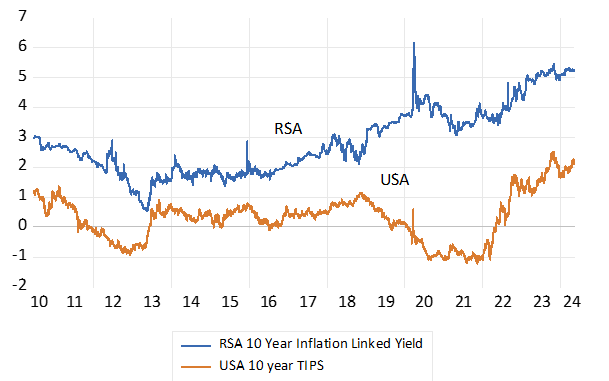

Yet with the advent of inflation protected government bonds rather than be exposed to potentially harmful, inflation events, that reduce the purchasing power of their interest income lenders can own fully inflation protected bonds. Bonds that are guaranteed to maintain their purchasing power regardless of the inflation outcomes. Since 2010 the RSA ten-year inflation linker has offered an average real 2.84% p.a. compared to an average 0.32% p.a. for the US equivalent. This real yield gap has widened significantly in recent years as RSA real yields have risen. The RSA inflation linked ten-year bond currently offer an impressive 5.3% compared to 2.1% for the US TIPS- a real spread of over 3% p.a.

Real Inflation Protected Yields in South Africa and the US. 10-year Government Bond Yields

Source; Bloomberg, Investec Wealth & Investment

Why has this high real 5.3% p.a. inflation protected yield not attracted more investor interest and a higher value? It is a rand denominated bond with no default risk- and no inflation risk. To which the equivalent vanilla bond is subject to – and to default through inflation – should control of the money supply be abandoned, as is always possible, should governments become irresponsible spenders. The current yield on an inflation exposed RSA vanilla bond with ten years to maturity is now about 12% p.a. And after inflation, if maintained around the current 5%, would become a very realised high real yield- and very comparable with the yield on the inflation linker.

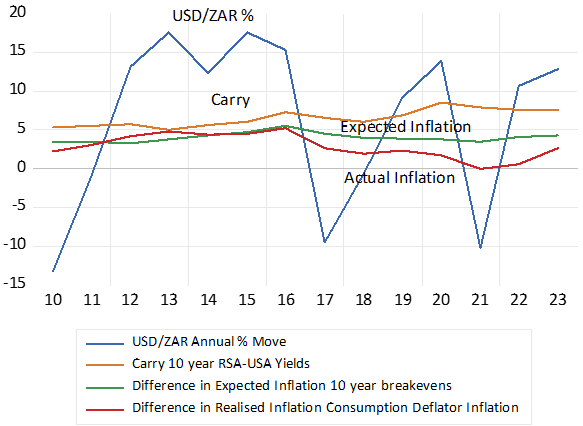

These RSA nominal and real yields are closely connected and elevated, by expectations of rand weakness. A market-based weaker expected exchange rate is revealed by the positive difference between RSA and USA borrowing costs and interest rates over all durations, from 3 months to ten years. This carry, or equivalently, the actual or potential cost of hedging rand exposure by buying dollars for forward delivery, reduces the actual or expected dollar returns on SA debt held by foreign investors. That is when they convert rand income, be it inflation protected or exposed, and capital gains in rands into dollars when exiting a trade in a rand denominated security, they will be well aware of the dangers of rand weakness. If they expose themselves to rand risks and do not hedge their exposure with forward cover, they will make a dollar profit when the rand weakens by less than the carry, that is by less than the difference in SA and US interest rates over the investment period. If the rand weakens by more than the carry they will have been better of holding the lesser interest paying, dollar denominated security.

The SA carry, the expected move in the USD/ZAR exchange rate, is however consistently much wider than the difference in actual and expected SA and US inflation. One might surmise that movements in exchange rates equilibrate differences in inflation and differences in expected inflation between trading partners. To level the foreign trading field. But this has not at all been the case. Since 2010 the highly volatile USD/ZAR has weakened on an annual average rate of a 6.3% p.a. The comparatively stable ten-year carry, the average extra cost of buying dollars for forward delivery, has averaged 6.53% p.a. while the difference between expected inflation in SA and the US, has averaged a fairly consistent 4% p.a. While the difference in realised inflation has averaged a mere 2.9% p.a. These long-term trends have made the USD/ZAR a consistently undervalued, therefore highly competitive exchange rate.

Reducing inflation will reduce interest rate levels and unhelpful interest rate volatility and real rates, as the Reserve Bank has asserted it is likely to do. But it will not necessarily make the rand more competitive as the Bank also asserts. With lower inflation the exchange rate might weaken by less than the difference in realised inflation rates between SA and in our trading partners. In which case lower interest rates and a stronger rand could well be accompanied by a less competitive exchange rate.

Interest and Exchange Rate Trends. Annual Data

Source; Bloomberg, Federal Reserve Bank of St.Louis, SA Reserve Bank, Investec Wealth & Investment

Persistently lower SA inflation and lower interest rates will therefore require not only less inflation, but less expected exchange rate weakness. That is a reduced difference between SA and US interest rates as SA interest rates fall.

How could this be achieved? A stronger rand and a stronger rand expected, and with it less inflation realised and expected, can only come with faster real growth, that would bring more favourable flows of taxes, proportionately smaller fiscal deficits and issues of RSA debt- given also restrained government spending linked closely to the same real growth trajectory. The Reserve Bank has limited influence on essential supply side reforms that would be essential to raise the actual and expected growth rates. The Reserve Bank lacks any predictable influence on the most important leading inflation indicator, the exchange rate, influenced as it is so strongly by global risk appetites as well as economic policy successes or failures. Interest rate increases at the short end of the money markets should never be used to fight rand or domestic currency weakness generally. Exchange rates should be left to market forces, and the wider spreads that accompany exchange rate weakness and the higher prices that temporarily accompany currency weakness are very hard to overcome without additional damage to the spending side of the economy. The Bank of Japan has been learning as much.

A wider or ideally a narrower carry, that is the interest rate spread between economies and currencies is part of a new equilibrium in financial markets. It reflects the adjustment to more or less perceived exchange rate risk and less or more capital supplied to a domestic financial market. It calls for the right supply side reforms that lead to faster growth and improved expected risk adjusted returns from additional private capital supplied willingly to domestic borrowers. Including to the government, the borrower that sets the level of interest rates.

The Reserve Bank as should other central banks effectively manage the demand side of the economy, so that demand, under the influence of real short term interest rates, does not exceed potential local supplies, nor fall short of them. So to avoid upward or lower pressure on prices and incomes, wage and interest incomes included. This is far from the actual state of the SA economy today. It suffers from too little rather than too much spending. The Bank could now help growth and the foreign exchange value of the ZAR by reducing what are very high nominal and real short term interest rates that have throttled domestic spending.

Lenders demand compensation for expected inflation with higher interest rates and borrowers are willing to pay more when higher prices are expected to erode their real borrowing costs. Interest rates, after inflation, therefore reveal the real rewards for saving and the real cost of issuing debt. Real interest rates in SA have remained elevated, even as inflation has receded. Since 2000 the real income owning a RSA 10 year Bond has averaged 3.7% p.a. while a US Treasury has offered on average less than 1% p.a. The current RSA-USA 10 year real yield gap is a large 6% p.a.

Real (after inflation) Long term Interest Rates in SA and the USA

Source; Bloomberg, Federal Reserve Bank of St.Louis, SA Reserve Bank, Investec Wealth & Investment

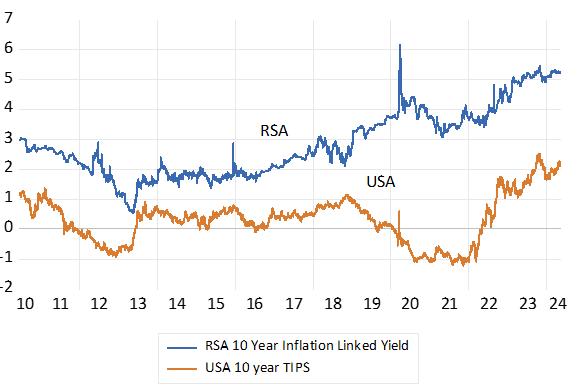

With the advent of inflation protected government bonds, lenders can now avoid exposure to uncertain inflation. They can buy a bond with a guaranteed real return. That is receive an initial yield to be augmented by actual inflation. Since 2010 the RSA ten-year inflation linker has offered an average real 2.84% p.a. compared to an average 0.32% p.a. for the US equivalent. This real yield gap has widened significantly as RSA real yields have risen. The RSA inflation linked ten-year bond currently offers an imposing 5.3% compared to 2.1% for the US TIPS- a real spread of over 3% p.a. Capital is really very expensive in SA and discourages capex.

Real Inflation Protected Yields in South Africa and the US. 10-year Government Bond Yields

Source; Bloomberg, Investec Wealth & Investment

Why has this high 5.3% p.a. real yield not attracted more investor interest and a higher value? It is a rand denominated bond with no default risk- and no inflation risk. To which the equivalent vanilla bond is subject to – and at worst should inflation accelerate – to the effective expropriation of wealth tied up in a bond. The current yield on an equivalent vanilla bond is now about 12% p.a. Time will tell whether it delivers a real return in excess of the certain 5.2% on offer from the inflation linker.

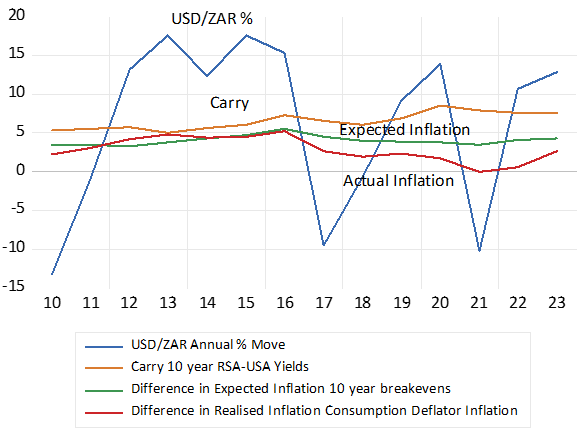

All the RSA bond yields are connected and elevated by expectations of rand weakness. That reduces the expected dollar returns for any foreign investor. The weaker expected course of the rand is revealed by the positive difference between RSA and USA interest rates over all durations. This carry, or equivalently, the actual or potential cost of hedging or compensating for exposure to the rand, reduces the actual or expected dollar returns on SA debt held by foreign investors who are an important source of capital for the RSA. It is expected returns in dollars not rands, even inflation adjusted rand income, that guides their investment decisions.